We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

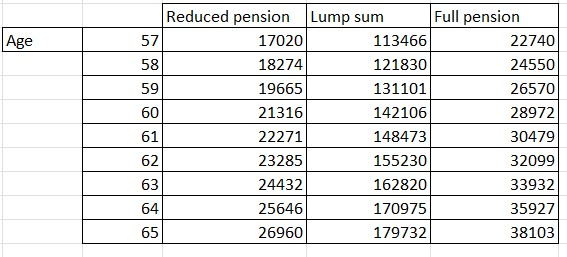

Timing and order of DB access and DC withdrawal

Comments

-

The other question (which can be for another time) is how to draw down £23k in April 2027 on 1257L making a gross income of £50k and pay 20% tax. I’m sure this has been covered loads.0

-

One of things for me is that sometimes people forget that the DB option is 'free' cash. What I mean by that is that once you start collecting it it does not reduce any 'pot' and is guarenteed. It is all yours. What I have worked out is how many years of DB pension have I had as income taking 2, 3, 4, 5 etc years total early and then how that compares to the DB sum I would have had at either age 65/67 pay out date, ie official retirement age (depending on the scheme's age full pay out date).

And then work out how many years I would need to live before I was in break-even by not taking it early? eg £14kpa pension at 65 gives me £28k income over 2 years. Taking pension at 67 gives me c£15kpa, but I have already earned 2 x £14k = £28k by age 67. Compare that to no guarenteed income for two years and and extra c£1k two years later. How many years before being 'in profit'?

Because of this I plan to retire at 62 (c£24kpa net needed) in c2years time - Cash ISA/DC SIPP fund to 65 (personal tax fee allowance used), then take x2 DB pensions at 65 (total c£14kpa of which one pays out the full amount at 65 - no cash lump sums) and then I am in approx equal/in surplus of needed income amount when STA pension comes into effect at 67.

This is a fairly simple methodolgy, I am not good with communitation rates etc and not including inflation, rise/fall in pots, CPI/RPI/capped pension increase and also does depend on whether you need you need a lump sum to pay off mortagage, house repairs, new car etc etc. Do you need to fund any of these expenses and can get adequatly by before STA kicks in and before needing to fund these expenses, ie potentially funding from the STA payment each year thereafter? For me, I am fortunate that the mortgage is now paid off and I am carrying no major debt with 2 years to go. So fingers crossed for my plan.

@Cobbler_tone the above is not meant to derail your thread but supports the argument about DB pensions and taking them earlier - with the (total sum) money you potentially loose by not taking them earlier - the diffence for me is really not a lot per month by taking it at 65 (all the time increasing by CPI/RPI/capped depending on the scheme) and gives me options for the earlier retirement, which you are considering and then to 67 when the STA kicks in. I appreciate that I have a mixture of DB and DC pension to work with. Can you cash fund the first couple or so of years? Also to think about - as you have considered, do you need the full cash lump sum from the DB or could you leave some in to give you a bigger per annum pension guarenteed when it does pay out?

0 -

Thank you. With the greatest respect I’m probably one step ahead. I have a model that does factor the difference in taking the pension at different ages with an RPI factors of between 1-5%, plus the impacts of lump sums. Taking it early can have the difference of up to £250k (adverse) by the time you are 90. The common ‘break even’ point is mid 70’s but clearly depends on the age of commencement.Itsme01x said:One of things for me is that sometimes people forget that the DB option is 'free' cash. What I mean by that is that once you start collecting it it does not reduce any 'pot' and is guarenteed. It is all yours. What I have worked out is how many years of DB pension have I had as income taking 2, 3, 4, 5 etc years total early and then how that compares to the DB sum I would have had at either age 65/67 pay out date, ie official retirement age (depending on the scheme's age full pay out date).

And then work out how many years I would need to live before I was in break-even by not taking it early? eg £14kpa pension at 65 gives me £28k income over 2 years. Taking pension at 67 gives me c£15kpa, but I have already earned 2 x £14k = £28k by age 67. Compare that to no guarenteed income for two years and and extra c£1k two years later. How many years before being 'in profit'?

Because of this I plan to retire at 62 (c£24kpa net needed) in c2years time - Cash ISA/DC SIPP fund to 65 (personal tax fee allowance used), then take x2 DB pensions at 65 (total c£14kpa of which one pays out the full amount at 65 - no cash lump sums) and then I am in approx equal/in surplus of needed income amount when STA pension comes into effect at 67.

This is a fairly simple methodolgy, I am not good with communitation rates etc and not including inflation, rise/fall in pots, CPI/RPI/capped pension increase and also does depend on whether you need you need a lump sum to pay off mortagage, house repairs, new car etc etc. Do you need to fund any of these expenses and can get adequatly by before STA kicks in and before needing to fund these expenses, ie potentially funding from the STA payment each year thereafter? For me, I am fortunate that the mortgage is now paid off and I am carrying no major debt with 2 years to go. So fingers crossed for my plan.

@Cobbler_tone the above is not meant to derail your thread but supports the argument about DB pensions and taking them earlier - with the (total sum) money you potentially loose by not taking them earlier - the diffence for me is really not a lot per month by taking it at 65 (all the time increasing by CPI/RPI/capped depending on the scheme) and gives me options for the earlier retirement, which you are considering and then to 67 when the STA kicks in. I appreciate that I have a mixture of DB and DC pension to work with. Can you cash fund the first couple or so of years? Also to think about - as you have considered, do you need the full cash lump sum from the DB or could you leave some in to give you a bigger per annum pension guarenteed when it does pay out?

I don’t get too wrapped up in it. I have been through so much in my life and tend not to look back. I think there is pretty much zero chance I would ever look back at 80 (if I am lucky enough to get there) and say “I would have drawn another £150k across the last 23 years if I’d held out”.

Life has too many changes and if anything money will appear from elsewhere. I never factor it in but I have 3 sources of potential inheritance to come for example. Look back 20 years and where your life was. It is also the cost not having to work and getting extra years of leisure. That’s the price of that. The ‘one more year’ dilemma is real!

So of course I wanted to fully understand that and the important thing is being happy with what you have at any given point and the impact of doing so. For me, I’m happy.

My biggest factor will be deciding whether it is right at the time to fully walk away from work. The emotional factor is the most difficult one to step up to in my case.3 -

If you only need £2k 'ish a month then either of option 3 or 4 would meet your needs?

DB Option 3: BPO Pension from 57-67 £22,150, pension from 67 £10,200 with £147,700 (25% PCLS)

Option3 plus supplementing £4K a year from your DC pot will give you a guaranteed £2k with £150k PCLS at 67 and from SP age your monthly income is the same. Depending on how you take money from your DC then you might need to take slightly less than £4K if using UFPLS.

DB Option 4: BPO (no lump sum) from 57-67 £29,729, pension from 67 £17,750

Option4 gives you a slightly higher £2.5k guaranteed without needing to touch your DC pot at all and from SP age your monthly income is the same, and you can still take a £32k tax free lump sum straight away from your DC if wanted.

So I think it boils down to what will you do with a £150k PCLS when you reach SP age? Is it something you would be happy waiting for or would you rather have the extra £7k a year guaranteed for life but starting ten years earlier?

Another way to look at it is let's say you will live for 30 years until age 87 if you take option 4 then you will get an extra £7k *30 = £210k vs £147k at 67, and you won't have needed to touch your DC pot at all so have a larger rainy day fund readily available.

0 -

Thank you. I understand all of the rationale.GenX0212 said:If you only need £2k 'ish a month then either of option 3 or 4 would meet your needs?DB Option 3: BPO Pension from 57-67 £22,150, pension from 67 £10,200 with £147,700 (25% PCLS)

Option3 plus supplementing £4K a year from your DC pot will give you a guaranteed £2k with £150k PCLS at 67 and from SP age your monthly income is the same. Depending on how you take money from your DC then you might need to take slightly less than £4K if using UFPLS.

DB Option 4: BPO (no lump sum) from 57-67 £29,729, pension from 67 £17,750

Option4 gives you a slightly higher £2.5k guaranteed without needing to touch your DC pot at all and from SP age your monthly income is the same, and you can still take a £32k tax free lump sum straight away from your DC if wanted.

So I think it boils down to what will you do with a £150k PCLS when you reach SP age? Is it something you would be happy waiting for or would you rather have the extra £7k a year guaranteed for life but starting ten years earlier?

Another way to look at it is let's say you will live for 30 years until age 87 if you take option 4 then you will get an extra £7k *30 = £210k vs £147k at 67, and you won't have needed to touch your DC pot at all so have a larger rainy day fund readily available.

A hybrid of option 3 is the likely route. A more modest lump sum but elevated pension. I don't want/need £150k on day 1. I'm happy to have enough to spend as I see fit with no major (planned) outlays, maybe a car. I might decide I want to throw £20k on some dentistry?!

The greatest security is clearly option 4 to get the healthiest level of guaranteed income, whilst I could draw the DC down over 4-5 years as savings. I've toyed with this but do want the buffer and flex to spend, or gift out.

It seems simple now but didn't when I first asked the question, hence the benefit of getting outside views.1 -

Thank you.Shadyocuk said:My first task would be to get an idea of the timescale from requesting the DB to actual payouts , then delay the decision until just before needing to make it.

Given that you show option 1 would increase in value by 7.9% if deferred for one year , have you got the figures for how the other options would increase and what the cummutation rates would be if also deferred by 1 or more years?

If all options increased by a similar rate then I would be tempted to fund year 1 , possibly years 2 and 3 from the DC pot and take the baked in increase , a lot would depend on how this alters the lump sums available and the likely timescales between requesting and receiving payouts, if a short timescale then you could reguard the deferred DB Lump sum as your £100K fund and if you took funds from the DC pot by monthly UFPLS , you could switch to the DB at when ever the sweet spot is or when ever you "need" the lump sum.

I understand the reduction factors and on an old thread was pondering the merits of taking it now. You will see some people class it as a 'no brainer' but I am all over the modelling of the various impacts, without fully knowing what RPI is going to do.

The 'sweet spot' can only be known if you know your expiry date, which none of us do. Even then, it isn't about pounds and pence, it is about setting the rest of your life up at your desired retirement date, which doesn't have to be a hard stop.

I haven't ruled anything out. Next year (which is my current thinking), instead of throwing the towel in, I could look to phase down to a 3 day week and maintain my benefits and plenty of income not to worry about touching my pensions, instead continuing to pay in. I don't know where my head will be then. I'm at the stage that my health, well being and having enough money to live comfortably (not £60k comfortably) comes before anything else.

The important thing is I know I could retire (the OH already is at 54, no kid she figures she has earnt it), even with today's level of spousal pension over over £10k PA factored in. They are all considerations I've factored in.

I've got these numbers modelled to death with different levels of RPI (plus the bridged options) but appreciate the timing, impact and options of DC too. I repeat that this forum has been invaluable in my learning and thinking, so appreciate the feedback and advice given.

0 -

Phasing into retirement is a good approach. Go down to 4 then 3, 2 days work per week over a year or two.A little FIRE lights the cigar1

-

Now favouring option 2, which mitigates risk.

Take tax free cash from DB and DC, with 10 year fixed term annuity with £100k (balance of DC pot). Gives a lifetime income of around £30k PA once state pension kicks in, plus decent lump sum. I don’t want to faff around with investments.

My DB will build and not drop at 67.

I’m assuming most fixed term annuity products need an adviser? I ran the calculation on Moneyhelper.0 -

Option 2 is the no brainer. It would be silly to use £100k to purchase an annuity when the PCLS alone could cover the ten year bridging gap. This will hit your £26k annual requirements easily until state pension steps in.

1 -

When you have a significant DB pension and also State Pension (guaranteed income) I’m struggling to see the benefit of purchasing an annuity? It seems like you are swapping your PCLS for an annuity (no inflation protection) when you’d be better off keeping it in the pension (some inflation protection).Cobbler_tone said:Now favouring option 2, which mitigates risk.

Take tax free cash from DB and DC, with 10 year fixed term annuity with £100k (balance of DC pot). Gives a lifetime income of around £30k PA once state pension kicks in, plus decent lump sum. I don’t want to faff around with investments.

My DB will build and not drop at 67.

I’m assuming most fixed term annuity products need an adviser? I ran the calculation on Moneyhelper.Option 2 seems the worst of the lot. To ‘mitigate risk’ Option 4 seems like the best bet. Guaranteed income, above the level you require, (around £30k) for the rest of your life - the DC pot adding a bit of spending money.If you were adamant on the needing £100k cash, then take some PCLS. £37k from the DC pot and £63k from the DB pension and see what that gives you in yearly income. That would be somewhere between Option 3 and Option 4. A touch more risk but not as much risk as Option 2.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards