We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

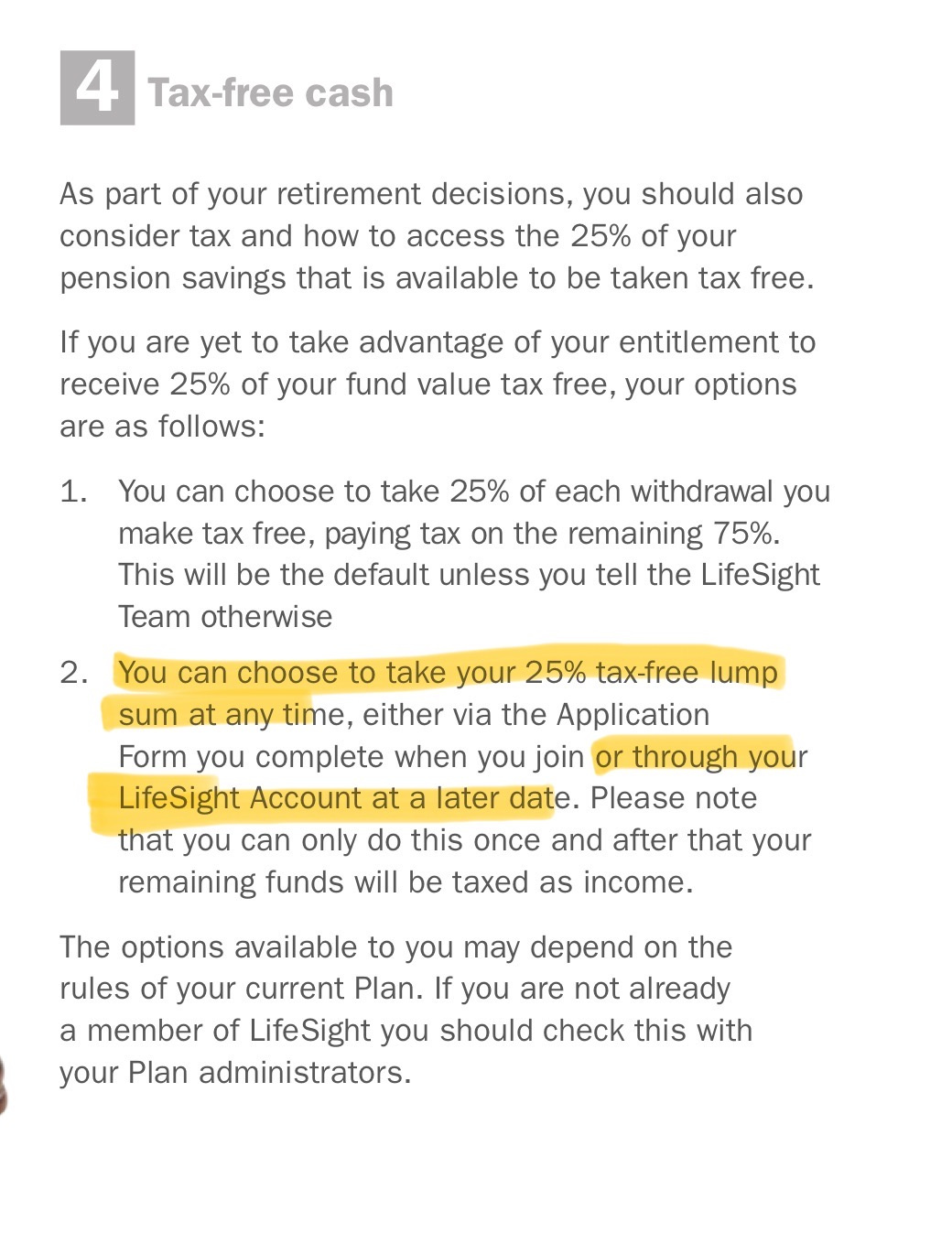

CAN I STILL GET UP TO 25% TAX FREE?

Comments

-

Thanks everyone for the help and advice. I will be asking WTW about transferring to another scheme.0

-

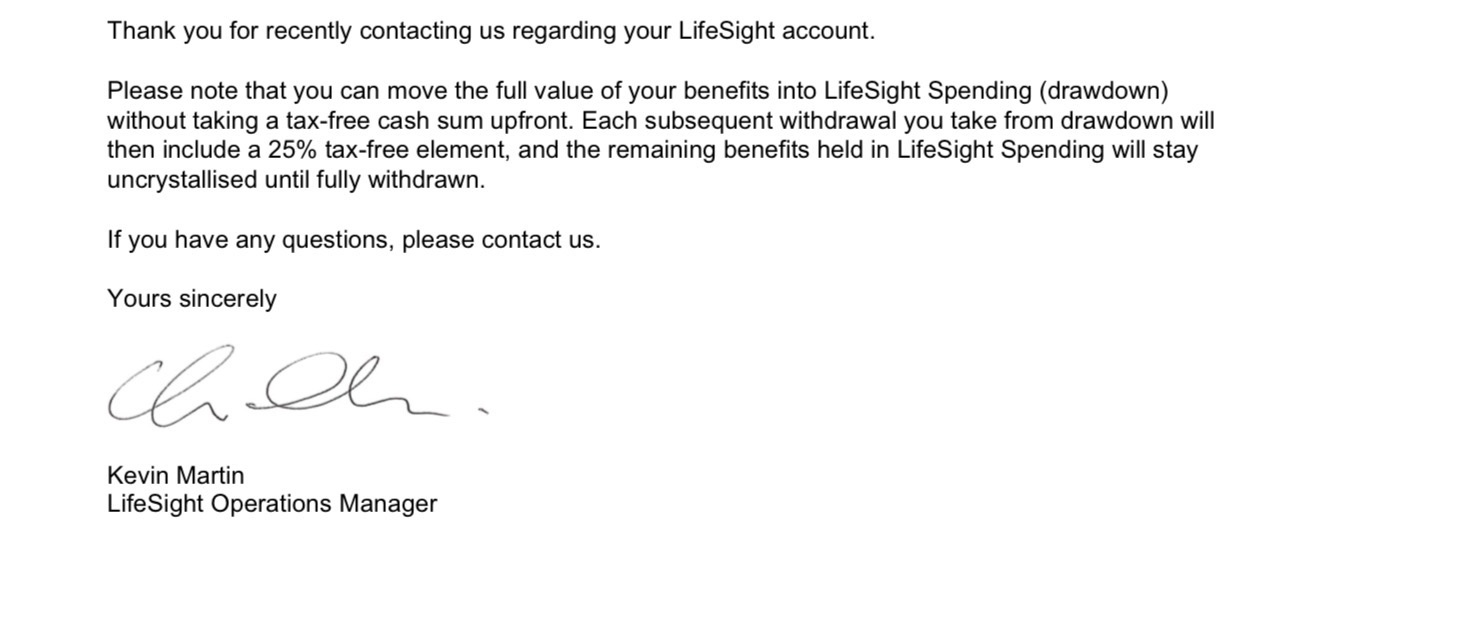

This can't be correct - if funds were crystallised on taking the first payment then how come they've made subsequent payments for 3 years with 25% tax free. That is only possible from uncrystallised funds.NOT_THE_TAXMAN said:OK I've now done some further checking with WTW (and waited the usual time for a response). WTW confirm that my "funds were crystallized when you took your first withdrawl from scheme". I have no knowledge or recollection of ever being told this, prior to taking any withdrawl. Now, previous to WTW, the Pension provider was Lifesight. I still have the documentation and have now been through everything provided to explain my options before taking my pension. AT NO TIME WAS IT MADE CLEAR THAT IF I STARTED MONTHLY WITHDRAWLS THAT I WOULD LOSE THE 25% TAX FREE IF I DIDN'T TAKE IT ALL BEFORE STARTING WITHDRAWLS. It does appear that I had very poor and incomplete advice from Lifesight on what options were available. So that's where I am. I would be grateful for any advice on whether I can challenge the "poor advice" given at the time by Lifesight, in order to be able to take my remaining 25% without touching the remaining fund. Also any advice on whether the Pensions Ombudsman may be any help in this matter.

Thank you in advance

David

You need to get back to them and get someone who knows what they're talking about. Some providers (WTW is one IIRC) complicate matters by transferring funds into a separate account for drawdown, but that separate account isn't necessarily all crystallised funds.0 -

Just bumping this thread because I have been trying to clarify with WWT how they treat crystallisation events within LifeSight. Their online documentation is somewhat 'dumbed down' with regards to how their drawdown product works and fails to mention crystallisation anywhere, not even in their 'tax help' leaflet.

Anyway I emailed seeking clarification and after a couple of attempts (1st attempt completely failed to address my question) finally got what I think is a straightforward clear answer:

so their drawdown product is essentially a flexi-access drawdown with only the withdrawal amounts being crystallisations.

@NOT_THE_TAXMAN did you ever get a clear answer yourself?

I will of course be saving this letter for future reference….0 -

Its not flexi access drawdown at all, it's all just UFPLS withdrawals, from their description.

3 -

According to the key features guide you can take your tax-free cash at any time so that would be FAD wouldn't it?

EDIT: re-reading it you might be right as can only ever take one tax free lump sum.

0

0 -

Curious if anyone on here is already taking LifeSight Drawdown - what does it show in your account?

0 -

I was responding to your initial response from Kevin Martin, where that description is just UFPLS.

The first option is UFPLS.

The 2nd option is sort of Flexi drawdown, but it applies to your whole pot at the time you do it, so you get the tax-free cash and the rest of the pot is crystallised. So any further withdrawals are taxable. True FAD would allow you to do this in chunks.

1 -

Thanks, every time I read it I interpret it differently!

You would have thought that pension providers have an obligation to clearly and unambiguously describe how they apply the tax and scheme rules. WWT literature seems to be trying to explain things in an easy to understand way but just ends up being even more confusing…

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards