We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Couple of State Pension queries.

Comments

-

Exactly. My OH retired recently at 60 with almost 45 years continuous employment and he was still a year short. He paid £907.40 to top up that final year, your friend may have the same option. The payback time is pretty good - though occasionally someone might only gain pence rather than pounds per week for their final year’s contribution, and decide that one’s not worth buyingminimalising said:Hi, all. Thanks for the replies.

I'm 50. I do have a gov.uk account.

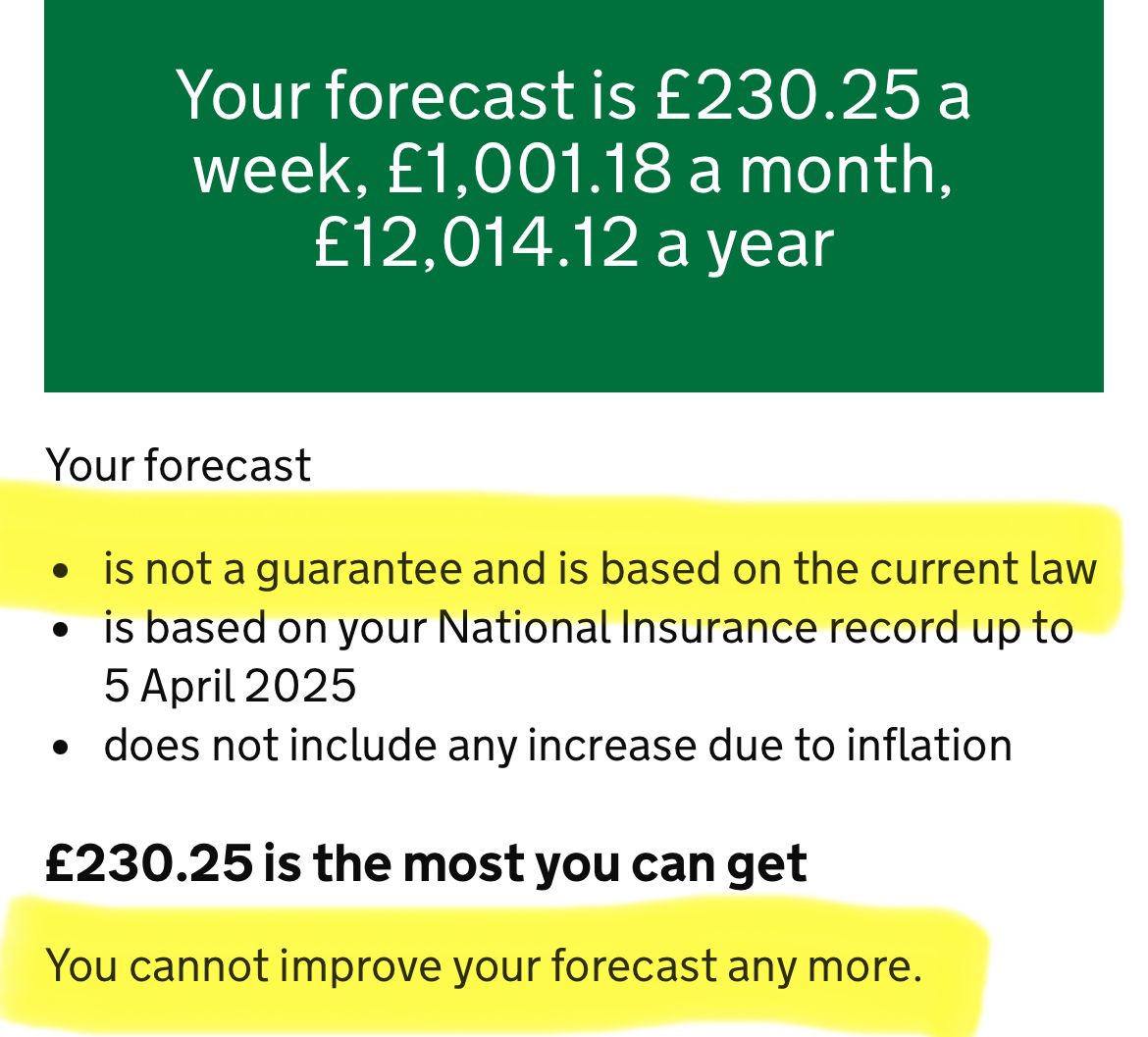

It currently says my forecast is £12,014.12 a year.

The reason for this thread is that a retired guy I know (went at 59 is now 62) said that his State Pension forecast has been reducing and he thinks it's because he's no longer paying in. He has over 35 years paid in, no gaps.

Fashion on the Ration

2024 - 43/66 coupons used, carry forward 23

2025 - 62/890 -

He's under transitional arrangements so as already repeatedly pointed out above, 35 years isn't the magic number (whatever endless posts on social media, press reports etc might say!).minimalising said:Hi, all. Thanks for the replies.

I'm 50. I do have a gov.uk account.

It currently says my forecast is £12,014.12 a year (SP at 2041). Currently £220.29 a week and will got up to £230.25 a week after I contribute two more years. It notes I was contracted out.

The reason for this thread is that a retired guy I know (went at 59 is now 62) said that his State Pension forecast has been reducing and he thinks it's because he's no longer paying in. He has over 35 years paid in, no gaps.Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!2 -

minimalising said:The reason for this thread is that a retired guy I know (went at 59 is now 62) said that his State Pension forecast has been reducing and he thinks it's because he's no longer paying in. He has over 35 years paid in, no gaps.At a risk of overlabouring the point, that guy will have a state pension forecast that says what pension he'll get if he pays for however many more years before he's 67.Your forecast says you need another two years. Once you've paid those two years, the forecast won't ask for any more.The 62-yo guy really needs to get a move on and buy his missing years, unless he wants to retire with a smaller pension.N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

2.72kWp PV facing SSW installed Jan 2012. 11 x 247w panels, 3.6kw inverter. 35 MWh generated, long-term average 2.6 Os.0 -

As you have noticed your state pension forecast includes two numbers.minimalising said:Hi, all. Thanks for the replies.

I'm 50. I do have a gov.uk account.

It currently says my forecast is £12,014.12 a year (SP at 2041). Currently £220.29 a week and will got up to £230.25 a week after I contribute two more years. It notes I was contracted out.

The reason for this thread is that a retired guy I know (went at 59 is now 62) said that his State Pension forecast has been reducing and he thinks it's because he's no longer paying in. He has over 35 years paid in, no gaps.

The first number is the amount you would get if you stopped working tomorrow and never paid another penny of National Insurance. It cannot decrease unless the government makes wholesale changes to the law around how state pensions are calculated, which is very unlikely in the short term.

(And it's even more unlikely that they would reduce already earned entitlements. When the new state pension was introduced in 2016 nobody had their already earned entitlements protected, which is part of the reason why everyone who started working before 2016 is under transitional arrangements and if they need 35 years for a full state pension it's purely by coincidence).

The second number is the amount you would get if you continue working or otherwise paying national insurance contributions until you are 67, or until your entitlement reaches the maximum of £230.25,whichever is sooner. It will go down eventually if you don't contribute for those years. I suspect that your friend is looking at the second number, and hasn't yet built up his full £230.25 entitlement. He should probably look into paying some voluntary NI contributions while he still can.0 -

Hi, all. Thanks for the replies.

So yeah my two numbers are 220.29 a week and 230.25 a week (which I believe is the full state pension).As you have noticed your state pension forecast includes two numbers.

The first number is the amount you would get if you stopped working tomorrow and never paid another penny of National Insurance. It cannot decrease unless the government makes wholesale changes to the law around how state pensions are calculated, which is very unlikely in the short term.

The latter is based on me contributing two more years before 2041 which I'll do, no problem there.

If I stop working in 2025 (aged 55) it's sounding like, if I'm reading some of the replies here right, they'll reduce my amount because I'm not paying in.

Presumably the only way to get around the not paying in NI from 55 to 67 thing is to claim benefits (which I don't want to do)? If you're not working and living on under the tax bracket for example, how much do NI payments cost per year?0 -

You have misunderstood something somewhere, it will not be reduced.minimalising said:Hi, all. Thanks for the replies.

So yeah my two numbers are 220.29 a week and 230.25 a week (which I believe is the full state pension).As you have noticed your state pension forecast includes two numbers.

The first number is the amount you would get if you stopped working tomorrow and never paid another penny of National Insurance. It cannot decrease unless the government makes wholesale changes to the law around how state pensions are calculated, which is very unlikely in the short term.

The latter is based on me contributing two more years before 2041 which I'll do, no problem there.

If I stop working in 2025 (aged 55) it's sounding like, if I'm reading some of the replies here right, they'll reduce my amount because I'm not paying in.

Presumably the only way to get around the not paying in NI from 55 to 67 thing is to claim benefits (which I don't want to do)? If you're not working and living on under the tax bracket for example, how much do NI payments cost per year?

But increasing from £220.29 to £230.25, your personal maximum, is dependent on adding two more years.

Given we are a few months into the 2025-26 tax year you may have already added one of them (worth £6.57/week) if you are working and earning decent money.

The second year adds the final £3.39.1 -

The amount you currently have will not reduce but if you make no further contributions the big green box will reduce once you get to within 2 years of retirement as there are not enough years going forward to fill the gap. You will though then get a third amount on the forecast which is the amount you can reach with filling past gaps. A voluntary class 3 year currently cots £923 increasing with CPI each and a full year is recouped in under 3 years - £923 / £6.58 = 140 wks.minimalising said:Hi, all. Thanks for the replies.

So yeah my two numbers are 220.29 a week and 230.25 a week (which I believe is the full state pension).As you have noticed your state pension forecast includes two numbers.

The first number is the amount you would get if you stopped working tomorrow and never paid another penny of National Insurance. It cannot decrease unless the government makes wholesale changes to the law around how state pensions are calculated, which is very unlikely in the short term.

The latter is based on me contributing two more years before 2041 which I'll do, no problem there.

If I stop working in 2025 (aged 55) it's sounding like, if I'm reading some of the replies here right, they'll reduce my amount because I'm not paying in.

Presumably the only way to get around the not paying in NI from 55 to 67 thing is to claim benefits (which I don't want to do)? If you're not working and living on under the tax bracket for example, how much do NI payments cost per year?

2 -

Or you can pay for the missing year(s) if you want / need that extra £10. Usually paying for one year short pays for itself within about 4 years (I think) depending on the actual triple lock increases.Your second year would probably pay for itself in 6-8 years as it's not adding quite so much to the total.0

-

Sorry

Perfect. Thanks, D&C.Dazed_and_C0nfused said:

You have misunderstood something somewhere, it will not be reduced.

0 -

This is what to look for:

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards