We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Tax on Savings

Comments

-

Sorry everyone if my method is wrong. It is truly a dreadful system if there is not a clear way of inputting. I looked very hard and there was no place for me to put interest income or Investment income.

So the only place I could put it was as Other (non-earned income) which Dazed is saying is a wrong way to do it.

Dazed has said on another post that the Interest section is not there yet for 2026-2027. That's why I could not find it. Maybe it will show up after April 6th? Meanwhile, I shall attempt to remove this other income.

1 -

i have an update after calling HMRC this morning.

DeductionCurrent tax year ends 5 April 2026Next tax year from 6 April 2026Untaxed interest on savings and investments£573£758Total deductions£573£758They told me that the figures above are included by HMRC because i will not be earning £12570 and these fill the gap from what i earn to to fill my personal allowance. They have now increased my part time income to fill the gap and removed the "untaxed interest on savings and investments". And yes, i heard that correctly as i asked him to repeat the explanation. He agreed that the system does not make sense but thats the way it works! Wow

2 -

Both myself and my daughter experienced this same issue re 'untaxed interest' being taken off of our tax codes.

When I phoned I was given the same explanation - that it's just what the system does. They adjusted my estimated income for the year 24/25 ( to more than I actually received)and that got rid of it. I haven't bothered doing anything about it this year.

As soon as my daughter started work and was earning above the personal allowance the unearned interest bit disappeared from her tax code

It's a rather confusing thing to happen and actually quite worrying when we first saw it - we both knew we hadn't earnt enough interest to pay tax. I spent ages going back through all my records to make sure I hadn't made a mistake somewhere

If they want to ' fill up' a tax code they need to come up with a much more suitable name

2 -

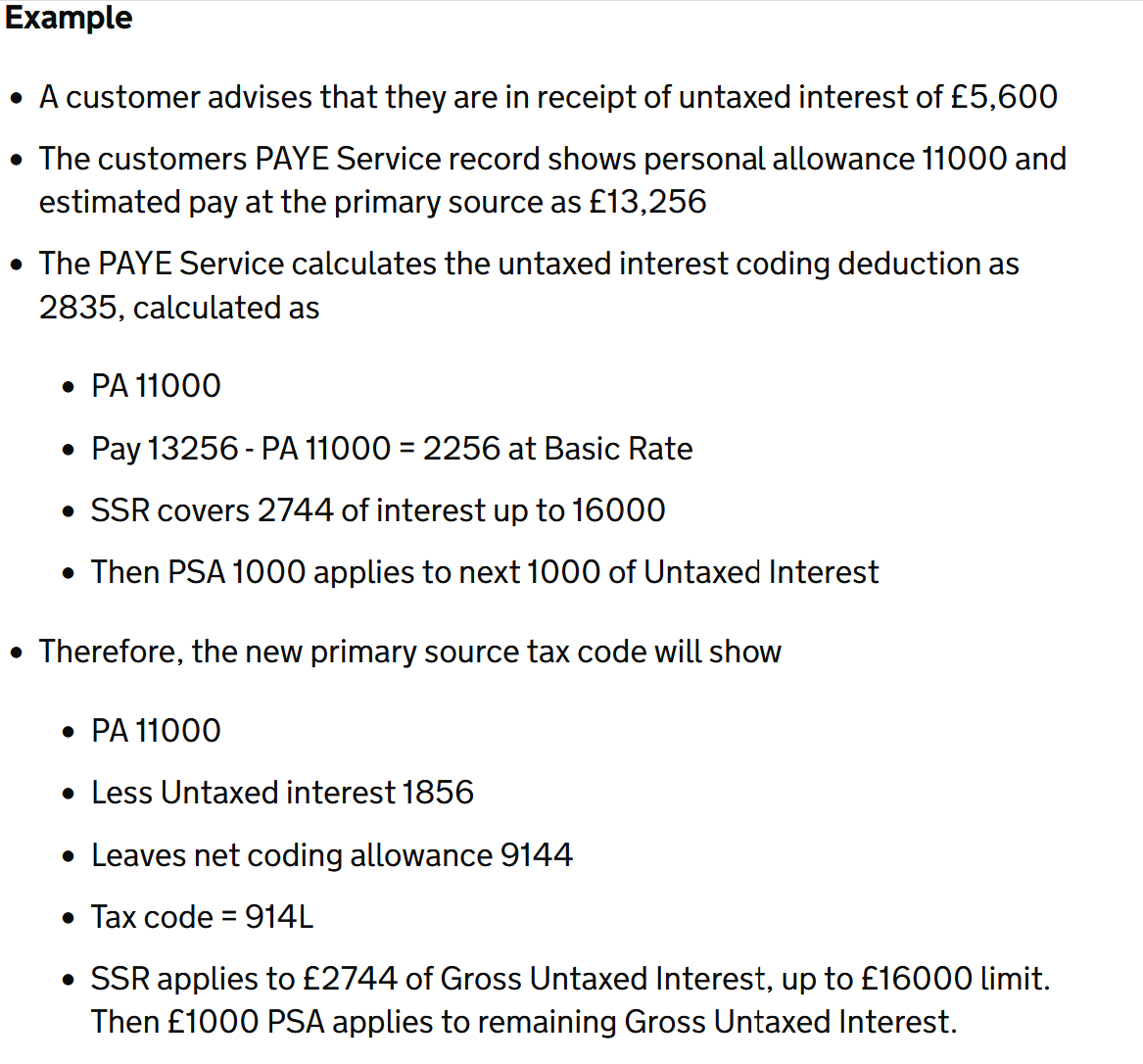

From the HMRC manual (the example shown below) HMRC should, as I understand it, only be coding in for the estimated savings interest on which tax will be actually paid, i.e. taking into account the starter savings rate and the personal savings allowance (?)

Consider someone with only estimated employed earnings of say £12,500 (i.e below the personal allowance) and say £6,000 of savings interest. By my reading there should be no adjustment in their employment tax code for savings interest because that is expected to be covered by the 0% starter savings rate and the £1,000 0% personal savings allowance band (1257L).

Presumably if mid tax year their estimated earnings increases to say £13,570 they in theory should be issued with a new tax code including a deduction in their tax code of £1,000 for savings on which 20% tax is estimated to be paid, (1157L)?

Is my understanding correct?

In my case HMRC are coding out all of my expected interest and not taking into account either the starter savings rate 0% band or the personal savings allowance 0% band. It's not an issue in my case. But I can see how it can cause confusion if someone updates their HMRC record with their estimate of savings interest without any deduction for the personal savings allowance (as I understand they should) and HMRC fail to take into account the personal savings allowance for example in the issued tax code.

I came, I saw, I melted0 -

No, you are overlooking the £70 of unused allowances.

The 0% bands only kick in after the allowances have been used.

So the code would be 1250L in your example.

2 -

Thanks. I've just seen Spivo46s post and can see that's what has happened there also.

If we take the purpose of tax codes to be a first stab at getting the right amount of tax deducted it seems a daft way of doing it.

Someone with say a pension of £8,000pa and estimated savings interest of £6,000 will be given a tax code of 800L. If that person gets a small increase during the tax year to that pension then they will start to pay tax if the tax code remains in place, and so they will either need a new tax code or have to get the overpaid tax refunded via a P800 after the end of the year.

It would make much more sense to give them a tax code of 1257L and then all bar a major change in income would mean the original tax code could remain in place and the tax deducted would be correct despite the pension increase.

I came, I saw, I melted0 -

Thank you all for the feedback, appreciated. I got there in the end. Special thanks to the HMRC.

In summary; our tax system is a dogs dinner. Nobody really understands it fully, including HMRC employees. Even well educated finance people disagree on the actual workings within the so called system. Perhaps it could be made a little easier to understand, or is that asking too much??

1 -

Yes @Spivo46 it's completely befuddled me to the point that I momentarily considered closing all my savings accounts and keeping all my money in a non-interest earning current account for a year just to "reset" the system. Obviously that's totally OTT, but what I will be doing next FY is keeping an exact record of all interest I earn and checking to see if HMRC figures match.

I suppose giving everyone access to the their tax account online is a good thing, but the user interface really needs some reworking into a clearer format.

2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards