We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

I’m £50k in debt Scotland

Comments

-

chrisjvc1 said:I may sound thick, but why not just take a consolidation loan and have one payment instead of 7. I know I’ll pay more interest but at least I’ll be £400 a month better offThat truly is the worst sort of debt.The credit cards are the way the lenders lure you into spending beyond your means, the interest can be zero percent with perhaps a 3% fee, but that is before the trap has got you.The consolidation loan is fixed interest, there is usually hardly any benefit in paying it off early and they truly have you by the short and curlies.There is no judgement here, we have all been where you are now or worse (I had £90k myself but did not pay a penny back because they were too slow to offer 60% off. By the time they did I was on the home run to the debt being statute barred so I stuck it out.Until you can be honest about how you ran up this debt you can't expect appropriate advice, you have several big loans which I thought could be consolidation hence I asked the questions.I think you could look at the scenario of interest you will pay on the following MSE page.The thing about that calculator is it speaks the truth, if you have self discipline of a ninja and pay off as much as you can, cutting back your spending for as long as it takes then you can get out with your credit score intact.If you know in your heart of hearts you can't or won't cut back then DMP and forget about credit, I opted out of credit participation. I recognised the error of my ways and circumstances that were beyond my control and knew I never wanted to be in that place again. Now I live so frugally that I might join the monks in the Monastery, I even save money to help out family members, pay for my funeral (self funded) and send money to Ukrainian causes.You have had a lot of good advice on here, review them, tell more, ask more and make a decision about your way forward.1

-

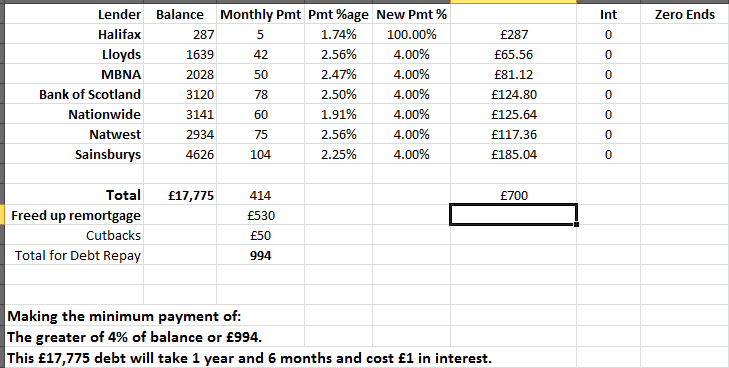

There's no requirement for posters asking for help to behave in any particular way or to answer any questions.DankVielen said:DankVielen said:chrisjvc1 said:Hi folks, I know this is all my own doing but after a difficult divorce I bought a small house that needed some work. To cut a long story short I now have 8 credit cards, with £17k of debt, most of which is on 0% for a year. I have 3 loans, one with 8k left, one with 7k left and one with 19k left. I earn £50k a year, I can just cover all my payments but have about £100 spare for food……I don’t want to loose my house but either I sell up or take out a 7 year loan for £29k which will mean I can pay off all my credit cards and 2 loans, this will take my payments for all that from £870 a month to £538 giving me some money to live on. Any advice pleaseFirst of all, well done for recognising you have a problem and coming to get help, this is not always easy.Before deciding on a debt solution I think there needs to be some analysis of where the money went.I have had family and friends in London buy a flat to add a bedroom, it was the only way they could afford to get to a 2 bed flat to start a family. They both used up to 6 credit cards each to fund the development of the property and that was after they had saved up around £40k and cashed in ISA's etc. When one went to remortgage to pay off all this debt (as property value was not £250k higher) the bank refused the mortgage because apparently they do not like to use a mortgage for this purpose. 6 months later they went to a broker who got them a deal to remortgage and they paid off every penny of debt, even the zero percent.House value (Gross)..................... 163000Mortgage....................................... 144000Therefore if your debt was 90% spent on the property and the property now has a higher value then I would suggest a remortgage, even if you have to pay above the going rate. However, unless you were quoting the old house valuation then it seems as if this was a money pit and you made poor decisions on developers.If we consider that theAmount short for making debt repayments. -278and you do only have around £20,000 of equity then the simple solution is to remortgage the house, pay off the Zopa thus reducing your outgoings by £415Zopa...........................19000.....415.......11.2This would give you an extra £137 a month to attack the Nationwide and HalifaxNationwide.................8523......189.......8Halifax .......................6327......189.......7.8If now that you have done up the house worth more you could add and extra £15k and pay off the Nationwide and Halifax too.This would release a further £398 a month so an extra £530 a month to pare down your zero percent debt.If you use can remortgage and then use this £530 you could have the whole debt paid off in 18 months If you had the dates when the zero rate expires it would be possible to reorder the cards so that you pay off the ones that have debt expiring first.If remortgage is NOT and option then let's work through other options, but first consider the ROOT CAUSE of the debt.If the Zopa debt for example was to already consolidate previous overspending then I think you need to address that problem. There is no judgement here, many people have gambling habits, paying of an Ex's debt and so on. What you need to know is whether the root cause could happen again?Normally the way I would approach an SOA like yours is on how much disposable income you have without debt and yours seems pretty healthy.So the next question is whether you mind trashing your credit record for 6 years to get a reduced rate on this debt?If the answer to that is that you want to preserve your credit record then there are two things to check,1. Is there any discount for early repayment of any loan?2. How much credit do you have on the zero percent cards and3, When do the zero rate expire.If there is some capacity on the zero percent cards and there is a discount for early repayment then it makes sense to use that capacity to reduce the debts that are costing you the most. You do this by putting your monthly spending of bills & food on the zero percent card and then each day move what you spent on the zero card to a savings account and then pay those accumulated amounts from the savings to the debt with the highest interest rate (if you benefit from early repayment).The three that stand out areZopa...........................19000......415.......11.2Nationwide...................8523......189.........8Halifax .........................6327......189........7.8

If you had the dates when the zero rate expires it would be possible to reorder the cards so that you pay off the ones that have debt expiring first.If remortgage is NOT and option then let's work through other options, but first consider the ROOT CAUSE of the debt.If the Zopa debt for example was to already consolidate previous overspending then I think you need to address that problem. There is no judgement here, many people have gambling habits, paying of an Ex's debt and so on. What you need to know is whether the root cause could happen again?Normally the way I would approach an SOA like yours is on how much disposable income you have without debt and yours seems pretty healthy.So the next question is whether you mind trashing your credit record for 6 years to get a reduced rate on this debt?If the answer to that is that you want to preserve your credit record then there are two things to check,1. Is there any discount for early repayment of any loan?2. How much credit do you have on the zero percent cards and3, When do the zero rate expire.If there is some capacity on the zero percent cards and there is a discount for early repayment then it makes sense to use that capacity to reduce the debts that are costing you the most. You do this by putting your monthly spending of bills & food on the zero percent card and then each day move what you spent on the zero card to a savings account and then pay those accumulated amounts from the savings to the debt with the highest interest rate (if you benefit from early repayment).The three that stand out areZopa...........................19000......415.......11.2Nationwide...................8523......189.........8Halifax .........................6327......189........7.8

If Zopa is a fixed rate loan and does not cost less if you pay off early then Nationwide and/or Halifax would be where you spend it, assuming they too reduce.If neither reduce then still use up your credit limit but use the money to pay off the zero percent that ends earliest. This will reduce the risk of you having to pay 24% when an offer expires and you are deemed over extended and can't transfer to another zero percent card.On personal spending these are the areas to question:Water rates............................... 0 ----> This should be payableMobile phone.......................... 12----> Switch to Lebara £3 month dealTV Licence.............................. 15 ----> £0 Dump BBC & Live TVSatellite/Cable TV.................... 40 ---> Dump all pay TVGroceries etc. ....................... 280 ----> Try to cut this by 20% minimum

Petrol/diesel........................... 200 ---->Road tax.................................... 0 ----> Is this another omission, how can you spend £200 on petrol but £0 on this?Haircuts................................... 20 ----> Get a trimmer for £18 at Tesco

If you were going to DMP your debt then you might take a different approach and pare down your mortgage with any spare cash but that would be a bit of a dodgy thing to do. You are not in that desperate a state yet.

DMP will trash your credit record but you should be able to remortgage at variable rate with existing lender when the promotion rate expires (or that may have happened). If your mortgage discount has reverted it would be a good reason to remortgage as rates are coming down.It seems some did not appreciate my advice, it did have some caveats, it started withBefore deciding on a debt solution I think there needs to be some analysis of where the money went.For example if you have a gambling problem then obviously securing your debt on your house would be nuts.However, if the debt was all accrued on fixing up the property (as implied in your OP) then it would seem fit and proper to move development costs to the mortgage, if you had got a mortgage with an extra £50k to do it up then I see no difference.I also saidSo the next question is whether you mind trashing your credit record for 6 years to get a reduced rate on this debt?If you are going to be doing other develop and sell on property then trashing your credit would not be a good idea.I also clarified for a 3rd time

If the answer to that is that you want to preserve your credit record then there are two things to check,1. Is there any discount for early repayment of any loan?2. How much credit do you have on the zero percent cards and3, When do the zero rate expire.You have not answered this or any of the questions so hard to give further advice which may be the same as others about getting a DMPchrisjvc1 said:It’s difficult to know what to do next.I do not think you would get better advice in a CAB, just perhaps a reality check.I have not been here very long, but I have come to truly respect the regulars posting on this section of the forum, their experience far outweighs mine.People have put in a lot of effort and you comment back with short answers which suggests to me that you may not quite be ready to be open about how you got into this position, which leads me to concur with others that DMP may be the best route for you.

I appreciate that you are trying to help,but it may be worth considering the following -

- the reason for the debt is useful for someone in debt to understand to help them address the root cause, but has very little bearing on the best method to address the debt

- this is usually indicated by their soa, plus knowledge of facts which might rule out some options, eg that their job relies on not having a ccj or going bankrupt or that they have an imminent change in their soa eg income reduction due to job loss, maternity leave

- converting unsecured debt into secured debt increases the risk of losing their home should their income fall or outgoings increase. If that happens, they can ignore unsecured debt, but they still need to keep paying the secured debt or they will lose their home. It doesn't matter if the debt was due to gambling or house improvements, this risk is still the same.

- there is no decent credit record to preserve if a poster cannot cover their minimum payments (which the SOA tells us)

- if you are getting frustrated at an op, that is the time to step away and take a break. On this board we are here to help where we can, not demand that our questions are answered.Statement of Affairs (SOA) link: https://www.lemonfool.co.uk/financecalculators/soa.phpFor free, non-judgemental debt advice, try: Stepchange or National Debtline. Beware fee charging companies with similar names.5 -

There isn’t really a lot to tell I’m afraid. I bought House and then spent 25K replacing ceilings etc after finding asbestos. I also bought a car for Work. I was also setting up home from having nothing so it cost a bit to get going.

I don’t have a gambling problem or a drinking problem or any other kind of problem. I’ve just got myself a mess and it has got worse from there. The largest loan I have was taken out to consolidate some credit cards that were coming to the end of their zero percent offer. Last month I managed to change most of my cards to further 0% offers for a year.

So yes I did think a consolidation loan would be the easiest option as it would clear most of my payments and just give me one to concentrate on. I was aware that will be paying back a lot more money but thought it was the easiest way to keep my credit rating decent And stop the bailiffs coming to the door. I had hoped to move house in a couple of years and buy somewhere near the kids. I’m guessing a dmp would put an end to that hope.

I don’t live an exciting life and don’t have lots of massive outgoings, but I am caught in a trap now and I’m unsure of the way out. I’m grateful for everybody’s input on this forum but there are a few different opinions and it makes it hard to know which one to pick .

1 -

Ok, well it's ultimately your decision, why don't you write out the options in a post and do pros and cons of each.Statement of Affairs (SOA) link: https://www.lemonfool.co.uk/financecalculators/soa.phpFor free, non-judgemental debt advice, try: Stepchange or National Debtline. Beware fee charging companies with similar names.2

-

Chris, take a look at the Dave Ramsey baby Steps, listen to the podcasts or on youtube, I used the steps as a simple and clear plan to get myself out of debt after a bad divorce (financially) I bought a new home and now have savings and an emergency fund as well as a fairly decent pension, I'm 57.

The baby steps was like a recipe for me, simple to follow and that mad my mind clearer, having a plan is 50% of the solution. The it snowballed into an obsession and total new financial me!I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert

Baby Step 6/7 . £18000 saved and invested. £47,000 deposit paid on new home DEBT FREE !!!1 -

I didn’t want to read and run, well done for coming here for help!chrisjvc1 said:I may sound thick, but why not just take a consolidation loan and have one payment instead of 7. I know I’ll pay more interest but at least I’ll be £400 a month better off

reading your posts I agree with the DMP route, it is still one payment instead of 7 but it will not put your house at risk.

you've spent so much time and money to make it yours so I would fight tooth and nail to secure it.

if it helps I’m 5 years into a DMP and it wasn’t easy, I got a few consolidation loans throughout my 20’s and 30’s and they worked for a time. Trouble was it was too easy to just keep living the lifestyle I wanted as I had spare money again.

The DMP has been a real eye opener as it took away the ability to just keep turning a blind eye to my outgoings. Having no easy access to credit hurt for a while as I didn’t read on these forums before I entered the DMP so didn’t know to save an emergency fund whilst waiting for the defaults but something clicked about a year or 2 in and I started saving.Honestly go for the DMP, 6 years goes by in the blink of an eye when you aren’t living month to month, paycheck to paycheck

Good luck 🍀The 365 Day 1p Challenge 2026 #26 £437.90/£667.95Save £12k in 2026 #12 £5288.83/£7500

Car Loan Dec 25- £14,114.74 (60mth)

Jan 26- £9857.07 (42mth)

Feb 26- £6438.83 (28mth)

Mar 26- £5930.87 (26mth)

Apr 26 - £4158.00 (18mth)

May 26 - £3917.00 (17mth)1 -

For clarity, a dmp doesn't mean one payment, but doing a dmp through a charity such as Stepchange (or a dmp company, but this is not recommended as they will take some of your money in fees) will, as you just give them one payment and they will divide it between your debts.Statement of Affairs (SOA) link: https://www.lemonfool.co.uk/financecalculators/soa.phpFor free, non-judgemental debt advice, try: Stepchange or National Debtline. Beware fee charging companies with similar names.1

-

Yes sorry I should have explained that better, thank youkimwp said:For clarity, a dmp doesn't mean one payment, but doing a dmp through a charity such as Stepchange (or a dmp company, but this is not recommended as they will take some of your money in fees) will, as you just give them one payment and they will divide it between your debts.The 365 Day 1p Challenge 2026 #26 £437.90/£667.95Save £12k in 2026 #12 £5288.83/£7500

Car Loan Dec 25- £14,114.74 (60mth)

Jan 26- £9857.07 (42mth)

Feb 26- £6438.83 (28mth)

Mar 26- £5930.87 (26mth)

Apr 26 - £4158.00 (18mth)

May 26 - £3917.00 (17mth)1 -

I don't see any real advantage in one payment instead of 7. Just set up standing orders and let them run

With 51k debt and around £1000 available, the op can clear this in under 6 years, which is why an IVA has no advantages. Too much surplus for a DRO, and bankruptcy risks the house.

So I can't see this business of too many options.

The emergency fund will build nicely while waiting for the defaults and any savings/windfalls will add to this so settlement deals may shorten the timescale later3 -

Chris, if fatbelly (or sourcrates) recommended a route to me to manage debt, I would follow it, they know what they are talking about.fatbelly said:I don't see any real advantage in one payment instead of 7. Just set up standing orders and let them run

With 51k debt and around £1000 available, the op can clear this in under 6 years, which is why an IVA has no advantages. Too much surplus for a DRO, and bankruptcy risks the house.

So I can't see this business of too many options.

The emergency fund will build nicely while waiting for the defaults and any savings/windfalls will add to this so settlement deals may shorten the timescale laterStatement of Affairs (SOA) link: https://www.lemonfool.co.uk/financecalculators/soa.phpFor free, non-judgemental debt advice, try: Stepchange or National Debtline. Beware fee charging companies with similar names.3

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards