We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

"Cashing in" a defined benefit pension

Comments

-

Yes, of course. Sorry Marcon. I missed that.QrizB said:

I think Marcon is suggesting that it would come from the employer.bjorn_toby_wilde said:Where else does the extra money come from for the active members?!

In the case of my old employer I doubt it. They weren’t known for their generosity, especially if, as Marcon suggests, most employees would miss the distinction.0 -

Ultimately it is the employer on the hook for whatever cash is needed to pay the promised benefits to which member are entitled under the scheme.bjorn_toby_wilde said:

Yes, of course. Sorry Marcon. I missed that.QrizB said:

I think Marcon is suggesting that it would come from the employer.bjorn_toby_wilde said:Where else does the extra money come from for the active members?!

In the case of my old employer I doubt it. They weren’t known for their generosity, especially if, as Marcon suggests, most employees would miss the distinction.

Early retirement is rarely an entitlement. ER from active membership often needs employer (and usually trustee) consent if the terms are better than 'cost neutral', because there's a cost. However, the way the scheme actuary calculates the ongoing contribution rate means that there's a bit of 'extra' cash in the scheme at the point where a member leaves early. This reduces the 'strain' on the fund and could mean the employer doesn't actually need to chip in extra cash at that point - so there's a better chance of consent being forthcoming.

If the scheme is in deficit, then it's likely the employer would have to pay in some extra cash to meet an ER request from an active member if the ER factors are better than cost neutral - so a bit of generosity would be needed unless the employer is keen to use ER as a method of getting shot of unwanted staff.Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0 -

bjorn_toby_wilde said:

So the actuaries assume future salary growth is lower than revaluation?Marcon said:

You'd expect the late retirement factors to be the same - there is no longer any need for the actuary to take into account future salary growth v future revaluation in deferment (see my previous post). Everyone is at the 'same point'.MeteredOut said:bjorn_toby_wilde said:

Not necessarily so, although it’s often quoted on here.Cobbler_tone said:Early reduction factors are not designed to be punitive.

One of my pensions has two sets of ERFs; one generous version for those retiring from active service and a far less generous version for those who had left the company or (as in my case) been made redundant.

3.5% reduction per year for active service and 5% per year for deferred.

Presumably the intent was to encourage people to stay.

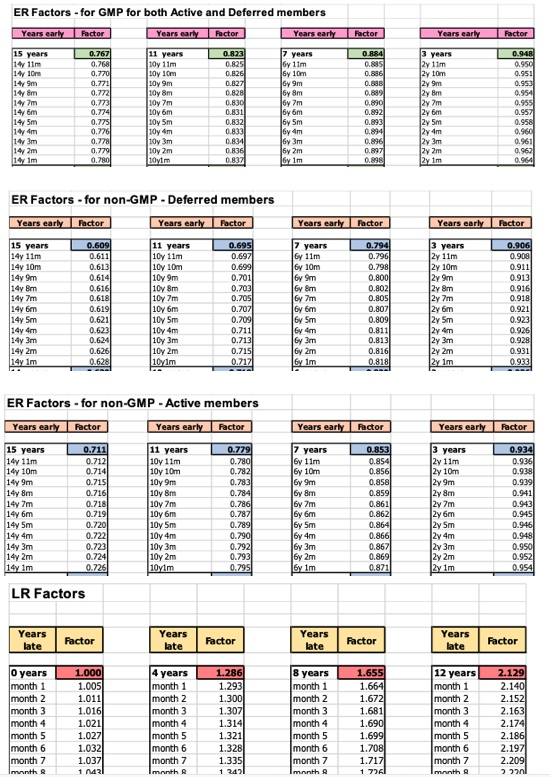

As an example of this, here's excerpts from the scheme I was in for a short period of time in the early part of my career. Same ERF for GMP, but different for active/deferred fpr GMP components. But the same late retirement factors for everything/everyone.

If you stay in active membership beyond a scheme's NRA, you get the benefit of further accrual and possibly salary increases, assuming the scheme allows this.

Late retirement factors are applied where members have ceased to build up benefits but don't draw their pension at the scheme's NRA.

Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!1 -

My take on the “punitive” element comes from my previous pension scheme.

Cost neutral ERFs were 4% per year, whether deferred or active. My feeling, and I can’t evidence it, is that this is about industry average.

The company was then bought out by a US multinational and the ERFs became 3.5% from active service and 5% for deferred.

Thankfully I didn’t transfer my benefits from the first scheme into the second.

0 -

It isn't just finger in the wind stuff, nor are all schemes created equal, so 'industry average' doesn't really come into it, although I can understand why you think it would.bjorn_toby_wilde said:My take on the “punitive” element comes from my previous pension scheme.

Cost neutral ERFs were 4% per year, whether deferred or active. My feeling, and I can’t evidence it, is that this is about industry average.

The company was then bought out by a US multinational and the ERFs became 3.5% from active service and 5% for deferred.

Thankfully I didn’t transfer my benefits from the first scheme into the second.

When carrying out a valuation, actuaries use mortality tables and make assumptions, which are discussed/agreed with the trustee and employer. Look at any triennial valuation report and it will spell out what these are, and which tables have been used - riveting reading, ideal for insomniacs looking for an alternative to sleeping tablets.

ERFs, like other scheme factors, are subject to regular review and take into account both general economic conditions and (importantly) scheme-specific experience - which is where the assumptions come into their own. Where members work in, say, a heavy industry in a part of the country with below average life expectancy those assumptions will be very different from a scheme where members work in cosy offices in an area where life expectancy is above average. The scheme actuary's recommendations will reflect that - which is why you can't just compare one scheme to another and draw valid conclusions from doing so.

Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0 -

Mmmmm. I’m sure you’re right as you work

or have worked in pensions…..but…..I had no change of job or industry. Just a 20% difference in ERF because of a takeover.

I didn’t move from a desk job to heavy industry.

You’re portraying a degree of review, accountability and standardisation which should surely result in very little difference between the two schemes but in fact there’s a huge gulf. That’s surely a result of differences in policy not practice?

0 -

Hi, I have just been through the exact same loop and my lovely new IFA stated NEVER cash in or transfer a DB pot. He said the same thing as many here; the DC managers wont do it without a full analysis and the analysis always says ‘ don’t move it!’Take the 25% if possible. The only thing hard to bear with me is paying 40% tax on the DB income, as I’m still working ( plus having to pay an accountant to do SA. )"Is it that the future is so uncertain, the present so traumatic that we find the past so secure? " Spike Milligan1

-

You could pay an equivalent amount back into your DC pension (subject to having enough annual allowance to spare), and claim the tax relief.Datchet said:The only thing hard to bear with me is paying 40% tax on the DB income, as I’m still working ( plus having to pay an accountant to do SA. )N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

2.72kWp PV facing SSW installed Jan 2012. 11 x 247w panels, 3.6kw inverter. 35 MWh generated, long-term average 2.6 Os.2 -

Generalisation alert - that assessment may have been appropriate for you, and chances are it'll fit most people, but it certainly doesn't apply to all people....Datchet said:Hi, I have just been through the exact same loop and my lovely new IFA stated NEVER cash in or transfer a DB pot. He said the same thing as many here; the DC managers wont do it without a full analysis and the analysis always says ‘ don’t move it!’5 -

My sentiments entirely. Any adviser who works on the basis that a particular course of action is right (or wrong) for everyone, regardless of their circumstances, is to be avoided. This adviser sounds pretty hopeless - the analysis does not 'always say don't move it'. If it's in the member's interests to transfer, that's what the answer will be.eskbanker said:

Generalisation alert - that assessment may have been appropriate for you, and chances are it'll fit most people, but it certainly doesn't apply to all people....Datchet said:Hi, I have just been through the exact same loop and my lovely new IFA stated NEVER cash in or transfer a DB pot. He said the same thing as many here; the DC managers wont do it without a full analysis and the analysis always says ‘ don’t move it!’

Wonder if this adviser actually hold permissions from the FCA to advise on such transfers? One can only hope not.Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!4

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.9K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.4K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards