We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Money Moral Dilemma: Should my employer adjust its rewards scheme so I don't lose out?

Comments

-

Not only that. My employer said several years ago that HMRC had told them that when they gave employees vouchers they had to show any tax they paid on the employee's behalf on their payslip and on their end-of-year P60. Payslips now show gross value of vouchers given, net value of vouchers given and tax paid on the gross value.

I assume that's because employers don't have enough information to know an employee's marginal tax rate so HMRC were concerned that the employer was not paying the correct amount of tax.

1 -

Speak to your manager / employer HR and explain your dilemma, they may be able to help. Presumably your salary is at the level to avoid repayment charges, so giving you a bonus to trigger them seems counterproductive.

As for the taxability of "reward" bonuses it depends on how much they are, what form they take ie company or third party provided, and how they are paid.

0 -

Vouchers are not subject to tax, however, they are subject to class one NICs.

Long Service Awards aren't, but rewards vouchers are

https://www.gov.uk/hmrc-internal-manuals/national-insurance-manual/nim02416

I wonder how Student Loans calculate income - based on taxable income or just everything reported on the P11D as a BIK?0 -

They're not subject to tax.

You're talking about vouchers that can be exchanged for tax.

https://www.gov.uk/expenses-and-benefits-vouchers/what-to-report-and-pay0 -

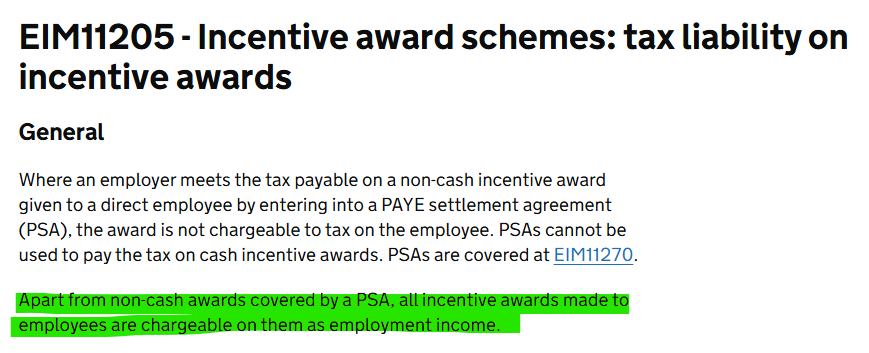

You're looking at the wrong part of the tax guidelines. Incentive awards, including non-cash vouchers, are covered here:

0

0 -

Ad-hoc unpaid leave would seem to be an answer to the immediate problem and could also mean an extra long weekend away somewhere or even just time to spend on a boxset or with family/friends…

It also depends how much they want to 'rock the boat' but if the company is compensating for other government deductions then I don't see why they should not do so for a quasi graduate tax. My latest employer would probably listen to most concerns but a few previous ones would view the request negatively.

0 -

It seems that you want to avoid paying back your student loan fees ….. why?

1 -

because student loans fees are effectively a graduate tax and

"Every man is entitled, if he can, to order his affairs so that the tax attaching under the appropriate Acts is less than it otherwise would be. If he succeeds in ordering them so as to secure this result, then, however unappreciative the Commissioners of Inland Revenue or his fellow tax-payers may be of his ingenuity, he cannot be compelled to pay an increased tax"

Althogh, as pointed out up thread, its a non-issue as the pseudo-OP will get back the extra payment caused by the bonus at the end of the tax year

0 -

Ask if you can either salary sacrifice it into pension, or buy something & get reimbursed for it, which if latter you might be able to click on the VAT

0 -

They may have attended university during COVID, when students cannot be blamed for feeling short changed. You could argue that those who started in 2020 knew what they were getting into, but those who started in 2018 or 2019 had no choice as they were already committed before it was known that they would be expected to pay full fees for a diminished service/experience.

Many people ask for and receive advice on how to keep their income within the basic rate tax band without any judgement, so I don't see why staying under the student loan repayment threshold should be any different, especially given the upcoming freeze - they may have made a different decision had they known that the terms of their loan could be unilaterally changed.

In answer to the question, I don't think the employer should have to make any adjustment unless they did not give you any time to decline the reward and avoid ending up worse off as a result. That is generally what happens when people qualify for payments they weren't expecting, e.g. Nationwide Fairer Share. Religion may also prevent some from accepting, so it is not fair for an employer or anyone to assume that everyone would welcome free money. But the employer isn't responsible for you taking a student loan, so shouldn't have to adjust the scheme for one person.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards