We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Max SIPP Pension Contribution

Sayr

Posts: 12 Forumite

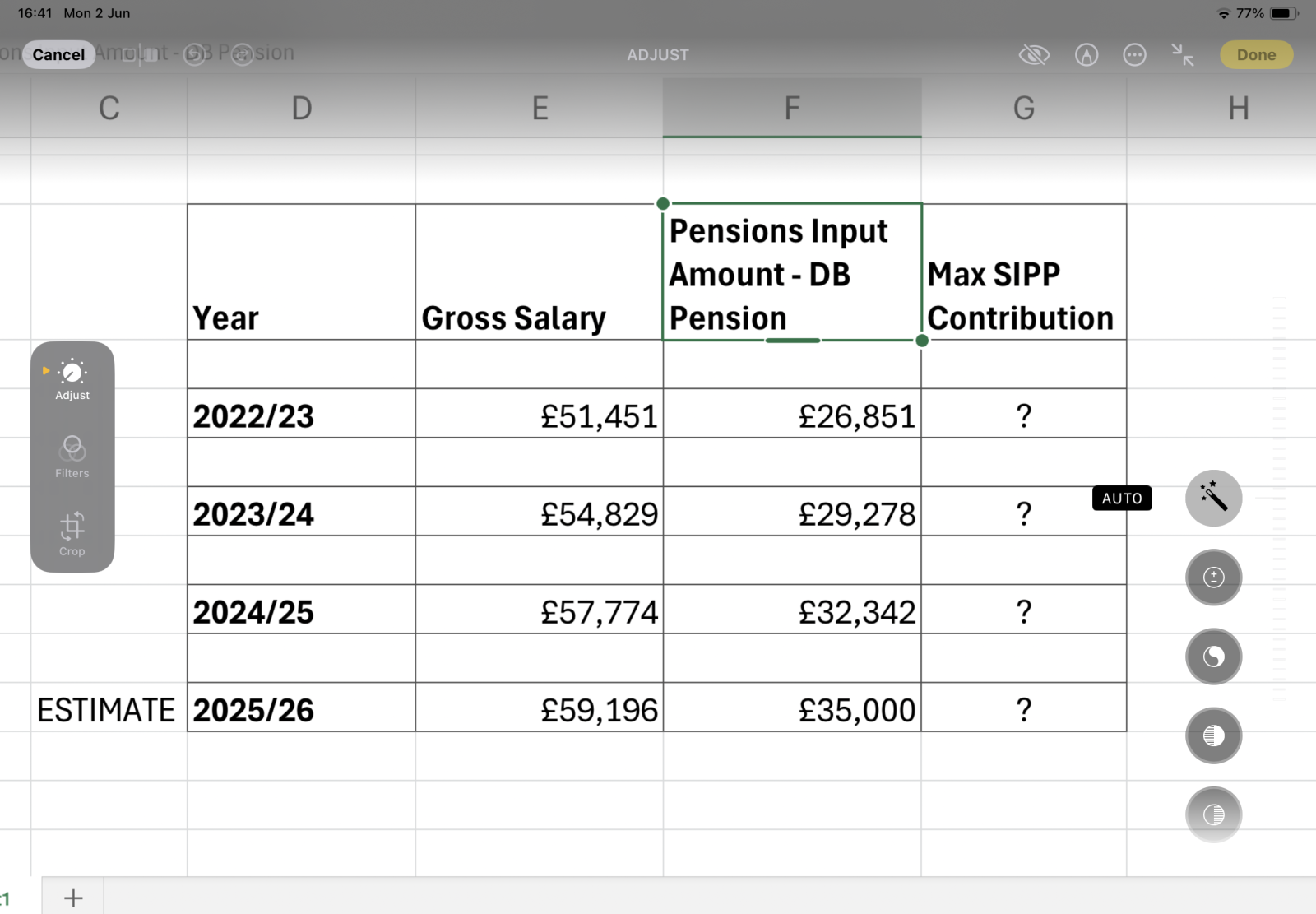

I save into a local authority DB pension and AVC. I have also opened a SIPP.

I plan to retire this financial year hopefully.

Based on my local authority salary and calculated Pension Input Amount (see table), what is the maximum I can invest before I retire into my SIPP (including any unused SIPP contributions from previous financial years) to get the maximum tax relief?

0

Comments

-

How much have you put into your AVC, this year and previous?0

-

(including any unused SIPP contributions from previous financial years)

You can only get tax relief on this tax years contributions, there is no such thing as retrospective tax relief, although a lot of people think there is.0 -

AVC:

22/23 - £12k

23/24- £16.1k

24/25 - £19.9k

25/26 £2.2k per month - £4.4k so far.

I really thought you were able to go back 3 years to utilise unused amounts for SIPPs.

Any further thoughts on how much I can contribute then into my SIPP based on the numbers in the spreadsheet?

Thanks.0 -

Nope, that was abolished a very long time ago.Sayr said:AVC:

22/23 - £12k

23/24- £16.1k

24/25 - £19.9k

25/26 £2.2k per month - £4.4k so far.

I really thought you were able to go back 3 years to utilise unused amounts for SIPPs.

Any further thoughts on how much I can contribute then into my SIPP based on the numbers in the spreadsheet?

Thanks.

You can sometimes use unused relief from earlier years to contribute more in the current tax year. But any tax relief due will be by reference to your current tax year income, not what you earned in previous tax years.0 -

You can utilise unused annual allowances from previous tax years, but with constraints.Sayr said:AVC:

22/23 - £12k

23/24- £16.1k

24/25 - £19.9k

25/26 £2.2k per month - £4.4k so far.

I really thought you were able to go back 3 years to utilise unused amounts for SIPPs.

Any further thoughts on how much I can contribute then into my SIPP based on the numbers in the spreadsheet?

Thanks.

So, for example, if you only put £40K (gross) into your pension last tax year, you can carry forward the unused £20K and pay £60K (you have to use this years allowance first) + £20K into your pension in this tax year.

But, this is constrained by your earnings this year. So you need to have earned £80K this year to put £80K gross in this year.

More details: https://www.moneyhelper.org.uk/en/pensions-and-retirement/tax-and-pensions/carry-forward

Edit: Looking at your figures, you're already on track for your contributions to exceed your salary this year (£35K Input amount + 12 * £2.2K) = £61,400. You can only contribute (gross) £59,196, or whatever your salary this year turns out to be. If you exceed this, you'll have to pay an annual allowance tax charge on the amount greater than your salary.0 -

Thanks. My DB pension provider has confirmed that my Pension Input Amount prediction for 2025/26 (a total of £35k) INCLUDES the 12 planned AVC amounts I intend to pay each month this year.1

-

Are AVC contributions gross or net?

0 -

My AVC amount leaves my monthly pay as a salary sacrifice and then my pay is taxed, so I have benefited from paying tax.Regarding my original question, I'm still struggling to understand how much money I can actually put into my SIPP given the Pension Input Amounts I have quoted from my DB pension provider. As noted, I have not retired yet and want to maximise my SIPP pension without exceeding any limits. Thanks.0

-

It's not helping that you have quoted your gross salary. Although that is doubtless relevant for your PIA calculation it's your taxable earnings which are more important when it comes to how much you can contribute.Sayr said:My AVC amount leaves my monthly pay as a salary sacrifice and then my pay is taxed, so I have benefited from paying tax.Regarding my original question, I'm still struggling to understand how much money I can actually put into my SIPP given the Pension Input Amounts I have quoted from my DB pension provider. As noted, I have not retired yet and want to maximise my SIPP pension without exceeding any limits. Thanks.

The mix of your normal LGPS(?) contributions and salary sacrifice is going to mean your estimated taxable pay is significantly less than £59k.

2 -

But if you use salary sacrifice for all contributions to the LGPS then don't the sums become very simple? You can contribute whatever is left of your salary (your taxable earnings) to the SIPP.

Now that could mean you go over the £60k annual allowance this tax year by £34196 (assuming the £59k figure is actually what is left.

That means you'd need to use up earlier years headroom on the annual allowance but that does not seem to be a problem. I think you have over £71k for 22/3 - 24/5.

Things to watch out for

Your taxable earnings may be less than £59 as mentioned above

You cannot pay the whole lot into the SIPP because you need to allow for the tax relief claimed by the SIPP so multiply whatever the figure is by 0.8.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards