We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Royal London GPP - Entire pension re-invested into higher risk fund without consutation.

vacheron

Posts: 2,700 Forumite

Hi all.

Quite a long post, so please bear with me (I also have to spread this over multiple posts as I only seem to be able to add one image per post.!

Before giving Royal London a call (which I don't feel hopeful about getting a sensible answer out of), I was wondering if some of the pension experts on here can explain to me what Royal London (RL) are doing with my Pension Contributions, as to me it looks like they are buying and selling my pension investments on a whim, and without warning or consultation.

Background:

Our company changed its pension provider to Royal London in February 2023. I elected to keep all my earlier contributions with my previous provider (Scottish Widows) and so started this Royal London pension from £0.

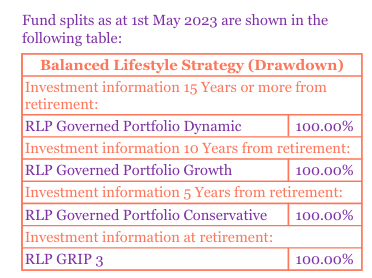

The investment strategy selected was their "Balanced Lifestyle Strategy (Drawdown)" and it still shows as this when I log in.

The issue I have noticed:

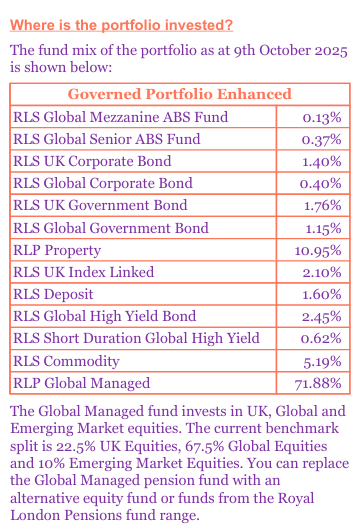

My Original welcome pack from Feb 2023 advised me that my contributions will be invested in their "Governed Portfolio 4" fund, which they defined as follows:

----continues on next post----

• The rich buy assets.

• The poor only have expenses.

• The middle class buy liabilities they think are assets.

• The poor only have expenses.

• The middle class buy liabilities they think are assets.

1

Comments

-

Before giving Royal London a call (which I don't feel hopeful about getting a sensible answer out of), I was wondering if some of the pension experts on here can explain to me what Royal London (RL) are doing with my Pension Contributions, as to me it looks like they are buying and selling my pension investments on a whim, and without warning or consultation.The Governed portfolios are a discretionary portfolio where they can make changes based on their invesmtent remit. Pretty much the same as every governed portfolio, discretionary model portfolio or multi-asset fund.

They do not require your permission and they do not give warnings or consultation. They do publish the change history for the small number of people who are interested in knowing and each month's factsheet shows the previous three changes: https://www.royallondon.com/strategyfactsheets/strategyfactsheet.asp?InvestmentType=G&strategyid=LAV

They also explain the rationale on their website. here is the latest:

https://adviser.royallondon.com/articles-and-guides/investment/SAA-updates-to-Governed-Range/The investment strategy selected was their "Balanced Lifestyle Strategy (Drawdown)" and it still shows as this when I log in.That is the risk adjustment strategy but not the portfolio name. The Balanced Lifestyle Strategy invests in the appropriate governed portfolio based on your timescale to scheme age:

https://www.royallondon.com/strategyfactsheets/strategyfactsheet.asp?InvestmentType=F&strategyid=726262

Again, that is quite normal across providers. Indeed, your existing SW pension probably did the same but used multi-asset funds with blending (that is what most of the SW workplace pensions do - although there are multiple SW workplace pensions).

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.6 -

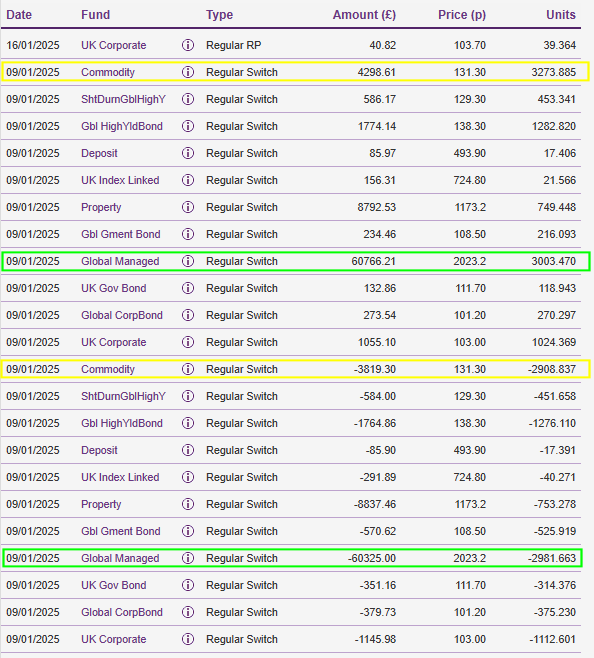

In around february this year, they changed the naming of these somewhat illogicaly numbered portfolios to something that made more sense. This also meant that instead of my transaction history showing purchases of every individual investment in the portfolio above individually each month, it now just showed one single purchase of the newly named portfolio which made the transaction history far easier to follow.

However.. on the 17th of July, RL were at it again and once more the my enitre "GPF Enhanced" fund was sold and replaced with a "GPF Dynamic" fund (with a different unit price) and after some messing about in August, Things have now settled down with all my contributions going into this "GPF Dynamic" fund.My Concerns are:RL appear to have switched me over from the "Enhanced" (originally Governed Portfolio 4) fund, which they have rated a 4 out of 7 for risk, to the "Dynamic" fund (rated 6 out of 7 for riskwithout informing me.They have also decided to sell ALL of my previous contributions to the original "Enhanced" fund and use entire proceeds to re-invest in their "Dynamic fund", again with zero consultation or warning.I was continuing under the assumption that I was in a fund with 69% equities and 8% bonds, whereas I am now in a fund with 80% equities and 2.5% bonds. Is is common practice for a pension provide to just change your risk profile without changing the name of the pension strategy? And also to retrospectively sell all your previous investments and re-purchase with the proceeds from these too?• The rich buy assets.

• The poor only have expenses.

• The middle class buy liabilities they think are assets.1 -

This is exactly what I am planning to do.Marcon said:Instead of posting here, why not set about switching your investments into funds you'd prefer?

My reason for investigating this more closely was because I was planning to make a partial withdrawl and invest the money in a SIPP using ETF's which would initially replicate the governed portfolio 4 allocations (as I was happy with that before they started messing with it).

This would allow me to quickly change the respective ratios, and more importantly now as it appears, retain full control to know what I am actually invested one month later!• The rich buy assets.

• The poor only have expenses.

• The middle class buy liabilities they think are assets.1 -

I was continuing under the assumption that I was in a fund with 69% equities and 8% bonds, whereas I am now in a fund with 80% equities and 2.5% bonds. Is is common practice for a pension provide to just change your risk profile without changing the name of the pension strategy?That is barely a change in risk profile, and yes, it is commonplace. Your SW pension probably did it too. Albeit within the multi-asset fund. Asset ratios on multi-asset solutions are rarely static. They will adjust the equity/bond/property/cash ratios within a defined risk band (or target volatility band).

Risk is diluted by timescale. So, 80% equities for someone 15+ years away is lower risk than say 60% equities for someone 5 years away.

On a typical 1-5 risk scale, 69% equities and 80% equities would fall under the same risk scale.

However, GP Enhanced has the current fund mix:

In your case, your choice to use a lifestyle risk strategy means you go higher risk the further away you and reduce risk as you get closer.

Are you sure you are still in the GP enhanced? Since the last tweak, GP enhanced isn't in the lifestyle strategy any more.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

You didn't give me a chance to offer my follow up post!dunstonh said:Before giving Royal London a call (which I don't feel hopeful about getting a sensible answer out of), I was wondering if some of the pension experts on here can explain to me what Royal London (RL) are doing with my Pension Contributions, as to me it looks like they are buying and selling my pension investments on a whim, and without warning or consultation.The Governed portfolios are a discretionary portfolio where they can make changes based on their invesmtent remit. Pretty much the same as every governed portfolio, discretionary model portfolio or multi-asset fund.

They do not require your permission and they do not give warnings or consultation. They do publish the change history for the small number of people who are interested in knowing and each month's factsheet shows the previous three changes: https://www.royallondon.com/strategyfactsheets/strategyfactsheet.asp?InvestmentType=G&strategyid=MBL

RL Governed Portfolio 4 has been renamed to Governed Portfolio EnhancedThe investment strategy selected was their "Balanced Lifestyle Strategy (Drawdown)" and it still shows as this when I log in.That is the risk adjustment strategy but not the portfolio name. The Balanced Lifestyle Strategy invests in the appropriate governed portfolio based on your timescale to scheme age:

https://www.royallondon.com/strategyfactsheets/strategyfactsheet.asp?InvestmentType=F&strategyid=726262

Again, that is quite normal across providers. Indeed, your existing SW pension probably did the same but used multi-asset funds with blending (that is what most of the SW workplace pensions do - although there are multiple SW workplace pensions).") (due to PC issues and a delivery making posting it take longer than I expected)

(due to PC issues and a delivery making posting it take longer than I expected)

I can completely understand blending and re-balancing (indeed I could see the re-balancing at work prior to February this year as all the investments in the portfolio were shown as separate purchases), but since the name change, they just now report as a single "Governed Portfolio Enhanced" purchase (with the rebalancing all taking place inside I would assume).

What I can't understand is why they would publish the composition of the portfolio in (GP4) your welcome pack, and then without warning switch you to a different portfolio (equivalent to GP7) without even letting you know. And selling down your entire previously accumulated investments to do so!

• The rich buy assets.

• The poor only have expenses.

• The middle class buy liabilities they think are assets.1 -

I appreciate that a 15% increase in equities and a 70% reduction in bonds may be "barely a change" to many, but hypothetically is there any kind of backstop to prevent them making larger changes in the future?dunstonh said:I was continuing under the assumption that I was in a fund with 69% equities and 8% bonds, whereas I am now in a fund with 80% equities and 2.5% bonds. Is is common practice for a pension provide to just change your risk profile without changing the name of the pension strategy?That is barely a change in risk profile, and yes, it is commonplace. Your SW pension probably did it too. Albeit within the multi-asset fund. Asset ratios on multi-asset solutions are rarely static. They will adjust the equity/bond/property/cash ratios within a defined risk band (or target volatility band).

In your case, your choice to use a lifestyle risk strategy means you go higher risk the further away you and reduce risk as you get closer.

As RL considered "Enhanced" (GP4) a 4/7 risk rating, and "Dynamic" (GP7) a 6/7, they certainly considered it to be a change in risk profile?

I don't want lifestyling either, but I knew 3 years ago that I was happy with the composition of the portfolio as it was provided to me at the time. The reason I am delivng deeper now is because I know the shift to Governed portfolio 5 (Growth) is approaching so I was going to ask them to leave it where it is... but now I have realised that it isn't where I left it anyway! • The rich buy assets.

• The rich buy assets.

• The poor only have expenses.

• The middle class buy liabilities they think are assets.1 -

I appreciate that a 15% increase in equities and a 70% reduction in bonds may be "barely a change" to many, but hypothetically is there any kind of backstop to prevent them making larger changes in the future?Yes.

Leave the lifestyle strategy and self select your funds.As RL considered Enhanced a 4/7 risk rating, and Dynamic a 6/7, the certainly consider it to be a change in risk profile.The 1-7 SRRI scale used for KIIDs is rarely used outside of the KIID. It is a synthetic risk and reward scale. It has quirks that lead to some assets overstating or understating risks. Its also quite a static scale with infrequent updates. So, don't put much weight on that.

Any risk scale will have lines in the sand where you could be just one side or the other but when it is a scale of 7 with no decimal places, it doesn't give much context.

For example, I use a 0-5 scale with time weightings. The scoring band for risk 4 is 3.50 to 4.49.

RLI Governed Portfolio Enhanced Pension is 3.67 for 21+ years

RLI Governed Portfolio Dynamic Pension is 4.40 for 21+ years.

Both fall in risk 4. Yet thanks to decimal places, you can see where they sit within that band.

However, on a different day, one could be risk 3 and the other risk 5. Capital market assumptions change (anything from quarterly to annually). Risks associated with different assets changes, and then you have portfolio drift, and the point at which they decide to rebalance it back. A 70% equities portfolio will often allow upto 10% drift before being rebalanced back. So, on a live risk scoring system you see those changes as they happen. However, on a synthetic snapshot based on assumptions you will not.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.5 -

Yes. As per my response to Macron's original post the reason I have been digging deeper recently is because I was planning to do exactly that, and what I have seen has certainly not dissuaded me from that path.dunstonh said:I appreciate that a 15% increase in equities and a 70% reduction in bonds may be "barely a change" to many, but hypothetically is there any kind of backstop to prevent them making larger changes in the future?Yes.

Leave the lifestyle strategy and self select your funds.

Thanks again dunstonh, really useful insights as always. 👍Risks associated with different assets changes, and then you have portfolio drift, and the point at which they decide to rebalance it back. A 70% equities portfolio will often allow upto 10% drift before being rebalanced back. So, on a live risk scoring system you see those changes as they happen. However, on a synthetic snapshot based on assumptions you will not.

One thing I did notice during my deeper dive is that RL did appear to be re-balancing regularly, but according to the transaction history the way RL appeared to re-balance (prior to the GP4 - Enhanced renaming) seemed to be by selling the full amount of every single holding (often more than once per month), and then buying back the entire same holdings again, at the same unit price, but with slightly different quanitites.

I was at a loss to understand why they didn't just buy or sell the difference required for each fund , but I am certain that there must be a logical reason for doing it this way, is it perhaps so that they know exactly what the full lquidated value is before the calculate the amounts of each holding to rebuy as percentages?

Regardless though, this certainly makes for a lot of transactions to wade through and make sense of. Especially when they were sometimes doing this twice (or even three times) per month!

• The rich buy assets.

• The poor only have expenses.

• The middle class buy liabilities they think are assets.1 -

I was at a loss to understand why they didn't just buy or sell the difference required for each fund , but I am certain that there must be a logical reason for doing it this way, is it perhaps so that they know exactly what the full lquidated value is before the calculate the amounts of each holding to rebuy as percentages?Whilst it is becoming increasingly common on modern software for rebalancing or adjustments to use just the difference in the areas short or over target, it used to be the case, with many providers, that the entries moved out entirely and then back in again using the revised weightings. Royal London's personal pension is actually the old Scottish Life pension rebranded using software from that period. It does what it is meant to do, but it does it in an early 2000s way.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

This is really interesting! So in January I moved mine into a higher risk profile, received the confirmations in the post, all ok. Well done I thought.Last month when checking my investments, and payments had been credited I noticed that the investments were 100% in equities which was not the selection I had made, or was confirmed in writing.

Contacted RL, they failed the answer how, why and what the impact is, so I sent a follow up communication, still nothing back from them - I called yesterday and the enquiry had been closed down 🤬, hence the no response. It’s now been escalated and I’m waiting for more contact.

So it’s interesting to hear that someone else has the same thing happen with RL. I’ll update this thread when I have an outcome.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards