We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Help with some DB/SIPP/HMRC pension maths, please

Comments

-

Whoops! sorry! adjusted now.Dazed_and_C0nfused said:You should be entitled to any additional relief due based on the amount of your contribution in each tax year.

You cannot combine years or move contributions from one year to another. If you have received too much relief via your tax code for one year then you will owe tax for that year.

Could you provide the correct info though, just realised you are missing a tax year and the third entry makes no sense. Is it 22-23 or 23-24 🤔

2020-21, gross SIPP contribution £4,062.502021-22, gross SIPP contribution £1,250.002022-23, gross SIPP contribution £14,937.502023-24, gross SIPP contribution £3,337.500 -

ugh. trying again. So, for 2023-24, the adjusted tax code from 12,570 to 12,850, implies additional tax relief of £280 (so equivalent to basic rate relief on roughly £1,280 contributions). IF SIPP contributions is what the adjustment is adjusting for, and not something different.

Assuming it is adjusting for SIPP contributions, then that's HMRC's made-up figure of £1,280 contributions via the tax code, plus Vanguard/my reported figure of £3,337.50 gross contribution (£2,670 contribution plus £667.50 tax relief).

So that's £3,950 net contribution, plus £947.50 tax relief. I still don't understand where they get this "you've had relief on £6k contributions" from.

0 -

I'm not sure you fully understand pension tax relief.FloraandFauna said:ugh. trying again. So, for 2023-24, the adjusted tax code from 12,570 to 12,850, implies additional tax relief of £280 (so equivalent to basic rate relief on roughly £1,280 contributions). IF SIPP contributions is what the adjustment is adjusting for, and not something different.

Assuming it is adjusting for SIPP contributions, then that's HMRC's made-up figure of £1,280 contributions via the tax code, plus Vanguard/my reported figure of £3,337.50 gross contribution (£2,670 contribution plus £667.50 tax relief).

So that's £3,950 net contribution, plus £947.50 tax relief. I still don't understand where they get this "you've had relief on £6k contributions" from.

With a SIPP you will only ever get the 25% that the pension company adds (20% of the gross contribution) inside your pension.

HMRC should then increase your basic rate band by the amount of the gross contribution to reduce your intermediate/higher rate tax liability.

That is a personal tax saving that benefits you and never changes what was contributed to your SIPP.

Unfortunately Scottish tax rates are way more complex than the England/Wales/NI so it takes time to work out.

And don't forget whatever happened with your tax code was only ever a provisional attempt to give you the correct tax relief. You are now wanting the actual situation resolving now each tax year has ended.

Finally, why not check your Personal Tax Account to see what the make up of your current tax code is. Presumably Personal Allowance £12,570 + £280 of ???0 -

I absolutely do not understand it, no! My brain starts shallow breathing when it sees numbers.

And I am further confused by HMRC's invention of the number £6k to make it's provisional attempt at correct tax relief, as I'd never previously contributed anywhere near that amount. They have the real numbers for previous years, in real time, in front of them, so is there a good reason they choose to use invented numbers to forecast the future instead?

GovGateway says my current tax code 2025-26 is S1285L, and my tax-free allowance is £12,856, with £286 calculated from personal pension payments.

So they are assuming that this year... what? What does that £286 in increased tax-free allowance represent to them?

"Unfortunately Scottish tax rates are way more complex than the England/Wales/NI so it takes time to work out."

How might I try to do this?0 -

That's not what you said in a previous thread though. Job related expenses you have claimed will have a direct impact on the calculations, even if just for 2020-21 and 2021-22.FloraandFauna said:No, no WFH expenses/allowances/anything, nor job related expenses (civil service, so I don't claim expenses for anything).

Thanks for the confirmation about the combining - but now it makes even less sense if they're not compensating for one year, in another.

Do you know the correct position expenses wise for those two years?

It was 1282 (WFH since March alteration requested only a couple of months ago)1304 now - so clearly we're not talking enormous amounts generated by that extra 1% of contributions this year") 0

0 -

Oh! Thank you for looking that up! That would have been the Covid changes, I'd forgotten all about that! Offhand, I don't know, no, but will go back and check. Certainly I've not claimed anything for the past few years (prior to which it appears my memory shuts down).0

-

Not a full answer but there are two subtleties in how pension tax relief is calculated, presumably due to a mix of devolved and UK wide rules . Firstly they sort of ignore the 19% rate, you are given tax relief of 20% even if you'd only paid 19% tax.FloraandFauna said:

"Unfortunately Scottish tax rates are way more complex than the England/Wales/NI so it takes time to work out."

How might I try to do this?

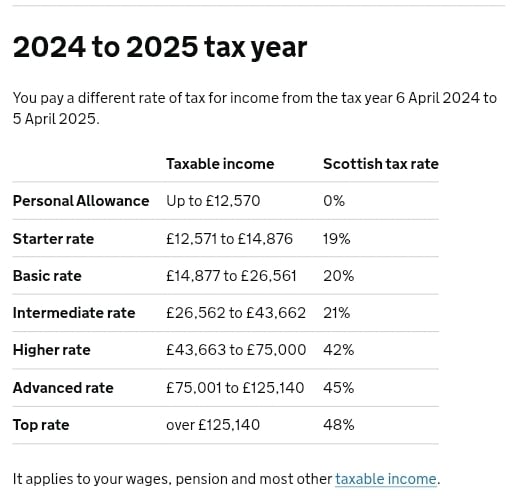

Secondly of the Scottish tax bands, it's specifically the 20% "Scottish Basic Rate" band that's increased, meaning you potentially have less taxed at 21% even if you're not saving Higher Rate. So last year the rates were ..

Using a nice round number if you paid £10,000 gross into you pension then your Intermediate 21% would start at £36,562 and Higher 42% at wouldn't start until £53,633.1 -

Oh, that's a really useful principle to know, thank you! I will try and work out:Qyburn said:

Not a full answer but there are two subtleties in how pension tax relief is calculated, presumably due to a mix of devolved and UK wide rules . Firstly they sort of ignore the 19% rate, you are given tax relief of 20% even if you'd only paid 19% tax.FloraandFauna said:

"Unfortunately Scottish tax rates are way more complex than the England/Wales/NI so it takes time to work out."

How might I try to do this?

Secondly of the Scottish tax bands, it's specifically the 20% "Scottish Basic Rate" band that's increased, meaning you potentially have less taxed at 21% even if you're not saving Higher Rate. So last year the rates were ..

Using a nice round number if you paid £10,000 gross into you pension then your Intermediate 21% would start at £36,562 and Higher 42% at wouldn't start until £53,633.

1. what I would normally have paid in each tax band

2. then how much each year's contribution will have extended the 20% tax band and so how much tax relief would be applied under that and the subsequent tax bands

3. then work out how much tax relief has been automatically received in the SIPP and how much accounted for via the tax code

4. and then if there's a difference between 2. and 3., I assume that's what I would query with HMRC. Does that sound right, or do I still completely misunderstand what's going on?

It just seems wild to me (with my no-numbers brain), that HMRC have worked out that the tax relief they say I have over-received on less than £3k contributions I've not made (so via tax code) is £491, but that the tax relief I have not received on over £8k of contributions is only worth £94, based on the same tax codes for each year.0 -

If you're working out from scratch don't base this on the tax code. The code is solely used to try and make PAYE tax you correctly. Instead have a look at what's behind the tax code, Personal Allowance of £12,570 I assume, but are there any other allowances added, or deductions (eg benefit in kind). That gets you your tax free allowance.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.6K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.7K Work, Benefits & Business

- 603.1K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards