We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Use LISA to pay of debt?

Lmm08

Posts: 26 Forumite

Hi everyone, I’d really appreciate some advice/opinions.

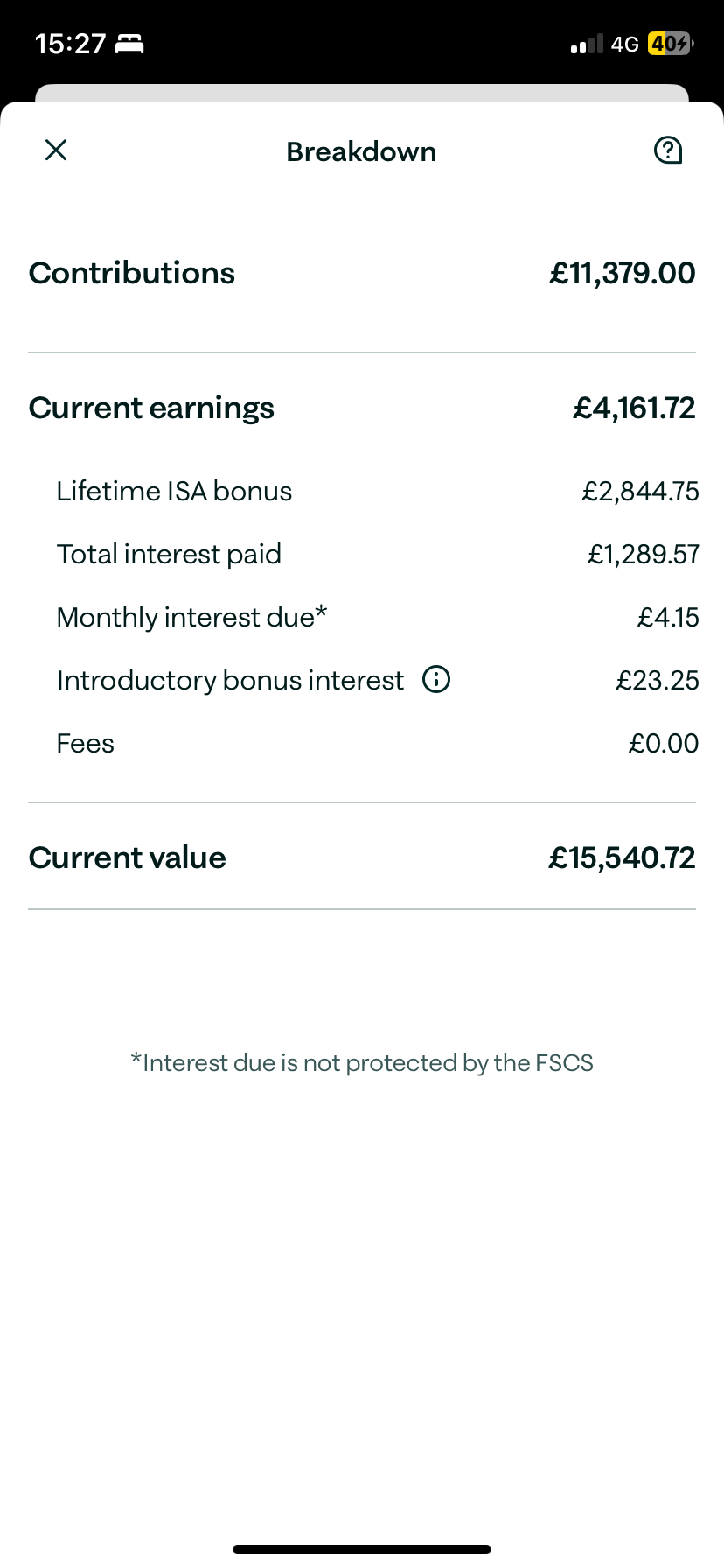

I have nearly £15,500 saved in my LISA account towards a deposit. My problem is, I also have £7000 worth of credit card debt which I just can’t seem to shift. Because I have them means I’m so frivolous and just use it. I really want to just get rid of both of them to stop me spending.

My question is, should I use the money from my LISA account to pay off both cards and then just cancel them? I understand that there will be penalties and lose my government bonus. I am currently living with my parents without any rent to pay so I am in a good position. When i’m sensible, I can put away £1000 per month.

I have nearly £15,500 saved in my LISA account towards a deposit. My problem is, I also have £7000 worth of credit card debt which I just can’t seem to shift. Because I have them means I’m so frivolous and just use it. I really want to just get rid of both of them to stop me spending.

My question is, should I use the money from my LISA account to pay off both cards and then just cancel them? I understand that there will be penalties and lose my government bonus. I am currently living with my parents without any rent to pay so I am in a good position. When i’m sensible, I can put away £1000 per month.

Perhaps I could just clear the debt and then my focus would be putting the money back into my LISA. Is this really silly… I just want to debt gone. I know I’ve been just so silly and immature, and I want to beat this.

I’ll include a screen shot breaking down my savings.

Thank you

0

Comments

-

how much are you adding to the LISA a month? Is interest being charged on the cards and have you looked for 0% balance transfers?0

-

I’ve not put anything into my LISA for months… one of my cards (has £4000) was a balance transfer and still 0% interest until next year. The other has £3000 and I get charged around £40 a month interest.ManyWays said:how much are you adding to the LISA a month? Is interest being charged on the cards and have you looked for 0% balance transfers?0 -

I wouldn't touch the LISAs as there will be cheaper ways of repaying your debt.

First you might want to reduce the cost of your debt. This could mean getting a balance transfer credit card or taking out a personal loan.

Next, you can lock the credit cards away, be extra frugal and put as much money as you can in to repaying the debts. Make repayments towards the debt whenever your receive money (salary, bonus, tips etc.).0 -

The priority is really figuring out what you're spending on and changing the habits. When is the last time you spent on a credit card and why?Lmm08 said:Hi everyone, I’d really appreciate some advice/opinions.

I have nearly £15,500 saved in my LISA account towards a deposit. My problem is, I also have £7000 worth of credit card debt which I just can’t seem to shift. Because I have them means I’m so frivolous and just use it. I really want to just get rid of both of them to stop me spending.

New habits could look like cutting up the cards and putting a strict budget to cover your essentials, credit card repayments and an allowance for 'wants' each month without needing to put more on debt.

If you don't and just pay off the cards in a lump sum, you'll have more credit line which you could end up just running up again, plus no savings.

Only then can we look at the balances and what to pay off:

Okay so 0% is good, and the £40 on £3000 is ~16% interest which is high but not as much as the LISA 25% penalty, and it would be a shame to give that up.Lmm08 said:

I’ve not put anything into my LISA for months… one of my cards (has £4000) was a balance transfer and still 0% interest until next year. The other has £3000 and I get charged around £40 a month interest.ManyWays said:how much are you adding to the LISA a month? Is interest being charged on the cards and have you looked for 0% balance transfers?

If you really can put away £1000 a month, that's 3 months and ~£80 in interest to pay off the 2nd card (as the balance goes down, so does the interest). The alternative is cashing in £4000 of your LISA to pay the 25% penalty and clear the £3000 balance, effectively costing you £1000!

Then even with a break over the holidays, another 4 months of pay offs next year and you could be done with all debt by April! For that sort of timeframe, you may not even want to bother with another transfer.0 -

Pay the minimum on the 0% card and as much as you can off the other card. Aim to clear that before the 0% ends and if necessary try and get an 0% with the aim to pay off the whole lot.

Meantime reduce the limits on your cards.If you've have not made a mistake, you've made nothing0 -

Another one to urge you to keep your LISA.

Excellent advice from posters already.@saajan_12 said, if you are able to put away £1,000 per month, then you can clear your interest bearing card in 3 months. Then focus on the other one.

Spend some time reviewing your last few months bank statements and understand where you being ‘frivolous’. Is it impulse purchases, coffee shop trips or work lunches? Are these habits you can change?Reduce credit limits, remove cards from apps or self impose an overnight hold on online baskets to take the impulsivity out of these decisions.Could you set yourself savings targets? You said you are currently living with parents and not paying rent, would you like to buy your own place in the future? You are in such a great place to save for your future. Would it help if your parents took rent from you and saved it on your behalf?I’m a Forum Ambassador and I support the Forum Team on the Pension, Debt Free Wanabee, and Over 50 Money Saving boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the Report button, or by e-mailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.0 -

I would get any 0% you can AND CLOSE CLEARED CARDS. Also set up a standing order that will clear the first 0% to end card, and ones that are more than the minumum to the other 0% cards.

Do not save any more money into the LIS, use it all to clear these cards.

Freeze the cards if you can in the app. Leave them all at home, not on your mobile, remove from digital wallets and the retailers you often shop at.

Reduce your credit limit as you clear them, remembering that at the end of this you ideally want one card, preferably with a low interest rate when the 0% ends, and a limit of about £1000.0 -

I think you really need to start budgeting to clear this debt down. Take the cards out of your purse and off your phone.

My concern is if you are living at home, not paying rent but are saving for a deposit. Once you get your own place, without a locked in budget you could end up in a far worse place down the line.

You're in the right place for excellent help and it's good you've recognised it now before it gets worse.0 -

Unless you are planning to spend your entire life unable to afford anything that costs more then what's left of your wages that month, then you need to learn to be able to have money and not spend it.

So, keep your LISA (but consider it untouchable until you buy a house) and make a plan for paying off your debt - highest interest first. (And think about adding to your LISA if the numbers make sense.)Statement of Affairs (SOA) link: https://www.lemonfool.co.uk/financecalculators/soa.phpFor free, non-judgemental debt advice, try: Stepchange or National Debtline. Beware fee charging companies with similar names.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards