We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

We're aware that some users are currently experiencing errors on the Forum. Our tech team is working to resolve the issue. Thanks for your patience.

DMP: 2 x CCA requests? Credit Agreement and Affordability - Is it worthwhile?

Ktaylor86

Posts: 57 Forumite

Dear All,

I am now 2+ years into a DMP with Stepchange, paid off over £10K with £25K to go. Debt free date is currently June 2030.

I have a total of 10 creditors of varying amounts.

In regards to some of my creditors I am wondering if it is worth doing a CCA letter for two different things but would be helpful (these are also the highest value ones):

1) Request my original credit agreement:

This is for a Barclaycard I originally took out when I was 18, some 21 years ago! As it stands it has been passed to PRA group and has a balance of circa £5,300 left to pay and was defaulted in 2023.

As it is my oldest debt I wonder if it is worth asking if they can produce the original agreement? Then I wouldn't be liable (or able to be taken to court is my understanding) if they cannot produce it?

Questions: Is it worth a shot? and would I write to PRA Group rather than Barclaycard directly? If they can't produce it, its unenforceable right? So I could ask Stepchange to not pay it?

2) Put in a claim for irresponsible lending:

I took out 3 x Zopa loans in the space of about 2 years (across 2020-2022), with the reason 'debt consolidation'. All 3 now defaulted and passed to Link Financial.

The remaining balances are currently circa: £8,000, £3,700, and £3,600.

I am considering following the process to claim this was irresponsible lending?

Questions: Would I claim with Zopa? How do I go about this? I do not know the exact dates so should I get the original agreements for these first? Is this likely to have an outcome that is useful in my circumstances.

I appreciate any advice and guidance on doing this and how to go about it.

Many Thanks

I am now 2+ years into a DMP with Stepchange, paid off over £10K with £25K to go. Debt free date is currently June 2030.

I have a total of 10 creditors of varying amounts.

In regards to some of my creditors I am wondering if it is worth doing a CCA letter for two different things but would be helpful (these are also the highest value ones):

1) Request my original credit agreement:

This is for a Barclaycard I originally took out when I was 18, some 21 years ago! As it stands it has been passed to PRA group and has a balance of circa £5,300 left to pay and was defaulted in 2023.

As it is my oldest debt I wonder if it is worth asking if they can produce the original agreement? Then I wouldn't be liable (or able to be taken to court is my understanding) if they cannot produce it?

Questions: Is it worth a shot? and would I write to PRA Group rather than Barclaycard directly? If they can't produce it, its unenforceable right? So I could ask Stepchange to not pay it?

2) Put in a claim for irresponsible lending:

I took out 3 x Zopa loans in the space of about 2 years (across 2020-2022), with the reason 'debt consolidation'. All 3 now defaulted and passed to Link Financial.

The remaining balances are currently circa: £8,000, £3,700, and £3,600.

I am considering following the process to claim this was irresponsible lending?

Questions: Would I claim with Zopa? How do I go about this? I do not know the exact dates so should I get the original agreements for these first? Is this likely to have an outcome that is useful in my circumstances.

I appreciate any advice and guidance on doing this and how to go about it.

Many Thanks

0

Comments

-

Yes to all, CCA requests are a good idea for debts that old, if they cant produce a copy, or a reconstituted copy, of your credit agreement, then it becomes unenforceable until they do, however long that may be.

Get any affordability complaint sent in as soon as possible as they can take some time to be processed.

Look on the Debt Camel website for more details and a template complaint letter.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter1 -

CCA requests always go to the current owner, in your case PRA. They have to go back to who they bought it from to request the documentation, and for one that old there is a good chance they wont be able to produce it. They couldn't for mine (taken oit in 2001 as an egg card, later transferred to Barclaycard.

Affordability complaints go to whoever it was that made the decision, in your case Zopa. In my experience you are more likely to have a complaint found in your favour if they gave you multiple loans or multiple credit limit increases. You don't have anything to lose so it's worth a shot. It's pretty standard for lenders to reject complaints so escalate it to the FOS if they happens(debt camel gives details). It can be a long drawn out process, my Nationwide one took two years with them dragging their feet every step of the way but I eventually got a £16,000 interest refund. I think that was quite an exceptional case but it's not unusual for people to get some back.2 -

Yes, as above

https://debtcamel.co.uk/refunds-large-high-cost-loans/

Note that lenders will automatically reject if the loan was more than 6 years ago so get started now, even though they will probably reject the complaint anyway.

Do affordability complaints on any large loans, multiple loans, multiple credit cards from the same lender. If in doubt , try it anyway

The cca request is a formal request under s77-9 Consumer Credit Act. Again do all those now on any loan, catalogue or credit card. This is a right that the government is due to remove and replace with something much more vague.

https://nationaldebtline.org/get-information/sample-letters/information-about-your-agreement-under-consumer-credit-act/1 -

Brilliant thanks all!Will get it started asap!I assume with the CCA request for agreement you can only do these on loans and credit cards, catalogues, not overdrafts?Also I realize my Zopa loans must have been 2021 onwards (as I moved house then and was definitely after the move) so that gives a little more time if there is a 6 year limit. However I will on these this week!0

-

Hi all,

Thanks for your help and guidance.An update from me:

I sent 6x CCA requests to my creditors, thought it can’t hurt. But the one I’m most hopefully with is the 20 year old Barclaycard.The postal orders included a fee (50p) so was £9 total I then sent them all in separate envelopes as second class signed for.Additionally I emailed Zopa my affordability irresponsible lending claim for 3 loans. Taken within 18 months period.

I’ve requested all my bank statements from that time in preparation (closed account)

I’ll update this thread as things progress in case helpful to others too.3 -

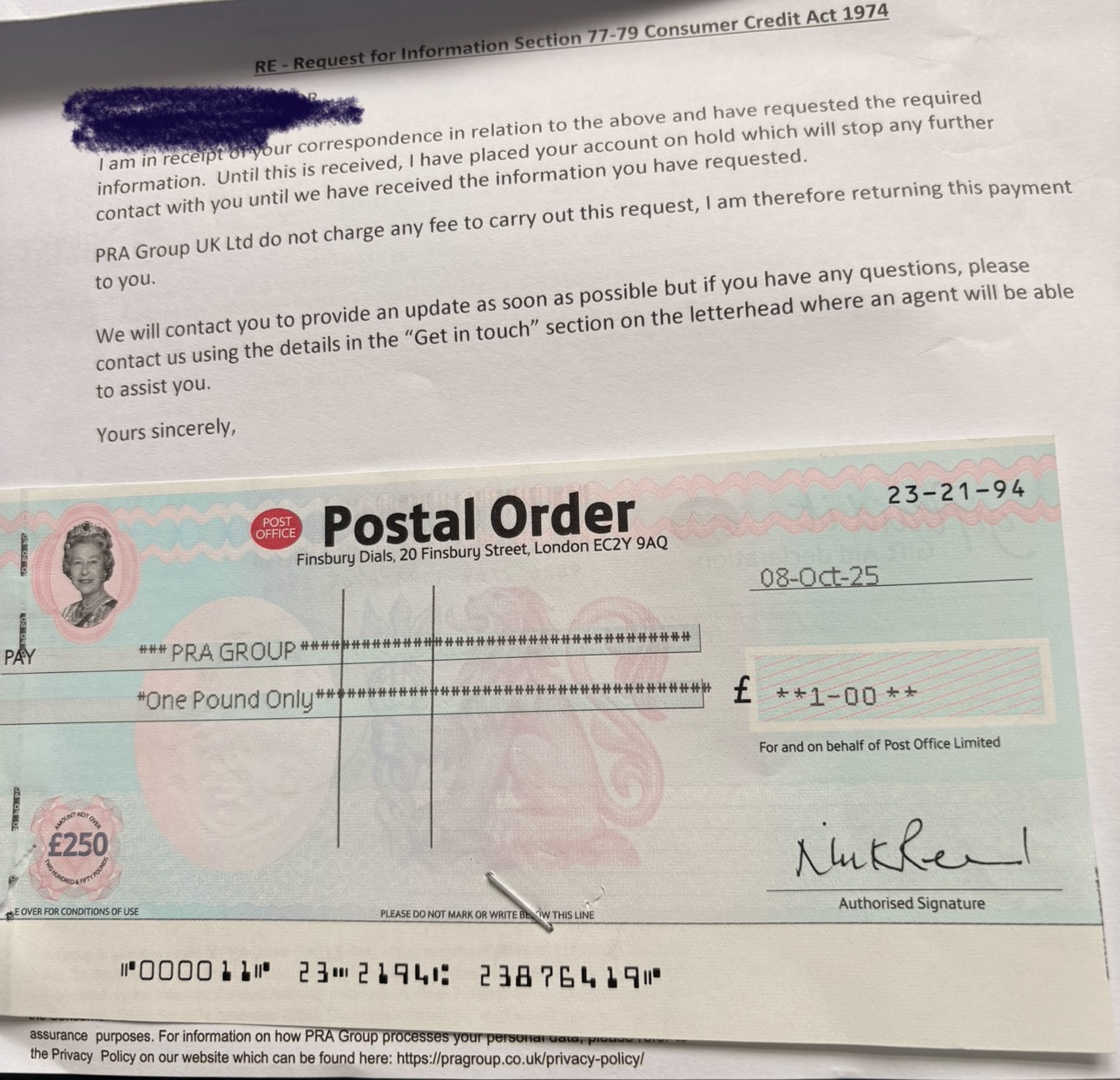

Update!I have received a letter as below from PRA - this is the one I’m most hopeful about as it has my 20 year old barclaycard and still owe £5K

The letter reads more like a general acknowledgement but the line about ‘your account is on hold and we won’t contact you’ is throwing me slightly.. does this mean they think they won’t be able to get it?Also it’s not even yet been 12 working days,

Do I take any action or keep paying as normal for now? 0

0 -

How much are you paying a month to them?

0 -

Paperwork is always retained by the original creditor, even when debts are sold, so PRA will have to go back to Barclaycard to try and obtain the information you have requested, which is why your account has been placed on hold, read nothing more into it than that.

It has absolutely nothing to do with the likelihood of Barclaycard having kept your information for 20 years, or not, its simply a statement of fact that they have asked Barclaycard to look for it, and will provide an update when they know more.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter1 -

At least PRA acknowledge that it is a formal request under CCA1974.

They don't seem to understand that it is a statutory fee. Anyway, keep the po and use it again. Ah, you made it payable to them. I never do that.

I thought the 12-day thing had gone but I notice National Debtline still quote it. Let me check.

Yep, pretty sure it's not there any more.

1 -

Thats just the standard letter they send while they are waiting for a response from whoever they bought it from. After about three months they told me that my Barclaycard debt was unenforceable but tried to downplay that with some ******** about it still being due and that they'd let me know if it became enforceable. Quite amusingly they enclosed a copy of a letter from Barclaycard to them that was marked internal only saying that due to the age of the account it wouldn't be possible to provide the CCA.

I'd stop paying now, you don't want to losr any more money than you hsve to.2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards