We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Royal London Governed Portfolio

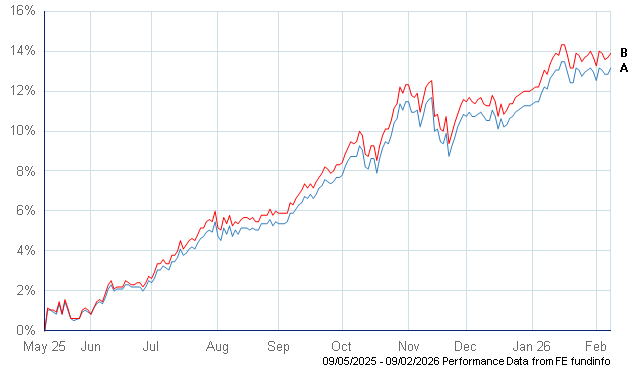

Governed Portfolio Growth (B) vs GRIP 5 (A) - I would be very interested to hear your thoughts regarding the choice between having your pension funds in one or the other. they appear to be very similar? Why have these x2 very close variants?

Comments

-

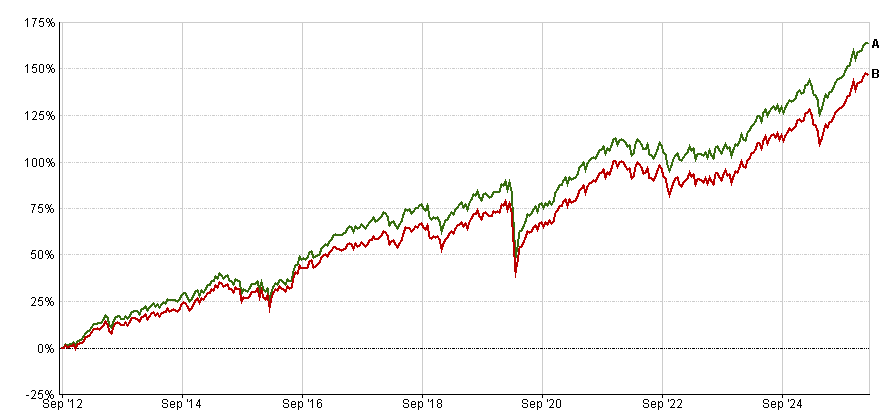

and here is a longer period (Grip 5 A/green & GPGrowth B red)

They are similar in that they cover the same risk profiles and have some overlaps. However, GRIP tilts toward yielding assets and more diversified assets (e.g., commodities and absolute return).

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0 -

If you look at the info on the RL website, there's comprehensive information there which both answers your question and gives a lot more detail if you need/would like it: https://adviser.royallondon.com/globalassets/docs/shared/investment/br5pd0001-our-governed-retirement-income-portfolios.pdf

Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!1 -

Thank you - are you sure these are correct, they contradict my original graph that indicates GP Growth outperforms GRIP?

0 -

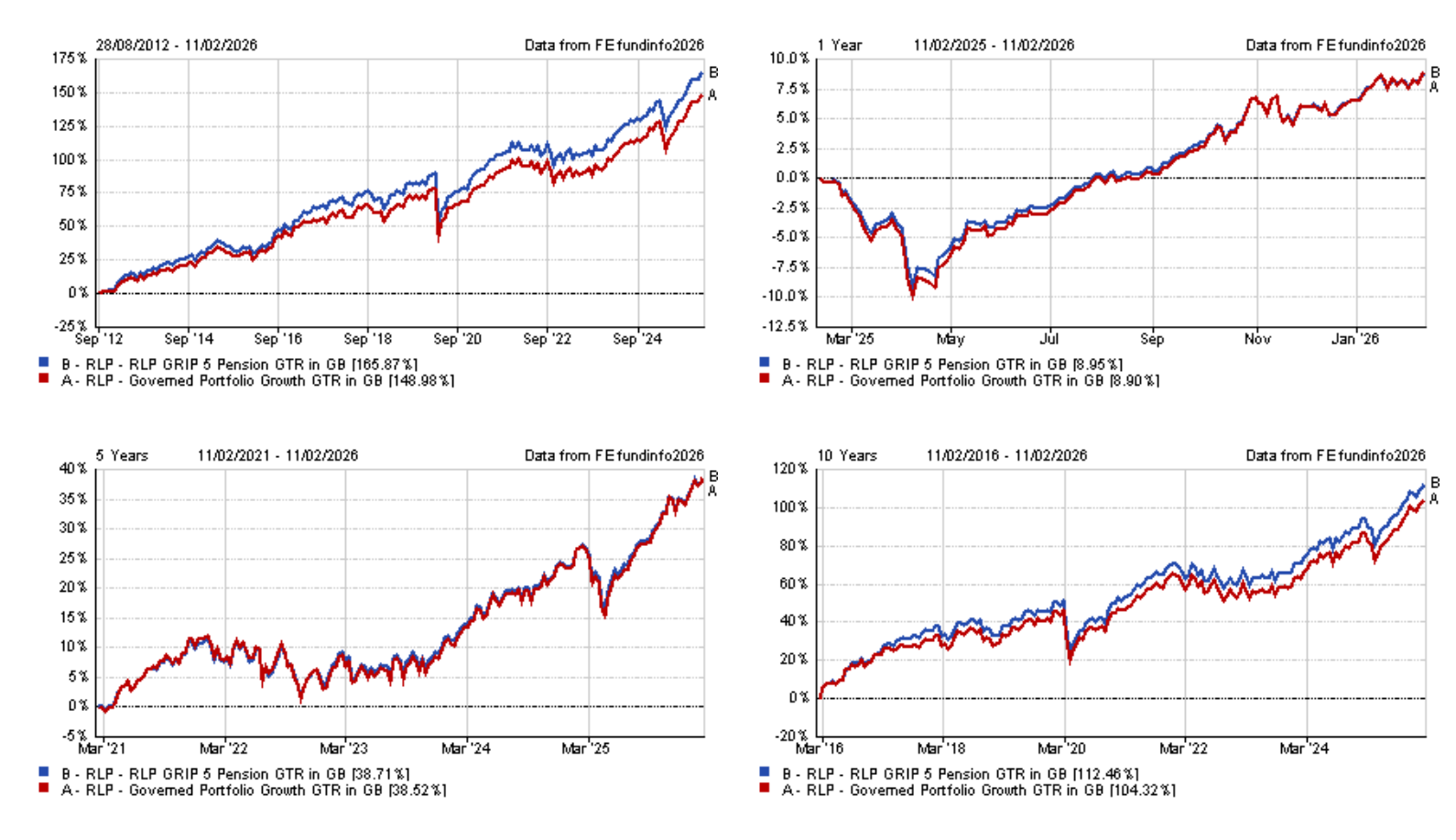

I just looked again and that is what FE is showing:

The period from May 2025 matches yours and has GP above GRIP

You need to make sure you are looking at the right versions.

RLP is the version used for pensions and has history going back to 2009 for GP and 2012 for GRIP.

RLI is the version used for ISAs. RLI was a new fund launch in May 2025.

The pension funds are bundled. The ISA is unbundled. This is why the RLI version has better performance than the RLP. However, while there are no additional charges for the RLP version, the RLI will incur a provider charge on top which will (depending on the charging tier) wipe out the difference.

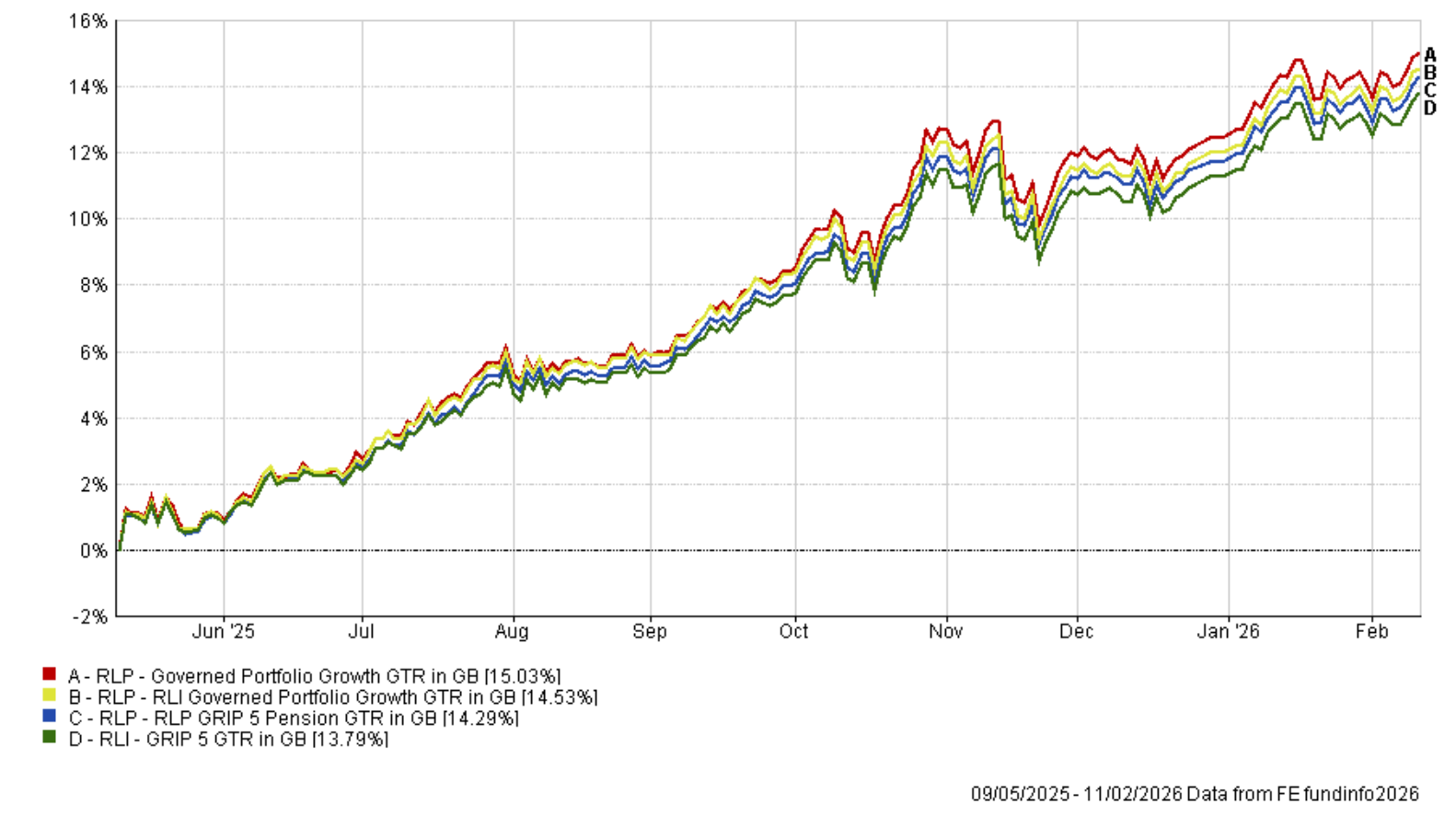

There is currently a naming error on FE: fund names are inconsistent in some cases (e.g., B shows RLP-RLI when it should show RLI, as in the same way as D).

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

I really appreciate the information - thank you.

I have started retirement and think GRIP5 may be the better option, given that the past returns have been marginal

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards