We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Kingfisher Pension Quote

Whiterose23

Posts: 269 Forumite

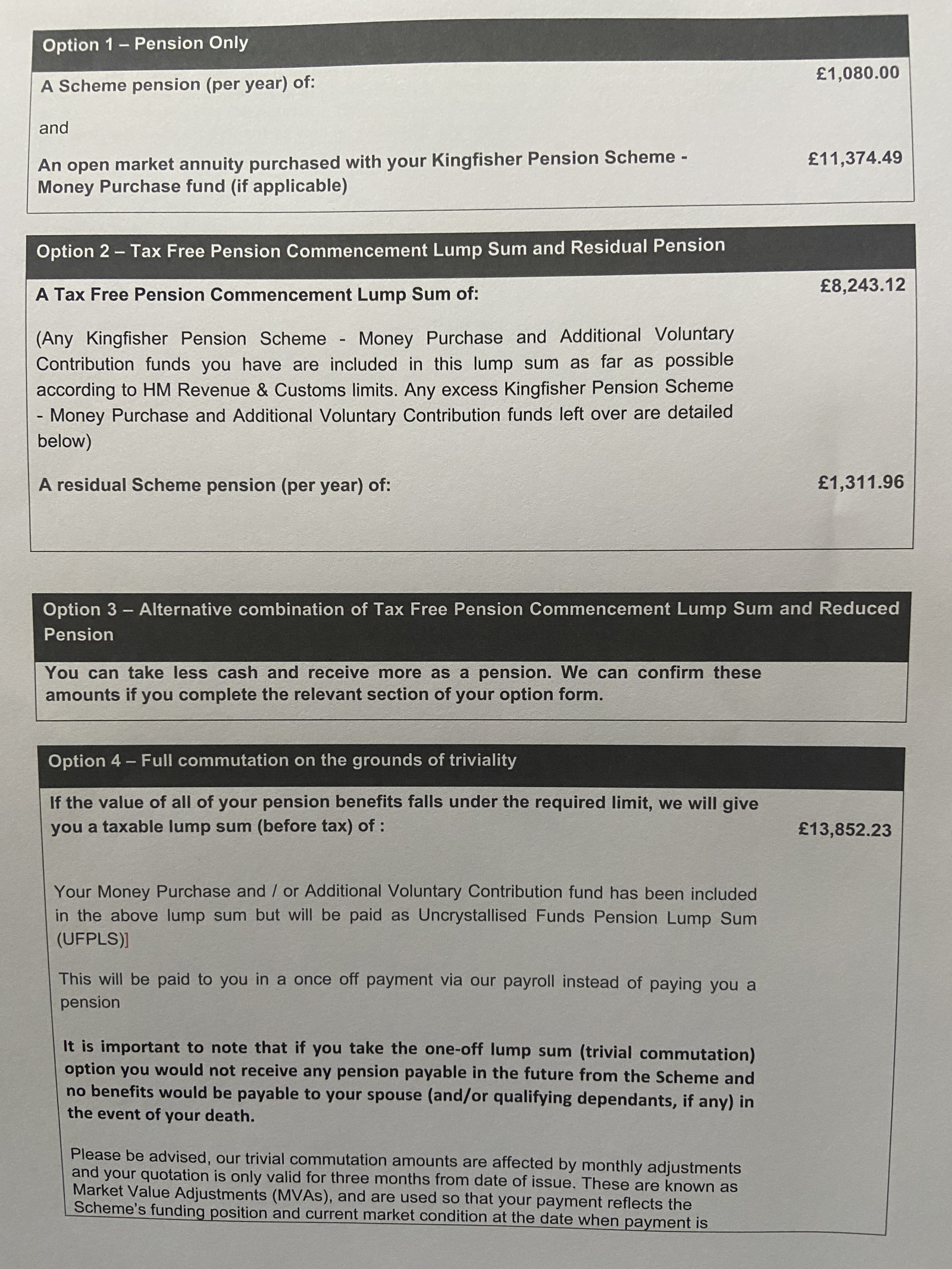

Hi, I have a tiny deferred pension with Kingfisher and have been provided with a quote with 4 options.

I would like to take a lump sum with a yearly pension (Option 2), but I’m confused about Option 1 which indicates it’s just a pension payment and no lump sum, but has a lower annual pension amount and a lump sum that would be used - as I understand it - to provide a top up by buying an annuity?

Please could anyone confirm this? And also which option, in your opinion would be the best one? I’m assuming £11,374 wouldn’t buy very much in terms of an annuity ..?

Also Option 4 seems very low when online the cash in value states that it’s £22,000 plus. Any insight would be gratefully received.

Thanks

Also Option 4 seems very low when online the cash in value states that it’s £22,000 plus. Any insight would be gratefully received.

Thanks

0

Comments

-

Opt 1 a KF pension of £1080 pa and purchase an annuity with £11374 which will give maybe around £700 pa incomeOpt 2 a KF pension of £1312 and a lump sum of £8243Opt 3 variations on opt 2Opt 4 a lump sum of £13852It would seem that option 3 with max pension & low lump sum may be the most beneficial as the rate looks to be in your favour.The £22K v £13.8K seems a bit strange1

-

i had a very similar offer out of the blue from a small old Securicor pension, similar amounts to yours actually, ended up taking some tax free cash and reduced annual pension from the point i chose it i was 57 at the time , key to my choice was a permanent , annual increase of 5% and spouse benefit of 50% for life, so i'd check the additional benefits of each one , whether there are increases etc, think i took about 8k with an annual reduction of £200 was well worth it at the time.1

-

It would seem that option 3 with max pension & low lump sum may be the most beneficial as the rate looks to be in your favour.

OP might wish to check if the pension increases in payment and if so how.

For example, is any part of it pre 88 GMP?

With regard to option 4, presumably there is the 25% tax free lump sum with balance taxable as income in year of receipt?

OP should check.

He should also check on discrepancy in amounts.

1 -

How can you tell?molerat said:Opt 1 a KF pension of £1080 pa and purchase an annuity with £11374 which will give maybe around £700 pa incomeOpt 2 a KF pension of £1312 and a lump sum of £8243Opt 3 variations on opt 2Opt 4 a lump sum of £13852It would seem that option 3 with max pension & low lump sum may be the most beneficial as the rate looks to be in your favour.The £22K v £13.8K seems a bit strange0 -

Re: Opt.4, it says "if the value of all your pensions falls under the required limit...."My understanding is that the limit is £30,000 https://www.gov.uk/hmrc-internal-manuals/pensions-tax-manual/ptm063500If the OP has other pensions, then option 4 may not actually be available.

0 -

A couple of things to check:

1) The annual rate of increase in payment

2) Whether the spouse benefit is based on the basic pension or the pension after any lump sum taken.

My small DB pays a 50% pension based on the higher annual pension (i.e., no lump sum taken) so it was worth my while to take a lump sum at a commutation rate of 22 (which on a quick calc looks similar to your KF offer).

Also take into account what your tax situation will be once all taxable incomes are in payment, i.e., SP and any other DBs.

Final point - option 4 looks to be a really poor choice.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.7K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 246.8K Work, Benefits & Business

- 603.3K Mortgages, Homes & Bills

- 178.2K Life & Family

- 260.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards