We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Are my pensions going to be enough?

I'm 50

Top photo is from a place i worked at for ten months

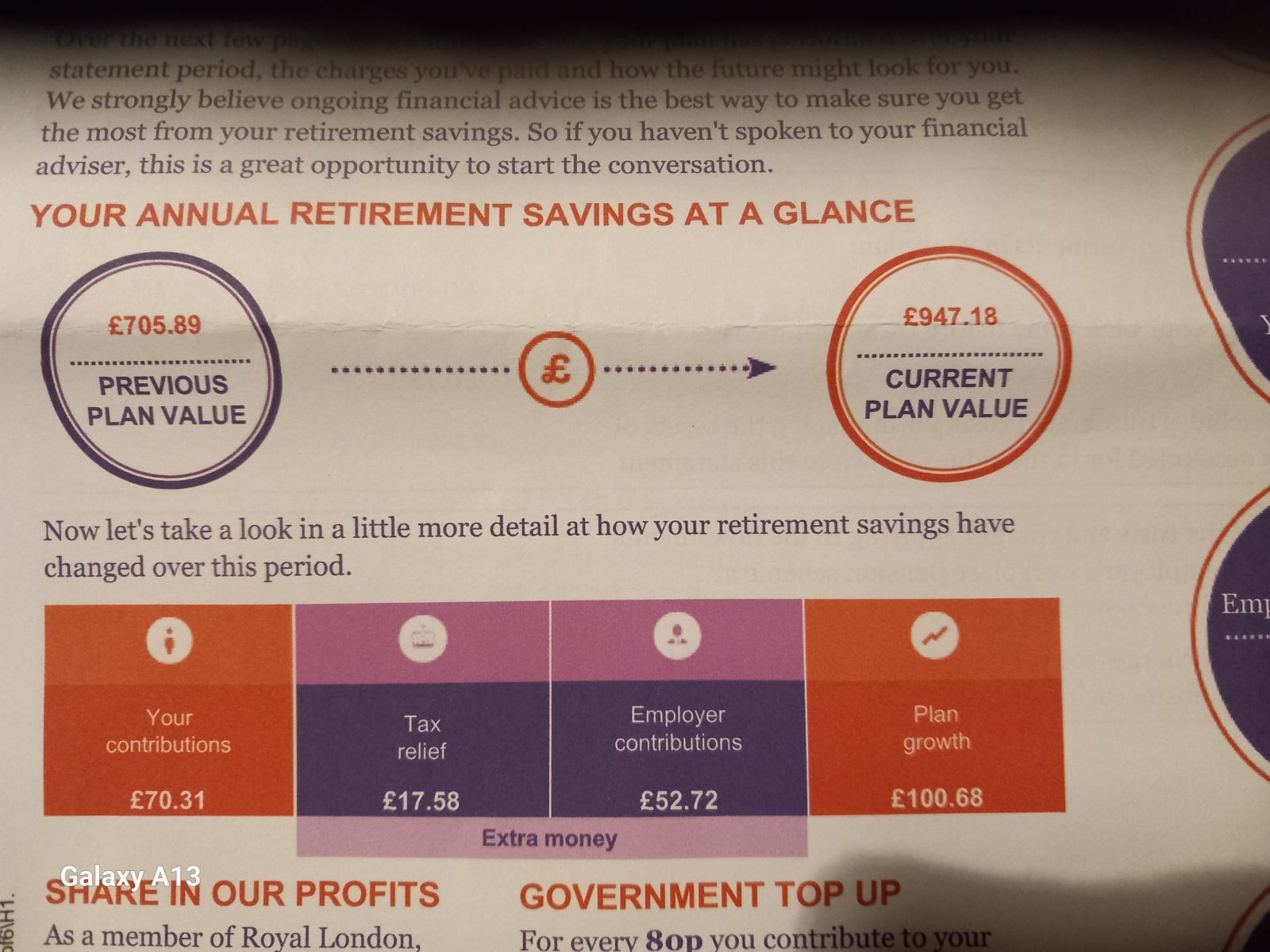

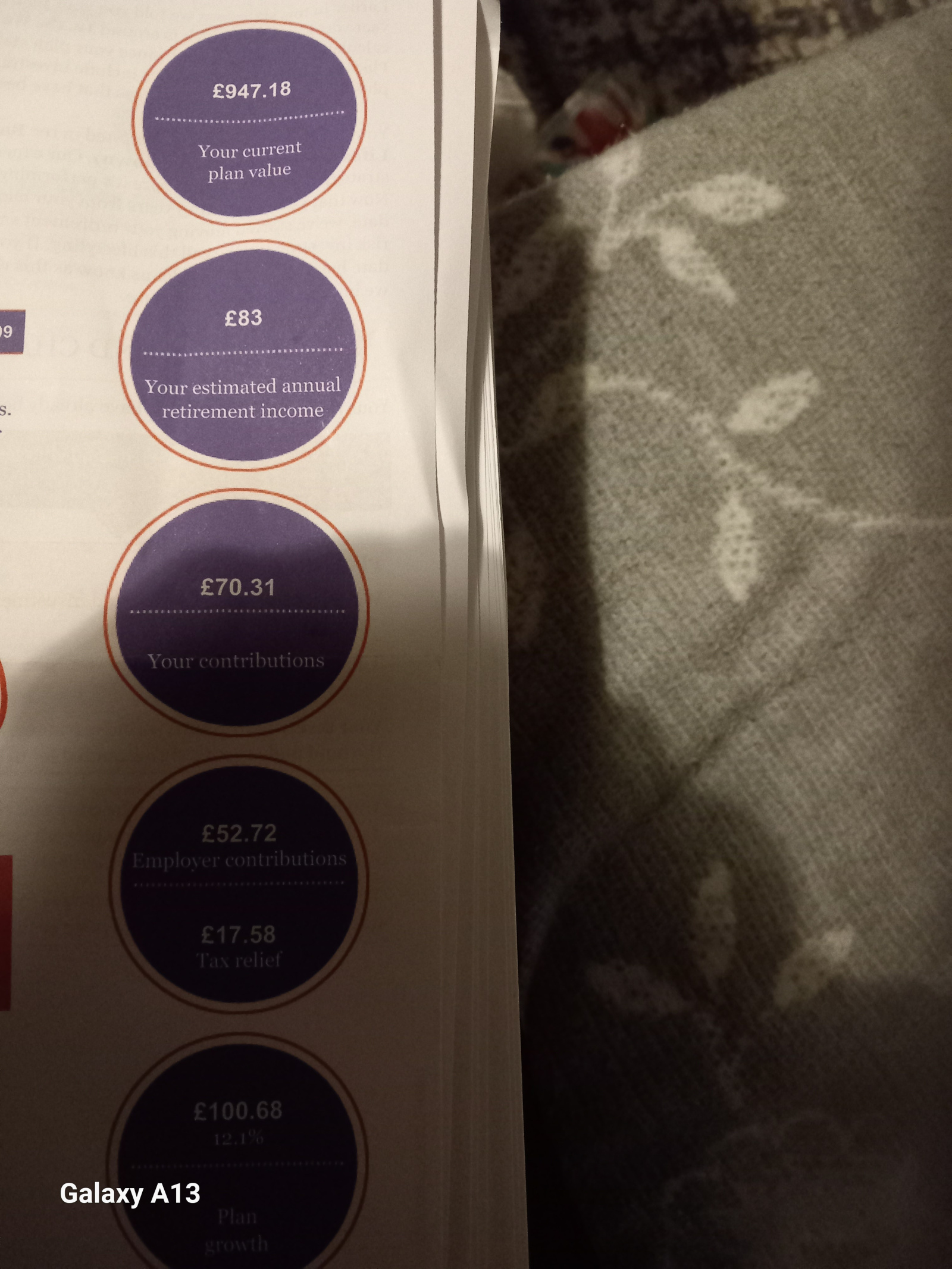

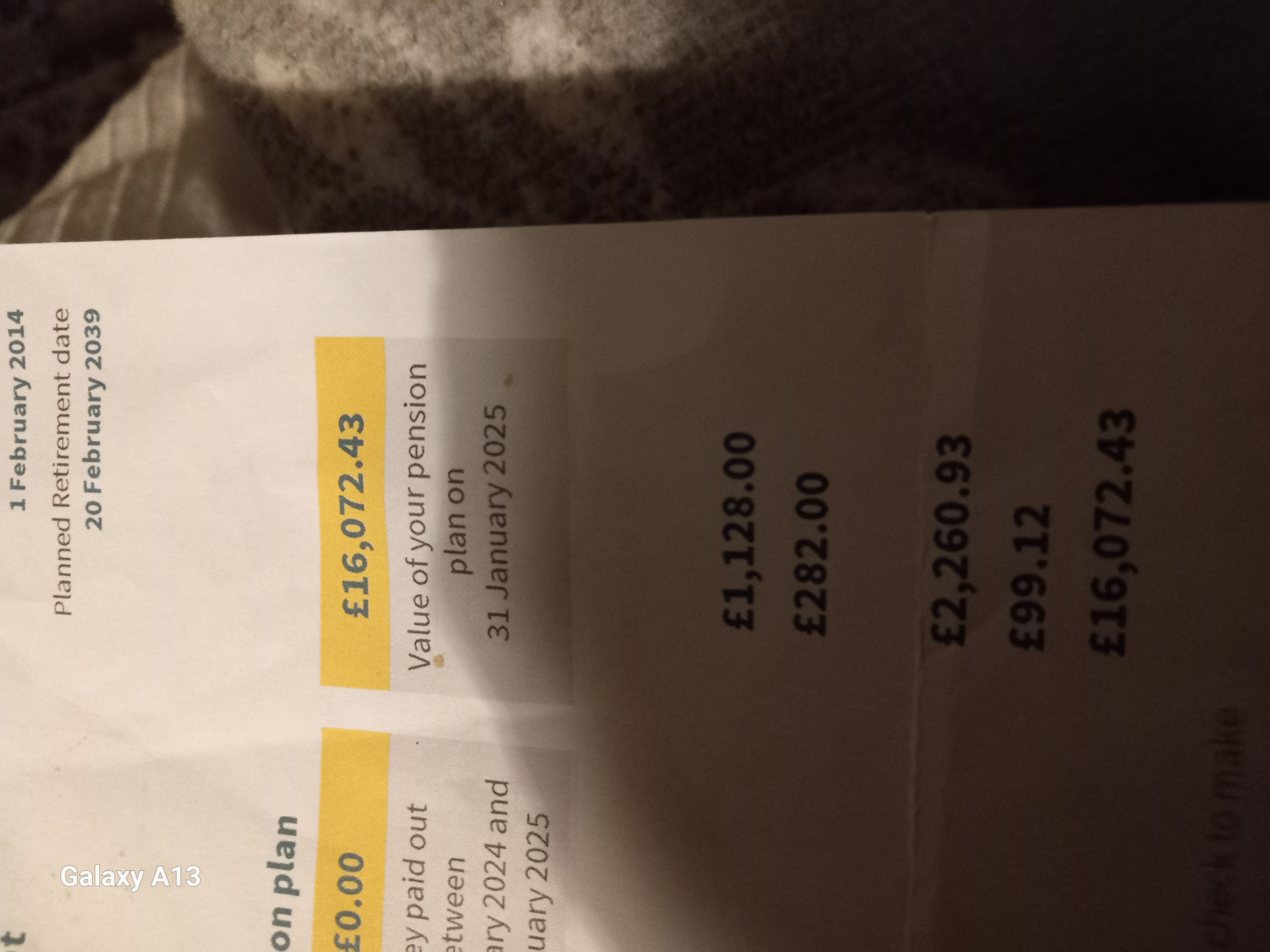

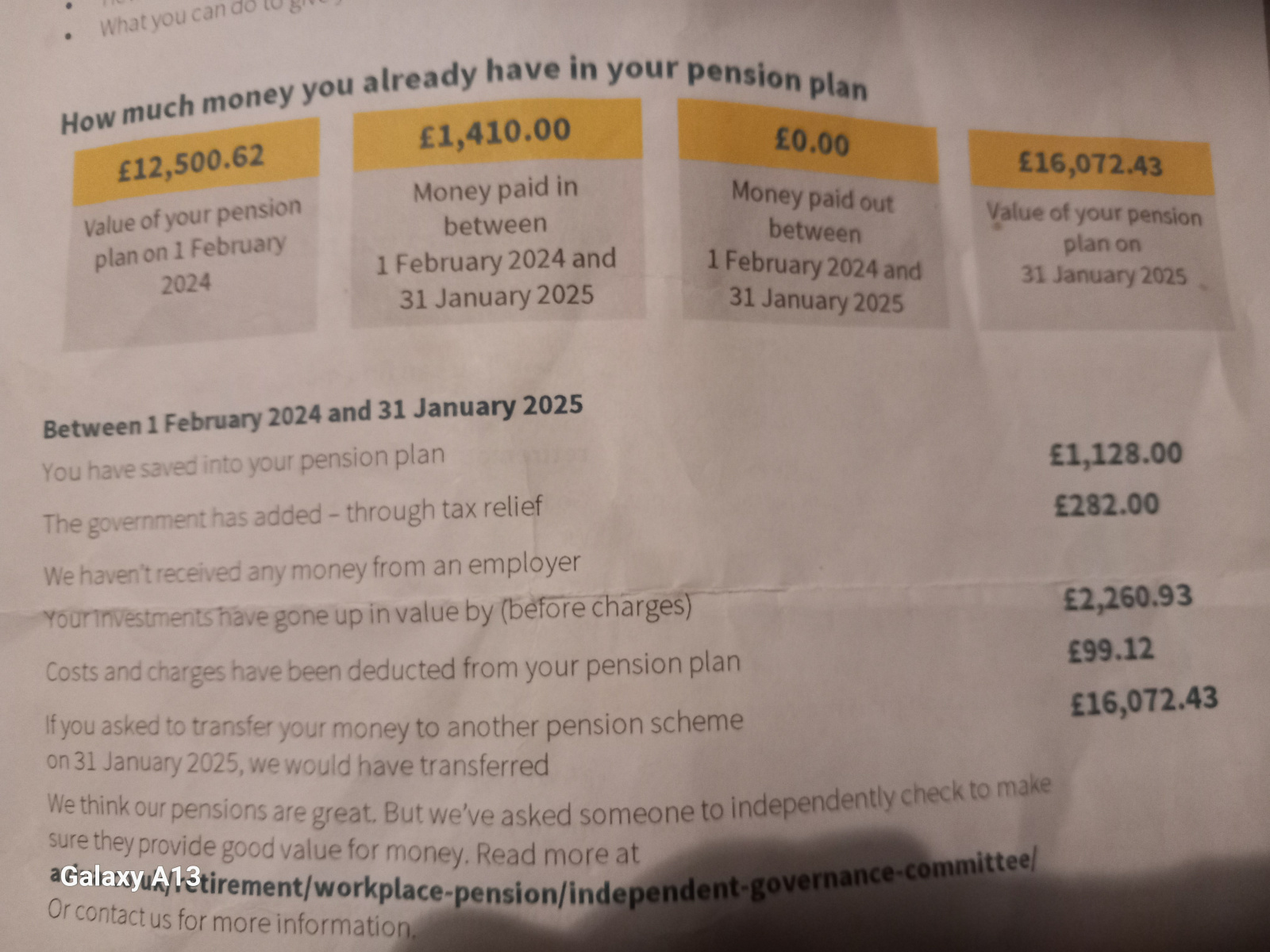

Bottom photo shows my Aviva private pension; pay £120/month into it.

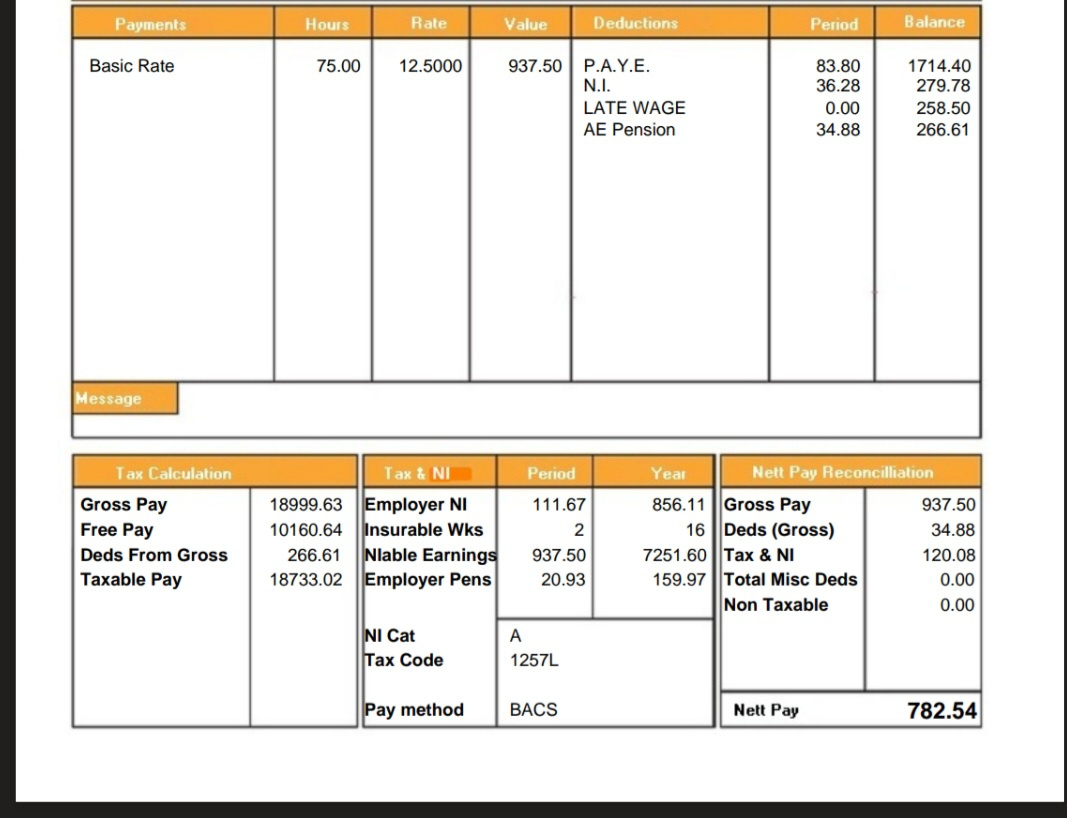

Payslip shows my current payments to a workbased pension, can I ask them to increase this? How much am I getting off it? Any good?

How do these compare with police/pcso/nurse pensions I heard if nurses pay in £200 tax payer adds £500 every month, sounds like a scam to me

Comments

-

it’s difficult to compare a Defined Contribution pension like yours with a Defined Benefit pension, like what nurses get. DB pensions give a guaranteed income for life once in payment, DC pensions are just a pot of money that is worth what the investments are worth. DB pensions are generally a lot more value for money for the employee, at least partial compensation for the fact that public sector salaries tend to be lower than private sector salaries.

if these two pensions are the only pensions you have then at age 50 you need to be thinking about adding a lot more to a pension in order to have a decent retirement.8 -

looks to me like you need a better employer / job.

the employer pension contribution is miniscule.

and that pay slip is one of the worst I have seen in terms of laying out information.6 -

Firstly, the important thing is that you ARE currently paying into a pension… and getting your (free) employer contributions and tax relief… many people aren't even doing that.

You say you are 50 (i'm 52) and you have 10 months in the top (£947) pension and £16K in the Aviva (private) one,

At £120 per month I'd roughly guess that you may have been in that Aviva scheme for about 8 years to have amassed the currrent £15k?

You don't say how long you have worked at your current role, but it looks like about £55 (including your employer contrubution) is going into that per month. Do you have a current valuation for this scheme, or can tell us how long you have been working there and making contributions?

My next question would then be: Did you not have any other employement in the 20-25 years between, say 18 and 40-42 where you may have also contributed to an employer pension scheme?

• The rich buy assets.

• The poor only have expenses.

• The middle class buy liabilities they think are assets.1 -

How do these compare with police/pcso/nurse pensions I heard if nurses pay in £200 tax payer adds £500 every month, sounds like a scam to me

Pensions for public sector employees are typically much better than those for private sector employees.

No idea why you might think it is a scam.

3 -

Been working in my current job for 12 months. £55/month is terrible if my contribution and employers added together reaches this total. Can I call up payroll and legally force them to pay more ?

Been in Aviva pension for about 10 years. I paid less in initially.

No pension contributions before 42 no.

I desperately want to sort this out and been applying for police jobs despite my age, council or education work would be good too. Thinking of upping Aviva payments from £120 to £200

0 -

You might want to start off by reading the pension policy you have with your current employer, and to see what happens to employer contributions if you increase your contributions. You may find that your employer might increase their contributions when you do the same.

0 -

Been working in my current job for 12 months.

If the payslip you've shared is typical, you're working for 75 hours a month (less than half of full-time hours) on £12.50 an hour (little more than minimum wage) and grossing £937.50 a month.

If that's enough for you to live on, and assuming you qualify for a full state pension when you retire, the state pension of £230.25 a week (£921 every four weeks) will be broadly equivalent to your current wage.

Any private pension will be on top of that.

Have you checked your state pension forecast?

I desperately want to sort this out and been applying for police jobs despite my age, council or education work would be good too.

I don't know what your current job entails but, based on the wage, it's likely to be unskilled. If you have workplace skills then you should be looking for higher-paid work, whether public sector or private.

N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

2.72kWp PV facing SSW installed Jan 2012. 11 x 247w panels, 3.6kw inverter. 35 MWh generated, long-term average 2.6 Os.1 -

Many of the public sector manual jobs, such as caretaker, have been outsourced and new joiners may not be eligible for LGPS etc membership.

Unless OP is after an admin job.

2 -

With that level of individual pension savings, state pension is going to be a big part of your retirement income, so it's worth checking what you are on course to receive, as QrizB suggests.

It's also worth thinking about what benefits might be available, especially if you find your state pension is not going to be the full amount. If you will be receiving less than the pension credit threshold, and assuming the rules are the same at that time as they are now, you might find that you lose out on benefits if you have saved for extra pension. Makes it much less of a good idea to give up money now, only to find it doesn't actually increase your income when you retire.

If you're on course for a full state pension, you'll probably already be above pension credit level, and extra pension savings do make sense in that case.

0 -

Sorry should have explained I get paid every two weeks. This paycheck is for two weeks work. So ivguess my monthly pension is 2x £55 so £110.

And have my own separate one I pay £120/month into

2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.3K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards