We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Addition of health details for Annuity triggers Underwriter referral

Comments

-

Many thanks, that’s very helpful 🙂DRS1 said:

I think once underwriting has done its thing you get an email asking you to call them. Then you tell them the sort of annuity you want (which may be two three or a dozen variations) and they go away (for half an hour - that's what it feels like anyway) and run the figures and then they tell you over the phone what those figures are and you say send me a written quote for that one or those two or however many you like the sound of). Be warned they come in the same envelope and mine didn't fit through the letterbox! That's because each quote comes with its own acceptance forms (yawn)grn99 said:One more aspect I remain unsure of, is getting the various options on the quotes such annual increment, Guarantee period, and how much of the fund to use etc. Given these were going to be done today to show the differences (we never got that far), how will that now work with Underwriting's involvement? Will they be involved for every quote or do they just give an annuity value to someone that is used during future quotes, or is it done another way?

But what you should not get is another 5 day wait between quotes (unless you are changing any of the medical details)0 -

Was doing quite well with getting annuity quotes but today SW wanted to speak to wife about her health history (my pension, but joint life annuity being quoted for)... So rather than come back with quotes as in the last few days, I'm told it's being referred to underwriting.All the providers can do manual underwriting for quotes. It typically occurs on more complicated health cases or where the health form hasn't been completed very well and is giving inconsistent information. Usually, the IFA or annuity broker would pick that up during the data collection stage, and that issue would be avoided, but if you are bypassing them, the provider will often step in to cover their own backsides.Apparently they email back eventually, but in the meantime the rates offered can alter and cannot be locked in as it is being referred.The quotes system for providers would lock in the minimum rate based on the data entered unless the medical info was so confusing that the quote system would show the annuity rate offered as "not guaranteed".They wont decline. Worst case scenario is clean health rates.

I know I cannot change their decision, but is there a chance they will either decline the risk or give a rate that is unattractive?

SW don't often come out on top (you usually have to hit a sweet spot for them to come out well). Not once have they been top in recent quotes for me. Last time was around May. So, how does the SW quote you have so far compare to the others?

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

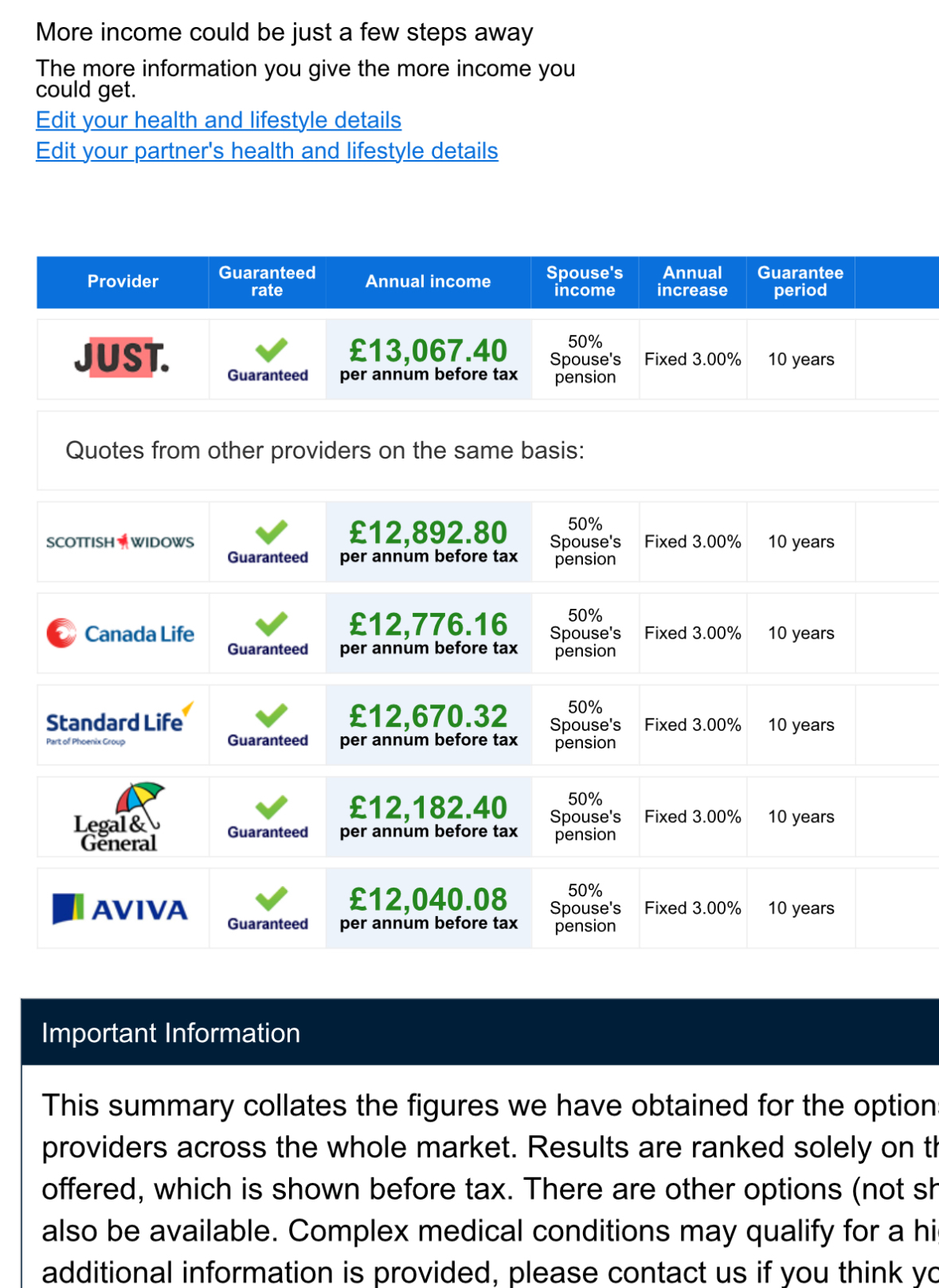

This is just one quote via HL for 279K

This is just one quote via HL for 279K

interestingly when those same criteria were put to SW direct they quoted circa 14,716.Today SW were going to obtain whole of mkt quotes as well as theirs, but we never got that far.If there’s a clear winner above SW, I’d need to start over with a new IFA. What would be a reasonable fee for doing an annuity with a.n.other provider and will the new IFA need to fact find our background finances etc to get to that point?0 -

A couple of thoughts

There are some threads on here about fixed increases (5%) vs RPI. I think most would opt for RPI. Personally 3% would be too low for me. But you may have other inflation linked income streams and want this one to start high.

You do hear stories of IFAs wanting to do a full work up on your finances. You should be able to find someone who doesn't want to do that but it can be tricky finding such a person. Others on here have instead used HL or Retirement Line for simplicity because neither of them will want to do that work up (but they are brokers not IFAs)1 -

Good thoughts. Yes other income will be index linked so was a bit of a hybrid, but I agree about 5 v RPI having seen the calculations.DRS1 said:A couple of thoughts

There are some threads on here about fixed increases (5%) vs RPI. I think most would opt for RPI. Personally 3% would be too low for me. But you may have other inflation linked income streams and want this one to start high.

You do hear stories of IFAs wanting to do a full work up on your finances. You should be able to find someone who doesn't want to do that but it can be tricky finding such a person. Others on here have instead used HL or Retirement Line for simplicity because neither of them will want to do that work up (but they are brokers not IFAs)

praying SW is a good rate as trawling IFAs again after 7 months is just more hassle 😂

are broker prices more or less competitive than IFA ?

0 -

I'm just glad I used Retirement Line after getting an IFA online quote, Moneyhelper and HL. No local IFA was interested.Same tax free lump sum and same pot to fund the annuity with all the quotes, wasn't bothered who paid the commission. The one that provided the most a year was the one I went for, thats the only figure that matters isn't it?2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards