We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

USS DB Pension - claim early while working?

I will get my USS Pension in September 2027 - no option to defer, and my state pension two years later, at 67.

I've recently found out that I can claim the DB pension early. I've done a few projections on their online calculator to get an idea what I can get at 65, 64 and 63 (I'm almost 63.5 now).

If I had claimed at 63, my lump sum is estimated at £1224 less than if I waited till I hit 65, and the annual pension would be £184 less.

Comparing those to the amount I would have had over the extra two years I'd have been claiming the pension, it looks as though I'd be better off claiming.

The loss of lump sum + (reduced pension x 25 years) = £4600.

The gain of two more years' pension payments = £26,000.

Am I missing something? This sounds like free money if I claim it now.

Comments

-

An actuarial reduction of less than 2% for taking your pension 2 years early doesn't sound quite right to me.

N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

2.72kWp PV facing SSW installed Jan 2012. 11 x 247w panels, 3.6kw inverter. 35 MWh generated, long-term average 2.6 Os.2 -

2 years early would be 10% reduction but maybe the OP has different NPAs for different bits of pension so it is not 65 for all of it?

3 -

Thanks for your responses. It didn't sound right to me. The whole pension is payable at 65. I worked at a university from 2000 until the end of 2015. The scheme changed after I left.

I suspect the online calculator isn't accurate. I suppose I may need to get an actual quote, both for claiming now, and claiming at 65.

I'm planning to keep working until I'm 67 anyway, I just didn't want to make a poor decision if the figures are correct.

0 -

Yes, I've seen this myself.

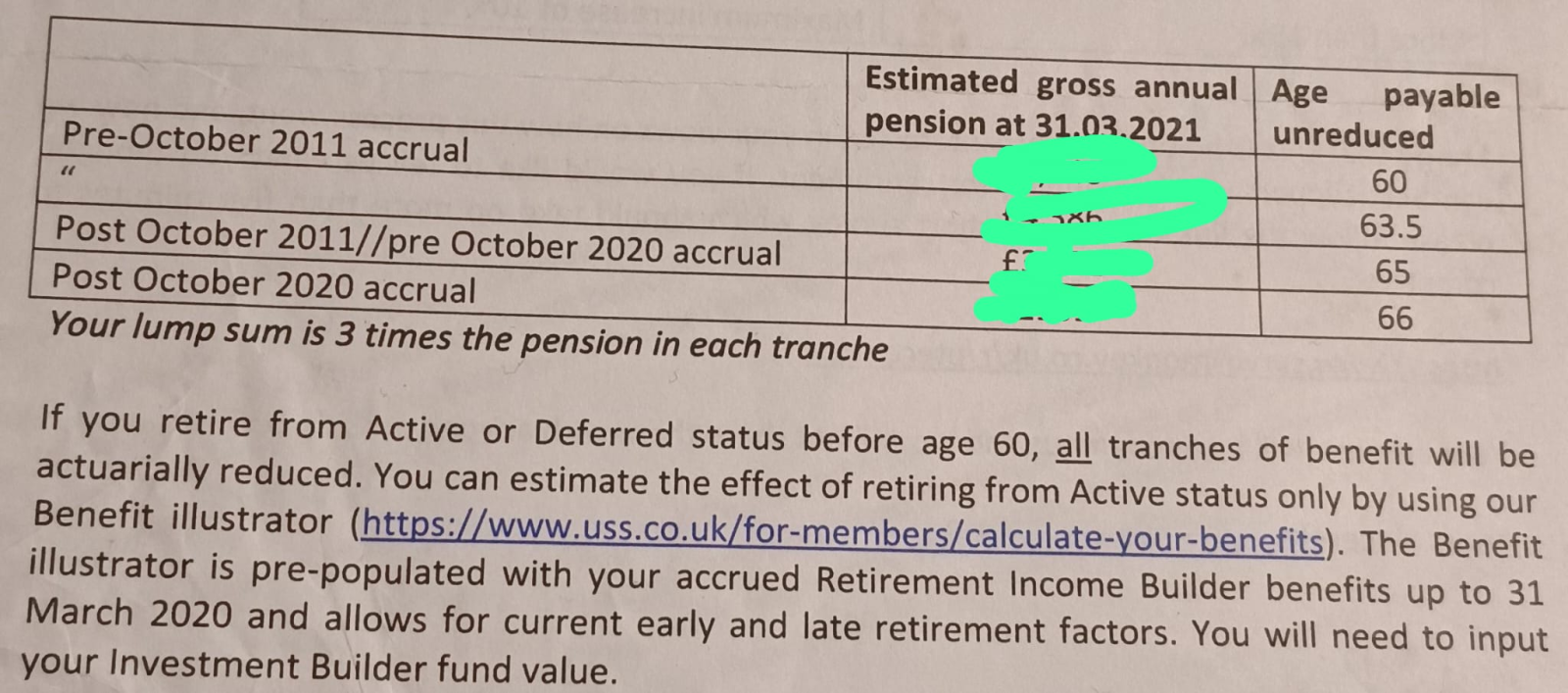

Here's an example from the USS of how differing Normal Pension Ages(Age payable unreduced) can apply to the different bits of a pension as mentioned by DRS1 above.

The key considerations are how much of your pension falls into each of the different tranches/pots, what the reduction is for those pots started early and what increase there are in the tranches/pots that have passed their Normal Pension Ages.

There can also be university specific rules about taking later pots without any acuarial reductions.You may also want to consider any effects of an increase income in terms of overall income and tax thresholds

In my example, the conculsion was the same as your, taking the pension earlier resulted in more pension payout overall. The USS scheme administrators should be able to give specific figures and confirmations for your pension.

2

2 -

Thanks Uncle Tom, that's really interesting.

When I do claim this pension, whether at 65 or earlier, I'm planning to increase my investment into my current SIPP by the equivalent amount, as otherwise I'd fall into the 40% income tax band. I'd rather pay 20% on the money after retiring when I need it, than 40% now when I really don't need it.

Time to get a couple of quotes I think. Thanks for the advice.

0 -

If you don't need the money then I'd say don't take it.

I’m a Forum Ambassador and I support the Forum Team on Debt Free Wannabe, Old Style Money Saving and Pensions boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.

Click on this link for a Statement of Accounts that can be posted on the DebtFree Wannabe board: https://lemonfool.co.uk/financecalculators/soa.php

Check your state pension on: Check your State Pension forecast - GOV.UK

"Never retract, never explain, never apologise; get things done and let them howl.” Nellie McClung

⭐️🏅😇🏅🏅🏅🏅🏅1 -

You can take the final salary portion of USS up to 2011, which sounds like it might be most of your pension, unreduced at 63.5

There are no late retirement factors between 63.5 and 65.

If you take it later than 63.5 you are giving up money in that tranche.

This will be somewhat offset against the early retirement factors from other tranches of the pension, given you have to take it all at once, and different accrual years can have different retirement ages.

However for service between 2000 and 2015 it's a good bet that you'd be significantly better off retiring at 63.5

4 -

That is usually good advice, but in this very specific case potentially means leaving money on the table

3 -

We have different NRA's for different time periods like that, specifically 60 and 65. On our scheme we could take the pre-2011 (i.e. split the pot) and leave the rest until we reached the relevant NRA without reduction. I work with a couple of people who have done that….but could be a scheme exception as opposed to the norm out there.

1 -

I know you may have this sussed but with the talk of your current SIPP, I'll mention it. The USS scheme also has this option which can allow a larger tax free lump sum to be taken alongwith the start of the DB. It did mean that money placed in the Investment Builder can be paid out, in effect, tax free.

As I said, you may well know all about it but it can be such a good benefit I though I'd point it out.

There are other posts on the details.2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards