We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

State pension calculation and HMRC calculator

Comments

-

This is mostly idle curiosity, but I'm hoping someone here can help me understand the basis for the UK state pension calculation.

https://forums.moneysavingexpert.com/discussion/comment/81545382/#Comment_81545382

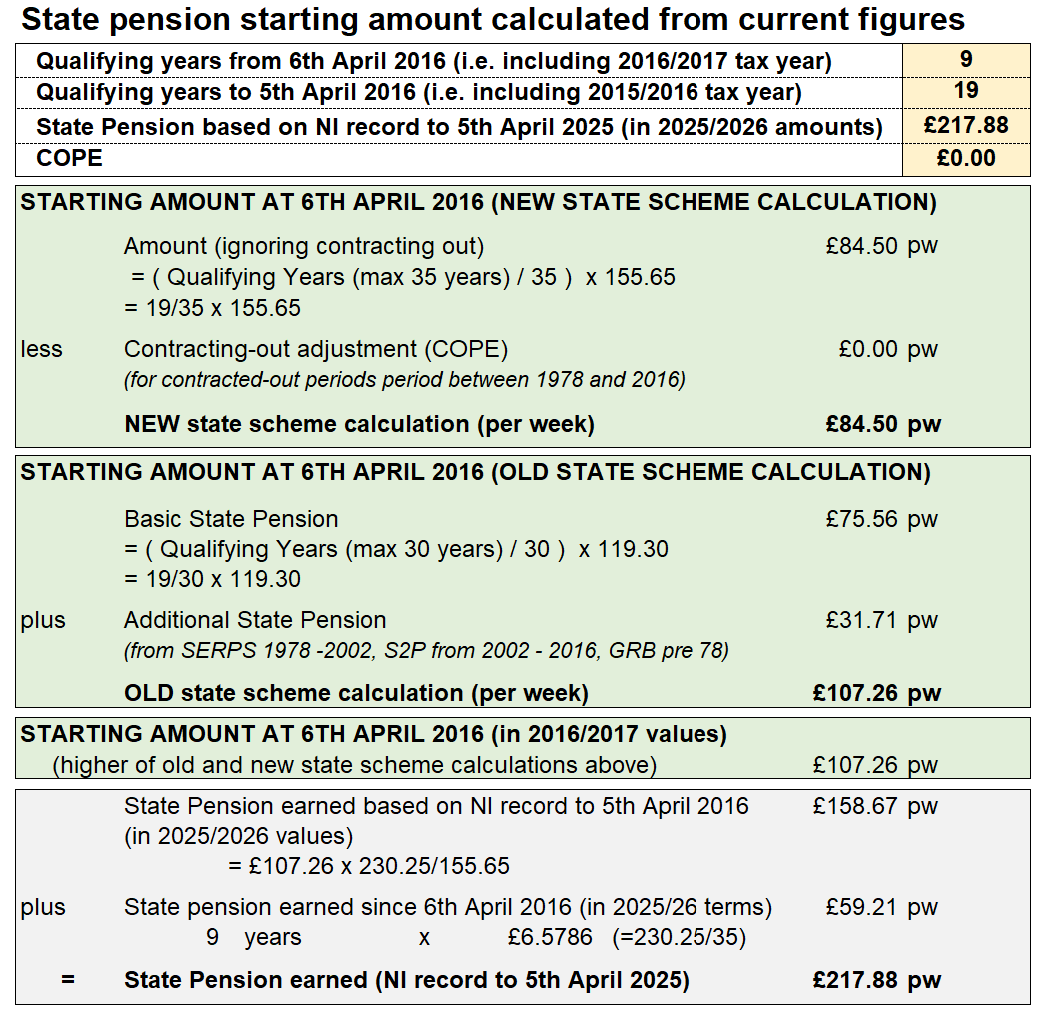

You are now aged 50. You have never been contracted out. You had 19 NIQY AT 6/4/16

Thus at 6/4/16, your starting amount for new SP was the higher of

Old Rules

{19/30 x £119.30) + SERPS/S2P. £75.55 + SERPS/S2P.

New Rules

19/35 x £155.60 £84.49

Each QY from 6/4/16 onwards would add 1/35 of NSP up to (BUT NOT BEYOND) full NSP.

2 -

£217.88 to April 2025molerat said:cockerWalker said:

Thanks.molerat said:cockerWalker said:Hi,

This is mostly idle curiosity, but I'm hoping someone here can help me understand the basis for the UK state pension calculation.

When I go to the HMRC state pension calculator it tells me "Forecast if you contribute another 2 years before 5 April 2042 £230.25 a week". I'd qualify in 2042 based on current law (I'm 50).

When I look at my NI record it tells me I have 28 full years and 6 not full (mostly when I was a student with bits of work in the holidays).

I thought that 35 years of full contributions were needed for full pension? How can I qualify with 28 +2?

Probably doesn't make any difference as I'm likely to be working long enough to get more than enough, but am curious.If you really want to satisfy that idle curiosity post up the following anonymous information from your forecast and NI record and someone will tell you exactly how you arrived at your current situationCurrent weekly £££.pp amount up to April 2025.

Number of full NI years 15-16 and earlier.

Number of full NI years 16-17 and later.

Any COPE amount. If you have "You've been in a contracted-out pension scheme" on your forecast then click

here https://www.tax.service.gov.uk/check-your-state-pension/account/cope whilst logged into your tax account

Never been contracted out.

2016 on - 9 years

2015 and before - 19 yearsAnd the third important bit ?Current weekly £££.pp amount up to April 2025.0 -

Here are the calculations

I came, I saw, I melted7

I came, I saw, I melted7 -

So, you do indeed only need two more years of NI contributions to take you to the (current) nSP of £230.25, despite only having 30 years.

No doubt you will be told by pre 2016 pensioners that you are 'lucky' to have this amount, while they are on a lower rate. But, the truth is, you are one of the losers under the new pension scheme. Had SERPS/SP2 not ended in 2016, you would have gone on accruing more earnings related additional State pension, instead of being capped at the nSP amount.

3 -

While I may only need 30 years, it's not like I can stop paying NI anyway! I guess that psychologically it may be nice in a year and a half to know I'll eventually get a full state pension, but it's not going to change behaviourSilvertabby said:So, you do indeed only need two more years of NI contributions to take you to the (current) nSP of £230.25, despite only having 30 years.

No doubt you will be told by pre 2016 pensioners that you are 'lucky' to have this amount, while they are on a lower rate. But, the truth is, you are one of the losers under the new pension scheme. Had SERPS/SP2 not ended in 2016, you would have gone on accruing more earnings related additional State pension, instead of being capped at the nSP amount.1 -

Where does that calculation come from?SnowMan said:Here are the calculations0 -

It's just a spreadsheet I created some time ago to do the calculations based on the 4 inputs at the top.FIREDreamer said:

Where does that calculation come from?SnowMan said:Here are the calculationsI came, I saw, I melted2 -

ImpressiveSnowMan said:

It's just a spreadsheet I created some time ago to do the calculations based on the 4 inputs at the top.FIREDreamer said:

Where does that calculation come from?SnowMan said:Here are the calculations2 -

People think there is some sort of black magic in calculating the state pension top ups and working out the viability of pre 2016 contributions but it is in fact pretty straightforward maths using the 4 points at the top of SnowMan's table. I similarly drew up a spreadsheet which does the same thing but not as pretty as SnowMan's.1

-

@SnowMan That's impressive

The above calculations show zero figure for COPE ------> does that mean the person was always opted in? (i.e. never opted out).

The reason i ask about the COPE is i don't think i have a cope figure (just like your example) but my friend does yet both our state pension maximum figures are the same i.e. £230.25

She got the following figures from her Gov Gateway:- (could you do a calculation please)

9 years

22 years

NI Record = £224.37

COPE = £22.70

EDIT - Ignore below this line-----------------------------------------------------------------------------------------------------------------------------------If she opted out and got COPE and i stayed opted in, why do i not get more than £230.25 (i think im opted in as i cant find a COPE figure)

NOTE TO MYSELF:

When calculating your new State Pension amount, the government compares what you would have received under the old rules (basic plus additional pension) with what you would receive under the new rules. If your "starting amount" under the old rules was higher than the full new State Pension amount, you receive a "protected payment" which is paid on top of the £230.25 rate. This is the only way to get more than the full new State Pension amount. --------> my starting amount under the old rules must have been lower than the NEW full state pension in tax year 2015/2016 when the change happened.

However in the example above the person also has zero COPE and it shows OLD rules are higher than NEW state pension amount so will this person get more than £230.25 when they come to retire?I have a tendency to mute most posts so if your expecting me to respond you might be waiting along time!0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards