We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

SIPPs/Pension Dilemma

ekimhoo

Posts: 8 Forumite

I have a SIPPs since 2015 and it got hammered during Covid but bounced back and June 2021 was approx £455k, now June 2025 it is £470k. Due to Covid, Russia/Ukraine war and Trump it has only gained £15k ( after £30k fund fees in 4yrs). With fees now £7.5k annually Can anyone give me some advice on what to do? Inflation has also affected the value. £455k in June 2021 would have to be £600k now. Sipps, Robo- Sipps, Personal Pension. I have little knowledge on investing and about a 5 attitude to risk, so I'm leaning towards a PP.

Mark Hughes' blue and white army

1

Comments

-

That is a lot to pay in fees? For a pension I just use the scheme run by my employer. Both I and the employer contribute to the scheme (I use salary deduction to save on NI). Fees are low because it's a deal negotiated between my employer and Aviva. And I have the option of choosing funds to invest in - or being invested in the default funds.

If I was self employed I would use a SIPP but not sure of any other reason to use a SIPP when an employer option is avavilable.1 -

People on here will tell you that what matters is not the vehicle (SIPP/PP) but the investment you have made inside the vehicle.

Fees are important - it seems like you are paying 1.5% which sounds high - how does that come about?

Has inflation really been that bad since 2021? We had two bad years but some inflation figures I have seen have been as low as 1.9%.1 -

Yikes, that's a shame.

While there was a big dip in global markets around late February 2020 (~-20%), this had fully recovered within around 3 months and then we saw an unprecedented bull run in response to global government stimulus measures. From the dip of Covid to the end of 2021, global indexes showed a roughly ~60% increase in value, it was absolutely the time to be invested. This then stayed flat for 2 years in 2022 and 2023 (with many believing this was the correction for the massive equity inflation during Covid). 2024 onwards has again been pretty good.

(when considering a fund weighted by global market cap - of course depending on your investments/diversification, performance will vary).

So to put it to you, you've paid £7.5k in fees per year, which based on your pot size suggests an annual fee in the region of 1.6%.

Unfortunately, and as you've probably realized, they've taken the majority of the growth in your investments and you're now worse off in real terms than you were in 2021 (though I make £455k in 2021 adjusted for inflation today ~£560k (+23%), not £600k as you say (+32%), meaning your money has lost 16% of the purchasing power it had).

Despite what you think regarding covid, the war, etc if you had invested in a personal pension at the start of 2021 in something like VWRL on Vanguard, you'd be sitting on around £635k now (not to rub salt on the wound).

While the public may have these impression that investing is for executives that sit in corner offices and earn 6 figure salaries while setting up offshore shell companies, it's really not as intimidating as you think, with many normal everyday people investing small amounts every month a single global index fund and outperforming most active fund managers (while paying a fraction of the fees).

It would definitely pay for you to do some research, or if still intimidated, shop around for a new IFA, though I don't know what the usual % charge is, or whether ~1.6% is normal/expensive/cheap/etc.2 -

That is a lot to pay in fees?Not really. If there is an adviser involved, then around 0.5-0.75% could be them. If managed funds are being used then those are more expensive than passive.

If the SIPP is using passive funds and no adviser is involved then its expensive.

Someone using the a popular DIY SIPP using their own brand funds could be that expensive without an adviser involved.

So, it could be a lot to pay but it could also be in the ballpark of expectation.If I was self employed I would use a SIPP but not sure of any other reason to use a SIPP when an employer option is avavilable.Plenty of other reasons, including that many SIPPs and investment options are lower charged than employer schemes.I have a SIPPs since 2015 and it got hammered during Covid but bounced back and June 2021 was approx £455k, now June 2025 it is £470k. Due to Covid, Russia/Ukraine war and Trump it has only gained £15k ( after £30k fund fees in 4yrs).You haven't told us what you are invested in but the value change gives a possible indication.

A broad basket of 100% equities would be double the value of 7 years ago now.

However, a broad basket of 100% bonds would be the same value as 7 years ago (or around 10% down over the last 5 years). Bonds suffered a 1 in 100 year loss event over Nov 2021 to Oct 2023. That period was the worst since 1915 (when reliable records began).

So, your change in value would point towards you being heavier in bonds than in equities.

Changing the provider won't make a difference. Changing the pension type won't change anything.

e.g. if you have the same investments in pension provider A, B C D etc or SIPP or PPP or SHP or Robo then you would have got the same return.

In a typical equities cycle of around 15 years, you get 5 fantastic years, 5 average years and 5 nothing or negative years, a couple of which will be larger losses. You never know the order.

All the things you have mentioned as being potential negatives are not really when it has come to equities. They were all short term dips that recovered (2015/16 had a crash along with 2018, 2020 and 2025)

Bonds play out over a longer cycle and basically from 2021 to 2023, you had the unwinding of quantitative easing due to the credit crunch. It was made worse due to the mini-energy crisis increasing the inflation spike.

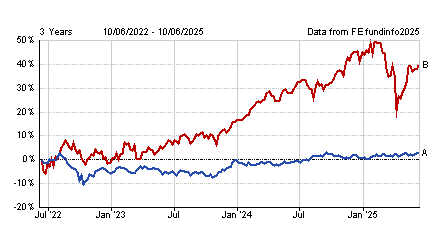

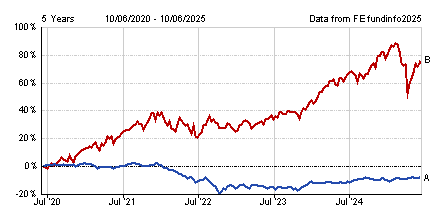

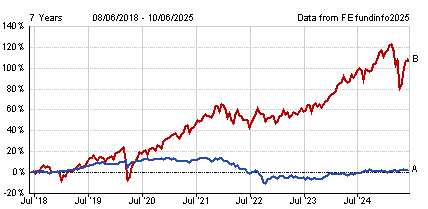

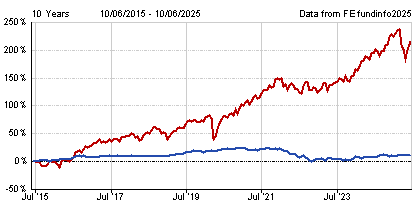

Here is how bonds vs equities have done over 3, 5, 7 and 10 years. (red equities, blue bonds)

3 years:

5 years:

7 years

10 years:

If you give us the name of your funds and percentage in each of them we can tell you why your performance has been as it has but it will almost certainly be linked to the bond vs equities ratio. Fees are a secondary issue to that.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.2 -

Inflation - from the latest monthly index figures available (April 2025), compared to 4 years earlier:

CPI: 110.1 -> 138.2. That would turn 455k to 571k

RPI: 301.1 -> 402.2 455k becomes 608k

0 -

The fees are 1.71% IFA + SIPP Platform . Using the Hargreaves Langdown Inflation Calculator £456,200 in June 2021 is equal to £603,100 today. 32.2%.DRS1 said:People on here will tell you that what matters is not the vehicle (SIPP/PP) but the investment you have made inside the vehicle.

Fees are important - it seems like you are paying 1.5% which sounds high - how does that come about?

Has inflation really been that bad since 2021? We had two bad years but some inflation figures I have seen have been as low as 1.9%.Mark Hughes' blue and white army0 -

Its a managed SIPPs with Quilter + an IFA (1.71% fees)dunstonh said:That is a lot to pay in fees?Not really. If there is an adviser involved, then around 0.5-0.75% could be them. If managed funds are being used then those are more expensive than passive.

If the SIPP is using passive funds and no adviser is involved then its expensive.

Someone using the a popular DIY SIPP using their own brand funds could be that expensive without an adviser involved.

So, it could be a lot to pay but it could also be in the ballpark of expectation.If I was self employed I would use a SIPP but not sure of any other reason to use a SIPP when an employer option is avavilable.Plenty of other reasons, including that many SIPPs and investment options are lower charged than employer schemes.I have a SIPPs since 2015 and it got hammered during Covid but bounced back and June 2021 was approx £455k, now June 2025 it is £470k. Due to Covid, Russia/Ukraine war and Trump it has only gained £15k ( after £30k fund fees in 4yrs).You haven't told us what you are invested in but the value change gives a possible indication.

A broad basket of 100% equities would be double the value of 7 years ago now.

However, a broad basket of 100% bonds would be the same value as 7 years ago (or around 10% down over the last 5 years). Bonds suffered a 1 in 100 year loss event over Nov 2021 to Oct 2023. That period was the worst since 1915 (when reliable records began).

So, your change in value would point towards you being heavier in bonds than in equities.

Changing the provider won't make a difference. Changing the pension type won't change anything.

e.g. if you have the same investments in pension provider A, B C D etc or SIPP or PPP or SHP or Robo then you would have got the same return.

In a typical equities cycle of around 15 years, you get 5 fantastic years, 5 average years and 5 nothing or negative years, a couple of which will be larger losses. You never know the order.

All the things you have mentioned as being potential negatives are not really when it has come to equities. They were all short term dips that recovered (2015/16 had a crash along with 2018, 2020 and 2025)

Bonds play out over a longer cycle and basically from 2021 to 2023, you had the unwinding of quantitative easing due to the credit crunch. It was made worse due to the mini-energy crisis increasing the inflation spike.

Here is how bonds vs equities have done over 3, 5, 7 and 10 years. (red equities, blue bonds)

3 years:

5 years:

7 years

10 years:

If you give us the name of your funds and percentage in each of them we can tell you why your performance has been as it has but it will almost certainly be linked to the bond vs equities ratio. Fees are a secondary issue to that.Mark Hughes' blue and white army1 -

When you had the initial discussions with them, did you say you only wanted low risk investments, because that could be the problem.ekimhoo said:

Its a managed SIPPs with Quilter + an IFA (1.71% fees)dunstonh said:That is a lot to pay in fees?Not really. If there is an adviser involved, then around 0.5-0.75% could be them. If managed funds are being used then those are more expensive than passive.

If the SIPP is using passive funds and no adviser is involved then its expensive.

Someone using the a popular DIY SIPP using their own brand funds could be that expensive without an adviser involved.

So, it could be a lot to pay but it could also be in the ballpark of expectation.If I was self employed I would use a SIPP but not sure of any other reason to use a SIPP when an employer option is avavilable.Plenty of other reasons, including that many SIPPs and investment options are lower charged than employer schemes.I have a SIPPs since 2015 and it got hammered during Covid but bounced back and June 2021 was approx £455k, now June 2025 it is £470k. Due to Covid, Russia/Ukraine war and Trump it has only gained £15k ( after £30k fund fees in 4yrs).You haven't told us what you are invested in but the value change gives a possible indication.

A broad basket of 100% equities would be double the value of 7 years ago now.

However, a broad basket of 100% bonds would be the same value as 7 years ago (or around 10% down over the last 5 years). Bonds suffered a 1 in 100 year loss event over Nov 2021 to Oct 2023. That period was the worst since 1915 (when reliable records began).

So, your change in value would point towards you being heavier in bonds than in equities.

Changing the provider won't make a difference. Changing the pension type won't change anything.

e.g. if you have the same investments in pension provider A, B C D etc or SIPP or PPP or SHP or Robo then you would have got the same return.

In a typical equities cycle of around 15 years, you get 5 fantastic years, 5 average years and 5 nothing or negative years, a couple of which will be larger losses. You never know the order.

All the things you have mentioned as being potential negatives are not really when it has come to equities. They were all short term dips that recovered (2015/16 had a crash along with 2018, 2020 and 2025)

Bonds play out over a longer cycle and basically from 2021 to 2023, you had the unwinding of quantitative easing due to the credit crunch. It was made worse due to the mini-energy crisis increasing the inflation spike.

Here is how bonds vs equities have done over 3, 5, 7 and 10 years. (red equities, blue bonds)

3 years:

5 years:

7 years

10 years:

If you give us the name of your funds and percentage in each of them we can tell you why your performance has been as it has but it will almost certainly be linked to the bond vs equities ratio. Fees are a secondary issue to that.0 -

Are you sure its an IFA?ekimhoo said:

Its a managed SIPPs with Quilter + an IFA (1.71% fees)dunstonh said:That is a lot to pay in fees?Not really. If there is an adviser involved, then around 0.5-0.75% could be them. If managed funds are being used then those are more expensive than passive.

If the SIPP is using passive funds and no adviser is involved then its expensive.

Someone using the a popular DIY SIPP using their own brand funds could be that expensive without an adviser involved.

So, it could be a lot to pay but it could also be in the ballpark of expectation.If I was self employed I would use a SIPP but not sure of any other reason to use a SIPP when an employer option is avavilable.Plenty of other reasons, including that many SIPPs and investment options are lower charged than employer schemes.I have a SIPPs since 2015 and it got hammered during Covid but bounced back and June 2021 was approx £455k, now June 2025 it is £470k. Due to Covid, Russia/Ukraine war and Trump it has only gained £15k ( after £30k fund fees in 4yrs).You haven't told us what you are invested in but the value change gives a possible indication.

A broad basket of 100% equities would be double the value of 7 years ago now.

However, a broad basket of 100% bonds would be the same value as 7 years ago (or around 10% down over the last 5 years). Bonds suffered a 1 in 100 year loss event over Nov 2021 to Oct 2023. That period was the worst since 1915 (when reliable records began).

So, your change in value would point towards you being heavier in bonds than in equities.

Changing the provider won't make a difference. Changing the pension type won't change anything.

e.g. if you have the same investments in pension provider A, B C D etc or SIPP or PPP or SHP or Robo then you would have got the same return.

In a typical equities cycle of around 15 years, you get 5 fantastic years, 5 average years and 5 nothing or negative years, a couple of which will be larger losses. You never know the order.

All the things you have mentioned as being potential negatives are not really when it has come to equities. They were all short term dips that recovered (2015/16 had a crash along with 2018, 2020 and 2025)

Bonds play out over a longer cycle and basically from 2021 to 2023, you had the unwinding of quantitative easing due to the credit crunch. It was made worse due to the mini-energy crisis increasing the inflation spike.

Here is how bonds vs equities have done over 3, 5, 7 and 10 years. (red equities, blue bonds)

3 years:

5 years:

7 years

10 years:

If you give us the name of your funds and percentage in each of them we can tell you why your performance has been as it has but it will almost certainly be linked to the bond vs equities ratio. Fees are a secondary issue to that.

Whilst Quilter make their platform available to IFAs, Quilter also have an in-house FA salesforce.

You can usually spot the in-house FAs rather than IFAs as the in-house ones also have to use the Quilter investment portfolios/funds.

What are the investments?I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

I'm a 'medium' The IFA scale runs from 1 to 10. I'm a '5'. On the Platform 1 to 7. I'm a 4.Albermarle said:

When you had the initial discussions with them, did you say you only wanted low risk investments, because that could be the problem.ekimhoo said:

Its a managed SIPPs with Quilter + an IFA (1.71% fees)dunstonh said:That is a lot to pay in fees?Not really. If there is an adviser involved, then around 0.5-0.75% could be them. If managed funds are being used then those are more expensive than passive.

If the SIPP is using passive funds and no adviser is involved then its expensive.

Someone using the a popular DIY SIPP using their own brand funds could be that expensive without an adviser involved.

So, it could be a lot to pay but it could also be in the ballpark of expectation.If I was self employed I would use a SIPP but not sure of any other reason to use a SIPP when an employer option is avavilable.Plenty of other reasons, including that many SIPPs and investment options are lower charged than employer schemes.I have a SIPPs since 2015 and it got hammered during Covid but bounced back and June 2021 was approx £455k, now June 2025 it is £470k. Due to Covid, Russia/Ukraine war and Trump it has only gained £15k ( after £30k fund fees in 4yrs).You haven't told us what you are invested in but the value change gives a possible indication.

A broad basket of 100% equities would be double the value of 7 years ago now.

However, a broad basket of 100% bonds would be the same value as 7 years ago (or around 10% down over the last 5 years). Bonds suffered a 1 in 100 year loss event over Nov 2021 to Oct 2023. That period was the worst since 1915 (when reliable records began).

So, your change in value would point towards you being heavier in bonds than in equities.

Changing the provider won't make a difference. Changing the pension type won't change anything.

e.g. if you have the same investments in pension provider A, B C D etc or SIPP or PPP or SHP or Robo then you would have got the same return.

In a typical equities cycle of around 15 years, you get 5 fantastic years, 5 average years and 5 nothing or negative years, a couple of which will be larger losses. You never know the order.

All the things you have mentioned as being potential negatives are not really when it has come to equities. They were all short term dips that recovered (2015/16 had a crash along with 2018, 2020 and 2025)

Bonds play out over a longer cycle and basically from 2021 to 2023, you had the unwinding of quantitative easing due to the credit crunch. It was made worse due to the mini-energy crisis increasing the inflation spike.

Here is how bonds vs equities have done over 3, 5, 7 and 10 years. (red equities, blue bonds)

3 years:

5 years:

7 years

10 years:

If you give us the name of your funds and percentage in each of them we can tell you why your performance has been as it has but it will almost certainly be linked to the bond vs equities ratio. Fees are a secondary issue to that.Mark Hughes' blue and white army1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.4K Banking & Borrowing

- 254.1K Reduce Debt & Boost Income

- 455K Spending & Discounts

- 246.5K Work, Benefits & Business

- 602.8K Mortgages, Homes & Bills

- 178K Life & Family

- 260.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards