We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Which fund to lock in annuity value

Comments

-

Have you bought individual gilts or a fund?Alexland said:

The IL gilts should still give around 20% growth above inflation in the next decade so it's only giving up the possibility that equities outperform that. Given current elevated stock market valuations that's looking less likely than in normal times but who knows we might see the valuations resolved by excellent earnings growth.dawsonrm said:I'm reluctant to give up 10 years of "possible" growth but with current equity values (the 200k is currently 100% in a global index tracker) and good annuity yields, being able to lock in the current value seems a sensible thing to do. If an AI bubble does burst no guarantee it's gonna recover before she's 58.

I am doing similar and have recently converted a proportion of my pensions into IL gilts to assure my current level of annual spending for early retirement starting in around a decade's time until old age0 -

So far I have used a workplace pension fund and an ETF in my main SIPP.dawsonrm said:Have you bought individual gilts or a fund?

My main SIPP provider doesn't support buying gilts directly (and I need to stay with them for my protected early access age) so I have opened another SIPP elsewhere and am in the process of partially transferring 99% of my workplace pension into that SIPP so I can build a gilt ladder that aligns to my retirement period and includes plenty of those those >2% pa longer dated IL gilts.1 -

FWIW, my view is that decision should be based on the consequences of getting it wrong.

For example, if the goal is to secure a certain level of income at retirement

1) Leave in equities - if real annualised growth is above about 2% (see post by @Alexland) then you will have more income than currently expected. If real growth is less than 2%, then you will have less income than currently expected (e.g., worst historical case over 10 years for 50/50 UK/US equities was an annualised real return close to -5%, while the 25th percentile was +4%). Will a very poor market affect your retirement plans?

2) Lock in current expected income. Assuming the expected income is good enough, you will give up potential growth - does that matter to your plans?

I note that building the ladder/putting aside for fixed term annuity purchase will take about half the £100k pot, so the other £100k is still available for potential growth.

Not an easy decision!

edit: Option 1 (leave in equities) also runs interest rate risk in the sense that yields might be lower than now (or higher). For a 10 year ladder/annuity this could make some difference. For example, going from a 5% yield to 0% yield changes the payout rate from 12% to 10%, i.e., 20% difference in income.

2 -

Alexland said:

The IL gilts should still give around 20% growth above inflation in the next decade so it's only giving up the possibility that equities outperform that. Given current elevated stock market valuations that's looking less likely than in normal times but who knows we might see the valuations resolved by excellent earnings growth.dawsonrm said:I'm reluctant to give up 10 years of "possible" growth but with current equity values (the 200k is currently 100% in a global index tracker) and good annuity yields, being able to lock in the current value seems a sensible thing to do. If an AI bubble does burst no guarantee it's gonna recover before she's 58.

I am doing similar and have recently converted a proportion of my pensions into IL gilts to assure my current level of annual spending for early retirement starting in around a decade's time until old age.I've done the same recently, sold off a chunk of my pension to buy IL gilt fund at around 2% real yield.I am already retired in my 40s so no income and no DB pension either. Makes sense to lock an income in rather than having to rely overly on equities (I was 80% equities prior to the change). I might be doing it early given I can not access my pension for at least 10 years, but the concern I have is we might see a severe stock downturn given how much valuations and speculation has driven the market prices recently.If equities continue to rip higher (+30% or more from here), I'll probably sell the lot in my pension and reinvest in the IL fund, providing me with a guaranteed income from 55 that covers more than my basic spending. I'll also consider buying more equities when the eventual downturn does happen from the cash/bonds in my ISA.Its better from a tax perspective too to shift growth assets from pension to ISAs.2 -

Thanks for that interesting thoughts.OldScientist said:FWIW, my view is that decision should be based on the consequences of getting it wrong.

For example, if the goal is to secure a certain level of income at retirement

1) Leave in equities - if real annualised growth is above about 2% (see post by @Alexland) then you will have more income than currently expected. If real growth is less than 2%, then you will have less income than currently expected (e.g., worst historical case over 10 years for 50/50 UK/US equities was an annualised real return close to -5%, while the 25th percentile was +4%). Will a very poor market affect your retirement plans?

2) Lock in current expected income. Assuming the expected income is good enough, you will give up potential growth - does that matter to your plans?

I note that building the ladder/putting aside for fixed term annuity purchase will take about half the £100k pot, so the other £100k is still available for potential growth.

Not an easy decision!

edit: Option 1 (leave in equities) also runs interest rate risk in the sense that yields might be lower than now (or higher). For a 10 year ladder/annuity this could make some difference. For example, going from a 5% yield to 0% yield changes the payout rate from 12% to 10%, i.e., 20% difference in income.

Were pretty well covered for guaranteed income after 67 but we're hoping to retire 10 years before that so it would be nice to have some guaranteed income for that 10 year period rather than rely on the vagaries of equity values.

The conventional idea of derisking by moving from equity to bond funds doesn't appeal at all. With how bond funds got hammered recently I don't see that as derisking as theres no reason it won't happen again might as well stick with equities.

That's why I like the idea of a fixed price annuity particularly at the current rates. I guess I was hoping there might be an easy way of locking in the current annuity rates using an index linked bond fund but it seems like that's not really possible as the durations don't really match up.

I guess an index linked gilt ladder is the only real way to guarantee the income levels. I was hoping to avoid buying individual gilts as it all seemed rather complicated but I guess I'll have to get my head around it.

I'm thinking about buying a 20k gilt maturing in 10 years time every year for the next 10 years while leaving the rest in equities. If a crash does come then I could always stop buying the yearly gilts and the market has 10 years to recover before I need the money. I guess the hard part is deciding what constitutes a crash!0 -

@itwasntme001 out of interest what fund did you buy?

Isn't the fund still risky if bond prices fall as your not holding to maturity?0 -

dawsonrm said:@itwasntme001 out of interest what fund did you buy?

Isn't the fund still risky if bond prices fall as your not holding to maturity?Its the L&G over 5 years index linked gilt fund.Yes the value of the fund could fall by the time I want to annuitise it. But if the value has fallen, the real yields would have risen, and so to the annuity rates I would be able to get. So in effect I have locked in a real yield of around 2%.1 -

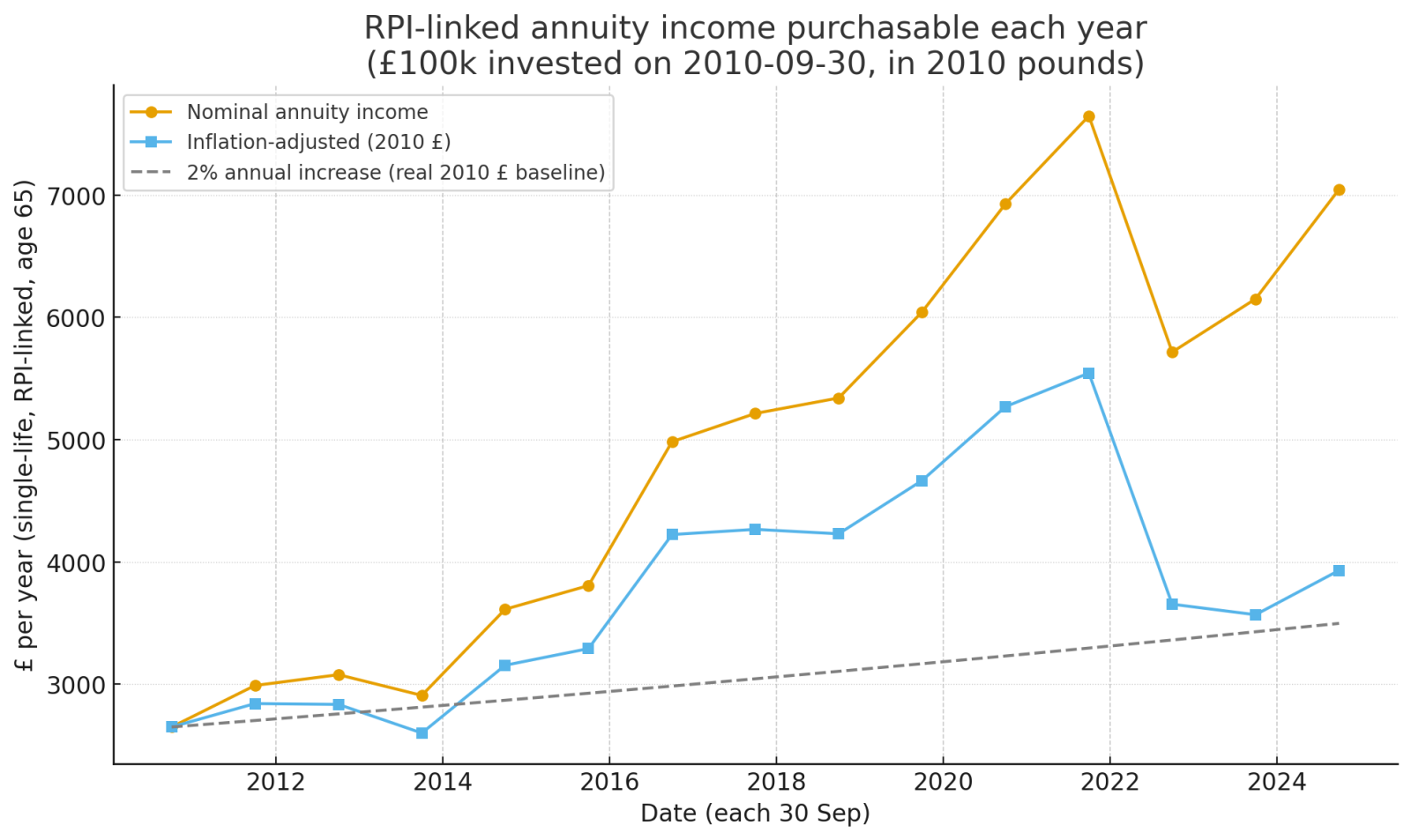

Interestingly I got chatgpt to plot a graph of how much annuity you could buy with the value of the LandG over 5 year index linked fund each year starting with 100k in 2010 and adjusting for inflation.

Assuming it's done it correctly it shows a lot of variation in what you would have got depending when you bought the annuity. This definitely makes me think the only real way to lock in current prices is with a gilt ladder.

1 -

Its never meant to be a perfect hedge. Prior to 2022, we had negative real yields, and bonds were in a bit of a bubble, so you could get a lot more income even though annuity rates were low.Now that bonds have crashed back to more "normal" levels, annuity rates have gone up but the value fell so much that the income is quite a bit lower.When rates fall to close to 0, the way the bond math works results in widely volaitle pricing as yields change. Now that yields have normalised, you won't see such large swings, and the hedge works better.That said, if we ever do see 0 or negative real yields again, I'll either move ot cash or buy up equities if they offer value. With bonds, it is much easier to determine if they offer value than it is to determine whether equities are.2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards