We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Understanding how the Pension Protection Fund would consider a previous lump sum payment

Wobble101

Posts: 89 Forumite

I will start drawing from a deferred DB scheme next year and have been wondering what would happen should the scheme end up in the PPF.

In terms of likelihood, I’m confident this isn’t imminent or inevitable but the organisation is in a troubled sector.

My question is about lump sum payments and how/whether the PPF takes these into account.

My understanding is that, pre-scheme retirement age, payments would be reduced to 90%. But if these payments had been accompanied by a lump sum payment (and so reduced accordingly) would this make any difference. If it doesn’t make a difference then taking an advance lump sum does seem advantageous in my situation.

I’ve had a look online but am struggling to find anything about this particular scenario.

Many thanks.

0

Comments

-

The PPF would pay according to the rules on a pension in payment, either 100% or 90% depending on the particular circumstances. The commencement lump sum does not come into the equation.0

-

Why do you think it would be treated differently ? The PPF looks at your entitlement at the point of them taking over responsibility for payments. If you have taken a lump sum you would be receiving a lower pension, no lump sum then a higher pension. That means the lump sum has already been taken into account.0

-

Given the vagaries and complexities of just about anything in the arcane world of pensions, it was pretty sensible of OP to even think of asking the question in the first place!molerat said:Why do you think it would be treated differently ? The PPF looks at your entitlement at the point of them taking over responsibility for payments. If you have taken a lump sum you would be receiving a lower pension, no lump sum then a higher pension. That means the lump sum has already been taken into account.

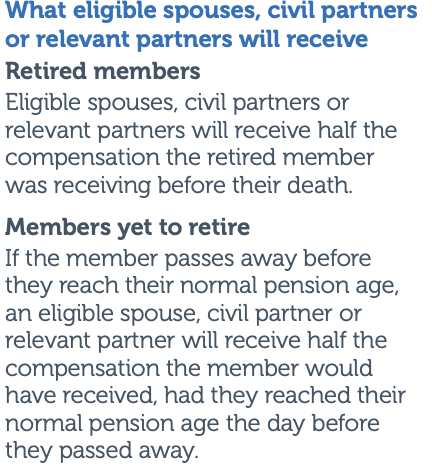

There is a further important consideration, especially if OP has a spouse/partner. Normally when a member chooses to 'commute' (give up some of their pension for an immediate tax free cash lump sum), any benefits for their spouse/partner/eligible children are calculated as if the member had not commuted any of their pension.

That's not how the PPF works - and payments are based on 50% of the member's pension, even if the original scheme offered a higher %:

https://www.ppfmembers.org.uk/-/media/Files/Booklets/COMPWeb_0315.ashxGoogling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0 -

As beneficiaries have been brought up, I thought I would post a link to my post about PPF beneficiary nominations. As nobody responded I took it nobody else was affected but I will add here just for info.

https://forums.moneysavingexpert.com/discussion/6603927/fas-ppf-beneficiary-nomination#latest0 -

Aren't there some other issues for the OP to think about with the PPF - eg pension increases? If he starts taking the pension he will presumably get scheme increases but if the scheme goes into the PPF aren't the increases restricted to benefits built up after 6 April 1997? Maybe all his service is post 97?

I am wondering if the OP thinks there will be any clawback of benefits already paid to him if he is taking benefits before NPA and so falls in the 90% camp? I don't think that can happen. But can the scheme (if it thinks PPF is imminent) refuse to pay benefits early (eg because it would mean giving someone 100% when they would otherwise only get 90%)?0 -

I suspect that was exactly what OP had in mind when they asked the question.DRS1 said:Aren't there some other issues for the OP to think about with the PPF - eg pension increases? If he starts taking the pension he will presumably get scheme increases but if the scheme goes into the PPF aren't the increases restricted to benefits built up after 6 April 1997? Maybe all his service is post 97?

I am wondering if the OP thinks there will be any clawback of benefits already paid to him if he is taking benefits before NPA and so falls in the 90% camp?

Trustee and/or employer consent is usually needed to take a pension before the scheme's Normal Retirement Date. If there are concerns about the funding position of the scheme/the employer covenant (the employer's ability to make ongoing contributions to ensure the scheme can meet its obligations), then allowing some members to retire early - especially if they take maximum tax free cash - may not be fair to other members.DRS1 said:But can the scheme (if it thinks PPF is imminent) refuse to pay benefits early (eg because it would mean giving someone 100% when they would otherwise only get 90%)?

If someone retires before the scheme's NRD and the scheme goes into the PPF, then:

https://www.ppfmembers.org.uk/-/media/Files/Booklets/COMPWeb_0315.ashx

Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0 -

Thanks everyone, and sorry for vanishing after all these helpful replies.

Why am I worrying about this at all? As @Marcon says, its for exactly the reasons that @DRS1 suggests. If previous lump sum payments are taken into account in the reduction factor applied to my pension were the scheme to enter into the PPF then taking a lump sum isn't worth it (ie there is an additional reduction on top of the 90% payment). But if they are not taken into account then it is worth considering.

@DRS1 asked about the scheme not paying out if there is likelihood of it entering the PPF. As mentioned in my original post this isn't something I'm worried about in the short term. But thank you for flagging the point about scheme increases and the PPF - my time in that pension began a few years before 1997 so that is something that would affect me.

With regard to @Marcon's other point (about spouse benefits), the scheme I'm in offers the same as the PPS - ie once you are retired the spouse would be entitled to 50% of the benefits.

All of this has strengthened my view that I should take some kind of lump sum out (not the maximum however).0 -

Beware - as I've said above, the calculation won't start from the same level.Wobble101 said:

With regard to @Marcon's other point (about spouse benefits), the scheme I'm in offers the same as the PPS - ie once you are retired the spouse would be entitled to 50% of the benefits.

All of this has strengthened my view that I should take some kind of lump sum out (not the maximum however).- Your scheme will pay a spouse's pension based on the amount a pensioner would have been receiving when they died had they taken no tax free cash (regardless of whether they actually took any - it's only their own pension they 'commute').

- The PPF bases any spousal pension on the actual amount a pensioner is receiving at the time they die.

Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0 -

Ah ok, thanks @Marcon.It’s hard juggling the unknowns - in this instance, who dies first and will the scheme enter the PPF. My husband has a long term illness that makes it more likely I’ll survive him (and means we are keen to enjoy the healthy years we have together) - these are factors in our thinking. But it is all of course unknown so we are just trying to make educated decisions.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards