We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Tax Free Lump Sum and 2025 Budget

Comments

-

Hi, thank you so much for the suggestion. I searched and found this on the forum.MK62 said:

You would seem to be an ideal candidate for an index linked gilt ladder..........roadweary said:I’m 55. About 800k in my pension.Plan was to work full time to 60, 4 days a week for another couple of years - then take 40-50k a year tax free till state pension contributes.I don’t have any ‘tax/growth sensible’ vehicles available should I take my 200k now.I’m risk averse and about as conflicted as I could be as to whether I withdraw some or all of the 200k now. https://youtu.be/UqrO9Wi6rSY In so much as I understand from that, I like the idea and the fact that you can buy something, know the price on maturity and have a good idea of the income generated.

https://youtu.be/UqrO9Wi6rSY In so much as I understand from that, I like the idea and the fact that you can buy something, know the price on maturity and have a good idea of the income generated.

A whole bunch of questions, sorry.

I didn't see any explanation of tax liability. So, tax on the 6-monthly interest of a UK bond? And if the bond were bought (using their examples) at £70 but it will mature at £100, what are the tax liabilities on that?

If you pay Capital Gains on it, isn't that potentially just as expensive (or more) as leaving it in the pension and then getting charged income tax as you draw down on the funds if the tax free allowance has gone?

And the 6-monthly interest....is that shielded from tax as long as you re-invest back into the fund...or do you get charged CGT/income tax on that interest?

Then the big one is....what are the costs (apart from time) of doing this for yourself? Do you have to pay to buy / sell / report on what you've done?

Next, the time part.....is this something where I can practically say, I'm going to invest 50k on bond A that matures in 7 years' time, 50k in bond B that matures in 8 years' time, 50k for Bond C - 9 years, 50k bond D 10 years? That's probably manageable. It seems like it might not grow as much as the pension fund....but then it seems guaranteed that it can't lose - or am I missing something there?

And is this all self-done, or can you pay just small fees for a trusted party to do this for you? But what is small and who do you trust")

Sorry for all the questions, but this sounds very interesting....and if I did decide to do it, I'd be investing 200k before the budget, so I need to get pretty savvy pretty quickly!0 -

RogerPensionGuy said:

It would be interesting to hear from any hard working people that got caught in 2010s zone of the LTA going up happy daze, but then reduced & reduced, it could of been hard to navigate decide what to do.HedgehogRulez said:

Sounds like me. I’m 46 with £860k in dc pension. Don’t intend to die for another 4 years though.RogerPensionGuy said:

Noted and good point, example of a hard working person with a big pension at say age 45 and they chop the LTA down with inflation going up, dies the hard working person stop pension contributions to maintain old LTA or keep doing contributions, very tuff decisions like asking employers to stop making company contributions, the LTA was completely bonkers in my head.artyboy said:

But when those LTA/TFLS reductions happened, there was at least the option to protect what had been built up to that point, albeit with the requirement to no longer pay into a pension.RogerPensionGuy said:

A great example of how much was taken from hard working people who saved well in to pensions for so many years.Silvertabby said:

And I don't recall a media fuss over the reduction of the maximum tax free lump sum from its peak at £450K to its current £268K, although there is a lot of speculation about what may happen to it in the coming budget.LHW99 said:westv said:

The media would put that righf.Cobbler_tone said:I think a levy on pension funds would be an easy one as the average Jo/Joe wouldn’t have a clue what that meant.

Not that many in the media picked up on Gordon Brown's cutting of dividend credits to pension funds.

The LTA was 1.8M and TFLS 25% was 450K as per the rules.

However time went by and inflation rolled on.

Then the LTA was reduced to 1M and TFLS 25% obviously reduced to 250K.

People's life & pension planning was ignored, as a minimum the old values could of been held up and rises only maybe 75% if inflation, but nothing of the like was adopted, it was just chopped.

A total mess and removed lots of confidence about pensions.

As mentioned, all this achieved and very very little press or backlash.

Unless Income Tax, NI or VAT is increased, it's looking like multiple levers will be used, housing and pensions are nice convenient easy levers and they will generate a reasonable Tax Take without too much upset generaly I feel.So there are people (and I've seen some posts on here) that have protected TFLS in excess of the current £268k that can still be taken.It might come across as a bit "I'm alright Jack" but in the event there were any further draconian reductions to TFLS, I'd hope there would at least be some transitional protections for those that are already close to taking it ,and may well have planned for it to pay off mortgages or other debts).

This government has already changed the rules to take a huge chunk out of my estate, so while you may not sympathise, you may at least understand just how hacked off I'll be if they come back for a second bite.

But mostly noticed also, it was also a nice touch that lowering LTA down against inflation going up had lesser effects on DB and obviously government workers.

Altho I have just now removed my full 268 TFLS as I had enough, I'm 99% feeling it won't be reduced and if it was they would indeed put in more protections that DC SIPP people need to navigate again.

Luckily for me I was far away/lower from the horrible LTA bonkers zone and set going over the M1 limit by maybe 5 to 10% as a margin of common sense.

Then saw the 1M limit go to M1.03 then M1.05 and then M1.073 and I was lucky due age and circumstances that I pushed a bit more in keeping that 5% 10% over limit in my mind as had it reduced yet again I was probably going to stop inputs and lose 10% employer contributions effectively, I was probably 10% over LTA when I stopped employment so I was again just lucky due personal circumstances.

The LTA treatment was an utter shambles, I was only slightly affected as I reduced pension input the last few years of employment and did less overtime as 40%Tax/2%NI (42%) didn't fit well in my head, my employer was unhappy and upped overtime deals to entice others/me to do overtime due lack of suitable staff.

Then the LTA was cancelled and that had the effect on my of leaving my SIPP cooking again due personal circumstances.

I think shambles is probably too nice a word for the LTA treatment.

I was lucky and thankful, but I really feel for people who had their hard work, planning and prudence totally disrespected by the system.It is interesting to see things from the perspectives of people in different positions.In my own case, the LTA reductions were a threat, but one I could mitigate nicely by taking DB pensions early - the simplistic LTA assigning the same value to a pension paid from age 55 as a pension of the same amount paid from 70. Then just as it would have constrained my pension saving, it was removed.Pension freedoms in 2016 was a great change for me, meaning it was easy to use DC to augment DB pension. It also meant I could oversave in a DC pension in order to repay debts I will generate in my early 50s to benefit from tax efficiency.Annual Allowance was a challenge, but after several years of maximising savings and using carry-forward in the early to mid 2010s, my pensions had increased nicely anyhow, to around the point where I wouldn't want to save much more, so it was never a real constraint. I will probably exceed the allowance again soon, but thanks to traveling for a long time between 2022-24, I once again have a lot of carry-forward available so that isn't an issue for me.Fiscal drag is the next obstacle - I will be a higher rate taxpayer in every year from age 55, so if fiscal drag carries on then my pensions will suffer from a lack of inflation protection (with every inflation increase getting 40% taken from it, so only getting a net 60% inflation protection). The only way to combat that is to save more than needed and have a good DC pension on the side.State Pension reforms have boosted my State Pension nicely, by removing the contracted-out reduction I would otherwise have faced under the old system. The increase in age from 65 to 68 is personally unwelcome, but fine as it will mean a better fiscal position more widely, and I can cover the lost 3 years pretty easily with DC savings.I would say I fell on the lucky side of things by having a DB pension and personal circumstances. It is depressing how for the last 15 years it has all turned into a min/max game, aiming to avoid various pitfalls and to take advantage of simplicities in the system. Whereas the concerns should all be about ensuring sufficient pension and adequate inflation and investment risk management, policy change risk is a very significant factor to test plans against.0 -

I fully fully agree, my view in this zone is the people who work hard, long hours, go without and plan inside the rules only to have the goalposts moved and totally upsets all their hard work and planning etc etc.Cobbler_tone said:Always find it interesting when people make the connection of 'hard working' and being affluent. My lived experience tells me that the two are not mutually exclusive. Especially in terms of having to work hard to become wealthy. Maybe 'worked smarter' is a better term. Whilst I know some very hard workers who just make ends meet.

As for just wealthy people by chance or luck, they can often augment stuff to still achieve nice outcomes.

With so much media talk about "working people" it's just talk.

An overriding view I hold reference pensions is, they should be kept simple and not tinkered with all the time, if negative changes are made these changes should be way way down the road, maybe 30 years or more, this would allow people to focus and plan.1 -

roadweary said:I’m 55. About 800k in my pension.Plan was to work full time to 60, 4 days a week for another couple of years - then take 40-50k a year tax free till state pension contributes.I don’t have any ‘tax/growth sensible’ vehicles available should I take my 200k now.I’m risk averse and about as conflicted as I could be as to whether I withdraw some or all of the 200k now.

No. Steady as she goes. You are on a good course, why change it because of mere speculation?

What may very possibly benefit you is having some flexibility in when you stop working and how and when you take the pension benefits. Having a savings buffer (like an ISA fund) will facilitate the latter.A little FIRE lights the cigar0 -

There is no CGT on gilts........the coupons are subject to income tax as interest unless held in a tax exempt account such as an ISA. The coupons on IL gilts are typically quite low though (eg 0.125%), though there are a few higher coupon examples.roadweary said:

Hi, thank you so much for the suggestion. I searched and found this on the forum.MK62 said:

You would seem to be an ideal candidate for an index linked gilt ladder..........roadweary said:I’m 55. About 800k in my pension.Plan was to work full time to 60, 4 days a week for another couple of years - then take 40-50k a year tax free till state pension contributes.I don’t have any ‘tax/growth sensible’ vehicles available should I take my 200k now.I’m risk averse and about as conflicted as I could be as to whether I withdraw some or all of the 200k now.https://youtu.be/UqrO9Wi6rSY In so much as I understand from that, I like the idea and the fact that you can buy something, know the price on maturity and have a good idea of the income generated.

A whole bunch of questions, sorry.

I didn't see any explanation of tax liability. So, tax on the 6-monthly interest of a UK bond? And if the bond were bought (using their examples) at £70 but it will mature at £100, what are the tax liabilities on that?

If you pay Capital Gains on it, isn't that potentially just as expensive (or more) as leaving it in the pension and then getting charged income tax as you draw down on the funds if the tax free allowance has gone?

And the 6-monthly interest....is that shielded from tax as long as you re-invest back into the fund...or do you get charged CGT/income tax on that interest?

Then the big one is....what are the costs (apart from time) of doing this for yourself? Do you have to pay to buy / sell / report on what you've done?

Next, the time part.....is this something where I can practically say, I'm going to invest 50k on bond A that matures in 7 years' time, 50k in bond B that matures in 8 years' time, 50k for Bond C - 9 years, 50k bond D 10 years? That's probably manageable. It seems like it might not grow as much as the pension fund....but then it seems guaranteed that it can't lose - or am I missing something there?

And is this all self-done, or can you pay just small fees for a trusted party to do this for you? But what is small and who do you trust

Sorry for all the questions, but this sounds very interesting....and if I did decide to do it, I'd be investing 200k before the budget, so I need to get pretty savvy pretty quickly!

Assuming you held these in a general investment account, you may need to pay income tax on the coupons, unless you have spare personal allowance or personal savings allowance to offset against.......lategenexr's gilt ladder tool will show you an estimate of the likely max amount you might have to pay.

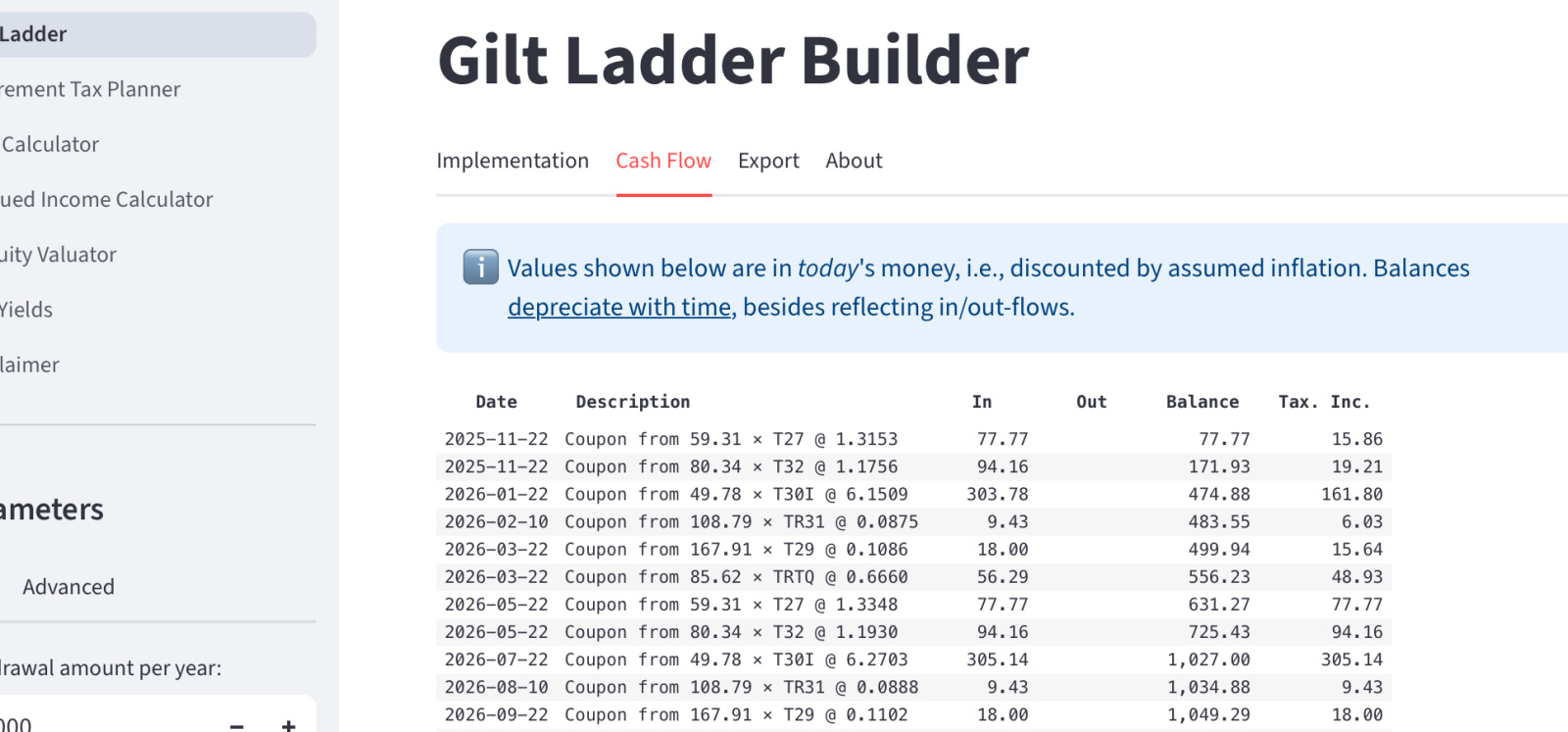

As to getting them, all you need do is open a GIA at your platform of choice and then call them to place your orders (IL gilts can't usually be dealt online, but most platforms will, AFAIK, charge you the online dealing fee, rather than the telephone dealing fee (but make sure beforehand)). Obviously the costs will vary depending on the ladder you want to build, but a 12 year ladder bought today, paying out for the final 4 years of it's life, might cost less than £50 to set up. Again, play around with lategenexr's gilt ladder tool.....it's fairly straightforward......you just need to tell it how long the ladder will last, how much you want it to payout (in today's money), when you want the payments to start, your marginal tax rate and the likely interest on cash deposits in the account (this is an unknown really, so I use 2%)......oh, and don't forget to click on "index linked". The tool will also show you the cash flow model of the ladder. Finally, while the tool is very handy, you don't have to follow it exactly......you can create your own after you see how it's done....though obviously that's more work for you (being handy with a spreadsheet is probably a prerequisite though)

2 -

Good advice.MK62 said:

There is no CGT on gilts........the coupons are subject to income tax as interest unless held in a tax exempt account such as an ISA. The coupons on IL gilts are typically quite low though (eg 0.125%), though there are a few higher coupon examples.roadweary said:

Hi, thank you so much for the suggestion. I searched and found this on the forum.MK62 said:

You would seem to be an ideal candidate for an index linked gilt ladder..........roadweary said:I’m 55. About 800k in my pension.Plan was to work full time to 60, 4 days a week for another couple of years - then take 40-50k a year tax free till state pension contributes.I don’t have any ‘tax/growth sensible’ vehicles available should I take my 200k now.I’m risk averse and about as conflicted as I could be as to whether I withdraw some or all of the 200k now.https://youtu.be/UqrO9Wi6rSY In so much as I understand from that, I like the idea and the fact that you can buy something, know the price on maturity and have a good idea of the income generated.

A whole bunch of questions, sorry.

I didn't see any explanation of tax liability. So, tax on the 6-monthly interest of a UK bond? And if the bond were bought (using their examples) at £70 but it will mature at £100, what are the tax liabilities on that?

If you pay Capital Gains on it, isn't that potentially just as expensive (or more) as leaving it in the pension and then getting charged income tax as you draw down on the funds if the tax free allowance has gone?

And the 6-monthly interest....is that shielded from tax as long as you re-invest back into the fund...or do you get charged CGT/income tax on that interest?

Then the big one is....what are the costs (apart from time) of doing this for yourself? Do you have to pay to buy / sell / report on what you've done?

Next, the time part.....is this something where I can practically say, I'm going to invest 50k on bond A that matures in 7 years' time, 50k in bond B that matures in 8 years' time, 50k for Bond C - 9 years, 50k bond D 10 years? That's probably manageable. It seems like it might not grow as much as the pension fund....but then it seems guaranteed that it can't lose - or am I missing something there?

And is this all self-done, or can you pay just small fees for a trusted party to do this for you? But what is small and who do you trust

Sorry for all the questions, but this sounds very interesting....and if I did decide to do it, I'd be investing 200k before the budget, so I need to get pretty savvy pretty quickly!

Assuming you held these in a general investment account, you may need to pay income tax on the coupons, unless you have spare personal allowance or personal savings allowance to offset against.......lategenexr's gilt ladder tool will show you an estimate of the likely max amount you might have to pay.

As to getting them, all you need do is open a GIA at your platform of choice and then call them to place your orders (IL gilts can't usually be dealt online, but most platforms will, AFAIK, charge you the online dealing fee, rather than the telephone dealing fee (but make sure beforehand)). Obviously the costs will vary depending on the ladder you want to build, but a 12 year ladder bought today, paying out for the final 4 years of it's life, might cost less than £50 to set up. Again, play around with lategenexr's gilt ladder tool.....it's fairly straightforward......you just need to tell it how long the ladder will last, how much you want it to payout (in today's money), when you want the payments to start, your marginal tax rate and the likely interest on cash deposits in the account (this is an unknown really, so I use 2%)......oh, and don't forget to click on "index linked". The tool will also show you the cash flow model of the ladder. Finally, while the tool is very handy, you don't have to follow it exactly......you can create your own after you see how it's done....though obviously that's more work for you (being handy with a spreadsheet is probably a prerequisite though)

A note on that [excellent] tool. Note that the gilts selected in the table on the right change depending if you are going to pay tax on them with the tax slider on the left. If the gilts are in a SIPP/ISA (so set the tax slider to 0%) then you want higher coupon gilts because they will be tax free held in the SIPP/ISA. However, if the gilts are going to be held in a GIA - where coupons will be taxed - then you want low coupon gilts which will trade for less than the £100 price and you make your return on the Capital Gain - which is CGT free on gilts. It's really important to get your head around this if you are interested in investing in gilts.1 -

I do not see how this is easy or can be implemented in an equitable manner for SIPP / DC pensions plus DB pensions.marathonic said:Ireland had a pension levy from 2011 to 2015. It was an annual charge on the total value of assets within the pension and was charged at:0.6% for 2011-20130.75% for 20140.15% for 2015.It was discontinued for 2016 onwards. Hopefully they don't go this route as it would be a significant cost for many. It would face a lot more backlash than some of the other options being considered.

In the case of the SIPP / DC pensions there is a pot with a value and the calculation of a percentage of that value to be passed across as tax is straightforward. It results in the individuals affected either needing to increase their contributions as a percentage of salary or receiving less income in retirement. Will those already in

However, in the case of DB pensions, there is not always pot with a value to provide the starting base for the calculation of the resulting tax liability. There are conversions that can be used for some purposes, not all of those conversions are necessarily reliable. I am certain there would be far more scrutiny of those conversions if they directly gave rise to a tax liability for someone to pay.

And who will pay that tax in the case of the DB pension - just current employees still accruing benefit, or current employees plus current retirees, or the employer?

If the employer has to meet the assessed tax cost but the scheme rules still need to be honoured, does this mean that actuaries will review the pension scheme, identify a black hole and report that as a liability which affects the balance sheet and, hence, finance for the ongoing business?

Will such a change force some companies to the wall?0 -

People who are hard working and well paid, can get a large DC pension pot that they have only contributed about only 50 or 60% to themselves , due to 40% tax relief and good employer contributions ( most well paid jobs also have more generous employers in this respect). Plus all investment growth is tax free.RogerPensionGuy said:

I fully fully agree, my view in this zone is the people who work hard, long hours, go without and plan inside the rules only to have the goalposts moved and totally upsets all their hard work and planning etc etc.Cobbler_tone said:Always find it interesting when people make the connection of 'hard working' and being affluent. My lived experience tells me that the two are not mutually exclusive. Especially in terms of having to work hard to become wealthy. Maybe 'worked smarter' is a better term. Whilst I know some very hard workers who just make ends meet.

As for just wealthy people by chance or luck, they can often augment stuff to still achieve nice outcomes.

With so much media talk about "working people" it's just talk.

An overriding view I hold reference pensions is, they should be kept simple and not tinkered with all the time, if negative changes are made these changes should be way way down the road, maybe 30 years or more, this would allow people to focus and plan.

So although later changes to limits and taxes can be annoying, it is still a very good way to save for retirement, especially for well paid employees.

Better to have a pension pot of a Million and worry about LSA changes etc , than have a much smaller fund elsewhere where you did not get any tax relief or employer contributions.0 -

I'm still trying to get my head around the whole thing. I created a csv suggesting I wanted to achieve 40k a year 2032-2036 inclusive.....set the tax slider to 40% and guessed at 2% on the cash interest rate and got the following.MetaPhysical said:

Good advice.MK62 said:

There is no CGT on gilts........the coupons are subject to income tax as interest unless held in a tax exempt account such as an ISA. The coupons on IL gilts are typically quite low though (eg 0.125%), though there are a few higher coupon examples.roadweary said:

Hi, thank you so much for the suggestion. I searched and found this on the forum.MK62 said:

You would seem to be an ideal candidate for an index linked gilt ladder..........roadweary said:I’m 55. About 800k in my pension.Plan was to work full time to 60, 4 days a week for another couple of years - then take 40-50k a year tax free till state pension contributes.I don’t have any ‘tax/growth sensible’ vehicles available should I take my 200k now.I’m risk averse and about as conflicted as I could be as to whether I withdraw some or all of the 200k now.https://youtu.be/UqrO9Wi6rSY In so much as I understand from that, I like the idea and the fact that you can buy something, know the price on maturity and have a good idea of the income generated.

A whole bunch of questions, sorry.

I didn't see any explanation of tax liability. So, tax on the 6-monthly interest of a UK bond? And if the bond were bought (using their examples) at £70 but it will mature at £100, what are the tax liabilities on that?

If you pay Capital Gains on it, isn't that potentially just as expensive (or more) as leaving it in the pension and then getting charged income tax as you draw down on the funds if the tax free allowance has gone?

And the 6-monthly interest....is that shielded from tax as long as you re-invest back into the fund...or do you get charged CGT/income tax on that interest?

Then the big one is....what are the costs (apart from time) of doing this for yourself? Do you have to pay to buy / sell / report on what you've done?

Next, the time part.....is this something where I can practically say, I'm going to invest 50k on bond A that matures in 7 years' time, 50k in bond B that matures in 8 years' time, 50k for Bond C - 9 years, 50k bond D 10 years? That's probably manageable. It seems like it might not grow as much as the pension fund....but then it seems guaranteed that it can't lose - or am I missing something there?

And is this all self-done, or can you pay just small fees for a trusted party to do this for you? But what is small and who do you trust

Sorry for all the questions, but this sounds very interesting....and if I did decide to do it, I'd be investing 200k before the budget, so I need to get pretty savvy pretty quickly!

Assuming you held these in a general investment account, you may need to pay income tax on the coupons, unless you have spare personal allowance or personal savings allowance to offset against.......lategenexr's gilt ladder tool will show you an estimate of the likely max amount you might have to pay.

As to getting them, all you need do is open a GIA at your platform of choice and then call them to place your orders (IL gilts can't usually be dealt online, but most platforms will, AFAIK, charge you the online dealing fee, rather than the telephone dealing fee (but make sure beforehand)). Obviously the costs will vary depending on the ladder you want to build, but a 12 year ladder bought today, paying out for the final 4 years of it's life, might cost less than £50 to set up. Again, play around with lategenexr's gilt ladder tool.....it's fairly straightforward......you just need to tell it how long the ladder will last, how much you want it to payout (in today's money), when you want the payments to start, your marginal tax rate and the likely interest on cash deposits in the account (this is an unknown really, so I use 2%)......oh, and don't forget to click on "index linked". The tool will also show you the cash flow model of the ladder. Finally, while the tool is very handy, you don't have to follow it exactly......you can create your own after you see how it's done....though obviously that's more work for you (being handy with a spreadsheet is probably a prerequisite though)

A note on that [excellent] tool. Note that the gilts selected in the table on the right change depending if you are going to pay tax on them with the tax slider on the left. If the gilts are in a SIPP/ISA (so set the tax slider to 0%) then you want higher coupon gilts because they will be tax free held in the SIPP/ISA. However, if the gilts are going to be held in a GIA - where coupons will be taxed - then you want low coupon gilts which will trade for less than the £100 price and you make your return on the Capital Gain - which is CGT free on gilts. It's really important to get your head around this if you are interested in investing in gilts.

Is the result below saying that I would invest 187.5k today to achieve 200k as drawn out annually in the five years beginning 2032? And that's 200k in today's money or what 200k is estimated to be worth at the point of withdrawal? 2

2 -

Think that is showing you the 'buy' cost, you need to click on the 'cash flow' table to see the dividends and redemption payments :

Is the result below saying that I would invest 187.5k today to achieve 200k as drawn out annually in the five years beginning 2032? And that's 200k in today's money or what 200k is estimated to be worth at the point of withdrawal?

0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards