We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Questions about a DMP and £50k in debt

Comments

-

Hey everyone, checking back in on my next steps if I could please.

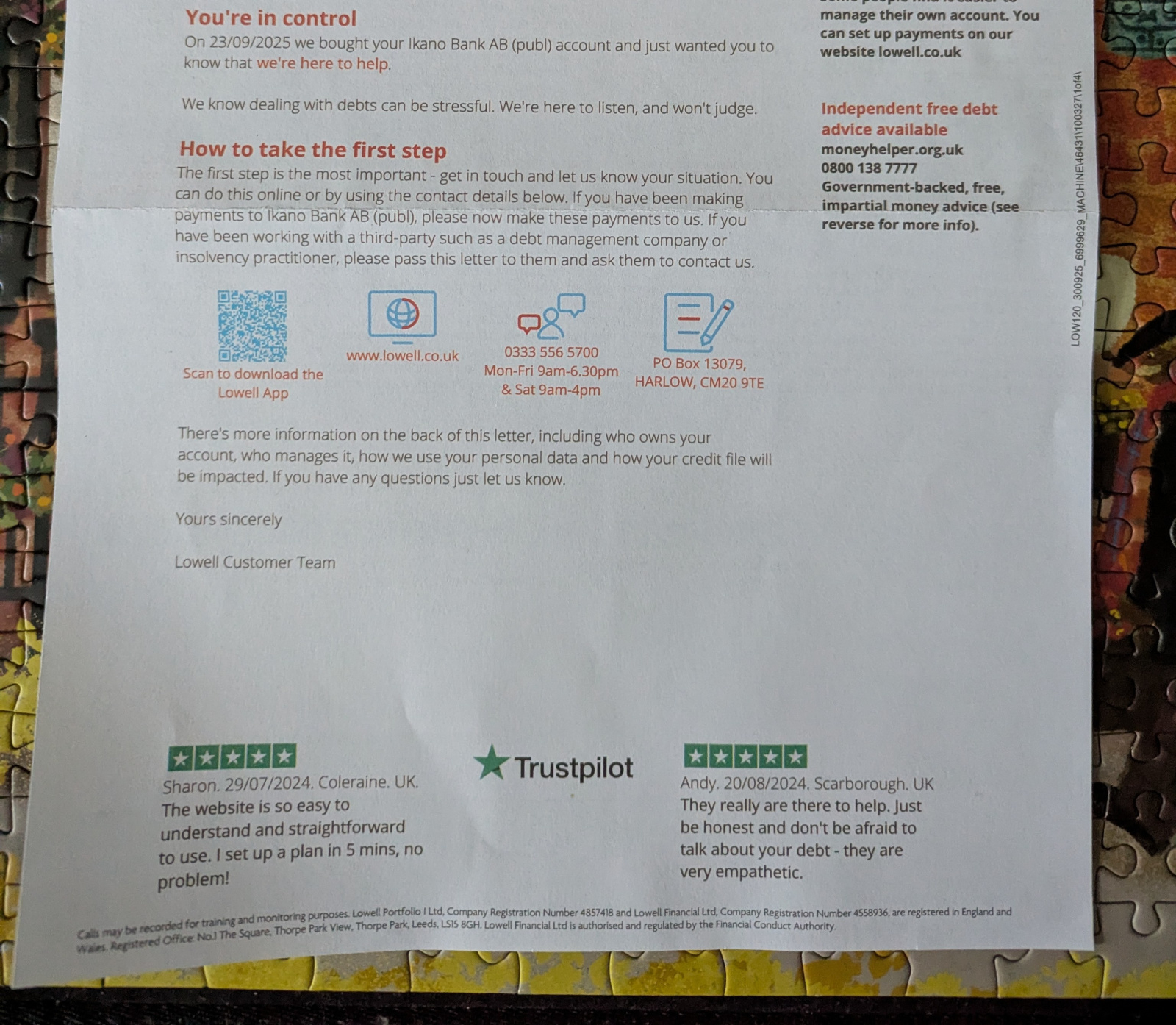

I've received the attached letter from Lowell, a debt collection/purchaser, alongside a letter from Ikano saying that Lowell have purchased my Ikano debts because they've defaulted (that letter wouldn't upload for some reason). Today my Ikano debts have also shown as defaulted on my Equifax report, as Fixed Term Credit Sale, and will also be removed from my next report (according to Clearscore). The letter was dated Sept 30th but life has been hitting us hard, and the Clearscore notification this morning prodded me to post.

- Does this letter from Lowell effectively start the default clock again? IE should I wait for the Lowell account to default now (if that's even a thing?), giving me another few months to save for a settlement figure?

- or should I offer them a settlement figure now, or just set up a standing order of what I can afford?

- is it sensible to set up an online account for them, or is that overdoing it? It'd be useful to see how much we owe etc but I've held off for now.

- I've seen mention of strategies a fair bit here, are they detailed anywhere? I know there's the pinned post but it feels like it's not step by step enough for me unfortunately, so any pointers for step by step of "when you get a letter that says x do y" would be amazing, I work great with those!

I've also started getting notice of defaults from the other lenders, so feels like they're all coming to a head now.

TIA!

0

0 -

Debts only default once, and being sold doesn't change that, so it's still defaulted even though it's with Lowell now.

I'll leave the strategy stuff to the experts.Credit card debt: £8530 £8071

Savings: £33631 -

Lowell will use the same default date that the lender did. (It's a good idea to check your credit record to see this has happened in a few months, but you dont need to wait to see this or anticipate problems here as they are pretty rare.)

You have quite a few options here and there isnt an easy way to decide which to do and in what order. Here is what I tend to think about, but some if it is personal preference:

1) ignore

I dont suggest ignoring this. At this point, it is wishful thinking to hope the debt will become statute barred, its a lot too far off. If you hadn't paid anything to it for 5 years, things would be different

2) set up a monthly payment

I think this is a good idea, but make it as low as possible. So you can accumulate an emergency fund and a post to make settlement offers from

3) make an affordability complaint to Ikano

if you win, interest is removed so the balance will reduce.

If there is a lot of interest in the balance (a loan where the balance includes all the interest for the full length of the loan, a loan where you are a long way through so have already paid a lot of interest, a credit card or catalogue where you have paid a lot of interest) then this seems a good idea if you think the loan caused you difficulties from early on.

For a debt where you have paid little or no interest, there isnt much point.

And if the debt defaulted a long time ago (5+ years) you will find it hard to prove unaffordability.

4) ask Lowell for the CCA agreement for the debt

Some people prefer not to do this now, hoping the debt will be sold on again, as each extra step in the chain makes it a bit less likely the CCA can be found, but it's my feeling this happens less than it used to.

Also, there is the possibility that the right to ask for the CCA may be removed or really watered down sometime in the next few years, so in general I prefer asking sooner rather than later.

If the account was opened a long time ago, the CCA is less likely to be found. I would ask straightaway for any card opened pre 2007 or any catalogue opened pre 2015

5) make a settlement offer

I would prefer to settle down and make low payments for a while and then ask for the CCA before making a settlement offer. Of course, if Lowell offers you an offer, you can counter with a lower one.

So a strategy could look like - set up low monthly payments, make an affordability complaint, if that is rejected at the Ombudsman ask for the CCA.0 -

You've not shared your SOA, so it's hard to comment in detail.

Regarding that letter, the important bit is probably immediate above the partially visible para on the right hand side at the top of the letter, referring you to their web-site. What does that say?

Beyond that, how much have you saved into your emergency fund, as a multiple of the essential spends in your monthly budget?

Have you encountered any spends that aren't in your SOA, like Christmas, visiting family, house repairs, clothes, holiday. If so, you need to divide that cost by 12 and add it to your monthly budget. Save that money into an instant access ISA.

And another for the emergency fund.

How much do you now owe and how much can you afford monthly with your revised SOA?If you've have not made a mistake, you've made nothing1 -

Sorry it's taken so long to do an SOA, it's been a pain to get my head around it with everything going on but I think I'm there. I did one in Stepchange a few months back when this all kicked off which reckoned I'd have about £210 leftover a month to spend, but just to try and get this done and posted I've taken a stab on a few things and using that as my figure and planning to just live it for a bit to see if it works, otherwise the inertia is just stopping me from doing anything.My finance spreadsheet makes more sense to me than this but leaves us with about £80 per pay (I get paid every 4 weeks), as does this roughly, but that has me a bit worried that we don't have much left for anything that might just "come up". I'll probably end up with a surplus every now and again which I can stick in our emergency fund because of the way bill dates fall too. Hope the formatting is OK, I can't fix the tags![font=courier new][b]Statement of Affairs and Personal Balance Sheet[/b][b]

Household Information[/b]

Number of adults in household........... 2

Number of children in household......... 2

Number of cars owned.................... 1[b]

Monthly Income Details[/b]

Monthly income after tax................ 3720.46

Partners monthly income after tax....... 0

Benefits ............................... 104.2 (should have additional 69 in Jan from new claim for second child)

Other income............................ 0[b]

Total monthly income.................... 3824.66[/b][b]

Monthly Expense Details[/b]

Mortgage................................ 740.1

Secured/HP loan repayments.............. 0

Rent.................................... 0

Management charge (leasehold property).. 0

Council tax............................. 216

Electricity............................. 255 (dual fuel, expires May - £75 exit fee per fuel)

Gas..................................... 0

Oil..................................... 0

Water rates............................. 67

Telephone (land line)................... 0

Mobile phone............................ 36 (two phones, paying off device plans, moving one from O2 to Lebara tonight!)

TV Licence.............................. 15

Satellite/Cable TV...................... 0

Internet Services....................... 27.95

Groceries etc. ......................... 850

Clothing ............................... 60 (trying to build up our fund rather than buying as we need)

Petrol/diesel........................... 140 (mostly WFH, this budget has worked well for the last few months)

Road tax................................ 17.06

Car Insurance........................... 34.92

Car maintenance (including MOT)......... 72.73 (trying to save about £800 a year so I don't get stung on this again like a couple of years ago, due Sept)

Car parking............................. 0 (factoring this in to holiday)

Other travel............................ 0

Childcare/nursery....................... 45

Other child related expenses............ 100

Medical (prescriptions, dentist etc).... 204 (we have NHS prepayments, but also have private therapy which bumps this up. Not covered through work sadly.)

Pet insurance/vet bills................. 107.6 (60p/m on insurance, might go down on vet bills but not sure yet and just had to pay £800 out for one cat prior to getting insurance with another cat needing it)

Buildings insurance..................... 30.89

Contents insurance...................... 0 (included in buildings)

Life assurance ......................... 18.56

Other insurance......................... 0

Presents (birthday, christmas etc)...... 150

Haircuts................................ 22.5

Entertainment........................... 100

Holiday/days out........................ 60

Emergency fund.......................... 100

Household subs (Snoop, Ring etc)......... 12.5

Streaming services...................... 57[b]

Total monthly expenses.................. 3531.81[/b]

[b]

Assets[/b]

Cash.................................... 2782.72 (we got a backdated child benefit payment of nearly 2k, but need to pay out about 1.5k on house repair, car and potentially vet)

House value (Gross)..................... 320000

Shares and bonds........................ 0

Car(s).................................. 5000

Other assets............................ 0[b]

Total Assets............................ 327782.72[/b]

[b]

Secured & HP Debts[/b]

Description....................Debt......Monthly...APR

Mortgage...................... 169012...(740.1)....3.56[b]

Total secured & HP debts...... 169012....-.........- [/b]

[b]Unsecured Debts[/b]

Description....................Debt......Monthly...APR

MBNA...........................8087.27...34.25.....0

Barclaycard....................10859.....42.23.....0

Halifax........................11334.....44.08.....0

First Direct Overdraf..........520.6.....2.02......0

Ikano 2........................1733......6.74......0

Ikano 1........................604.......2.35......0

Virgin.........................10569.....41.1......0

First Direct Gold..............7252.81...28.21.....0

HSBC...........................2318.01...9.01......0[b]

0 -

RAS said:You've not shared your SOA, so it's hard to comment in detail.

Regarding that letter, the important bit is probably immediate above the partially visible para on the right hand side at the top of the letter, referring you to their web-site. What does that say?That was just account details, and payment methods that I cropped off for private info.

Beyond that, how much have you saved into your emergency fund, as a multiple of the essential spends in your monthly budget?See my SOA, but now 2782. We've not done well at budgeting and I've struggled to get my head around it but over the last couple of months I've started enveloping more.

Have you encountered any spends that aren't in your SOA, like Christmas, visiting family, house repairs, clothes, holiday. If so, you need to divide that cost by 12 and add it to your monthly budget. Save that money into an instant access ISA.

And another for the emergency fund.

How much do you now owe and how much can you afford monthly with your revised SOA?£53,998.71 owed, still looking at about £210 to pay back. It's about 20 years which is crazy for a DMP but this is what Step Change suggested on their online tool too, but I don't see what other choice I've got as an IVA is too scary and bankruptcy just doesn't seem an option.

Sorry forgot to reply to these!

0 -

A quick thought £850 on groceries why?If you go down to the woods today you better not go alone.0

-

In your opening post you mentioned your 3 year old will be starting nursery, is this with the free hours, or will you have costs associated with this?

Can you wife work and start making a financial contribution to the household?I’m a Forum Ambassador and I support the Forum Team on the Pension, Debt Free Wanabee, and Over 50 Money Saving boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the Report button, or by e-mailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.0 -

Thanks for the input.

£850 groceries - looking back this is how much I set aside in my Groceries space/envelope each cycle, but more accurately we spend about 680 on average on groceries. I'm not sure if that in itself is high, but 3/4s of us have limited diets as we're autistic so have to eat specific things like brands (and there's probably not that many brands we buy, but only a handful of meals we actually eat as a family), so can't just go to Lidl without driving 10 mins to a main supermarket to get other stuff too, so we get a food shop delivery because I can't deal with going walking and driving around a supermarket for 90 minutes, and neurodiversity is a huge challenge to what we face financially. That also contributes to needing to get takeaways too which takes it up to the 850, things like fish and chips/pizza/McDonald's etc because that's all sometimes some of us can feel like we can eat and can't push ourselves to eat something else we've meal planned or cook something else - normally due to overwhelm with 2 ND kids in the house too, combined with our ADHD too. At least we're getting food in us at that point, even though we know it's bad for us/the planet (mcds)/our bank account. It's such a vicious cycle and how we got in this wider financial mess in the first place, but at least that type of stuff isn't going on a credit card now and we have cut back because of the situation we're in. A ramble, but basically the biggest contributor to credit companies taking advantage of people like us. Ok ramble over 😅Grumpelstiltskin said:A quick thought £850 on groceries why?Smudgeismydog said:In your opening post you mentioned your 3 year old will be starting nursery, is this with the free hours, or will you have costs associated with this?

Can you wife work and start making a financial contribution to the household?

Childcare costs - we use the 15 free hours. We're not eligible for more free right now but don't pay for more as she's only in 2 days a week. We actually just got child benefit for her, I'm taxed on roughly half of it due to my income (HICBC) but either way some more that can go towards paying off debt.

Wife working - no. Not sure how much detail you need as a response to any of this but feel like I need to share our thought process! As I mentioned, she's AuDHD and the prospect of going back to work with all the added stress that would bring on our family (adding to things that I haven't listed here), for the little amount of money she'd bring in at min wage, would be too much. She used to work 16hrs in a shop til COVID furlough, and then realised when she wasn't working the toll it was actually taking on her. She's also primary carer for our daughter for 3 days a week when not in nursery in school hours, which would be the case til July til school full time. Then we'd need to juggle our time off to watch the kids over summer/other term times which doesn't add up, and we wouldn't share much time off together either in that scenario.We really need to start claiming disability allowance for my son that'll help towards our overall situation and increased costs of his needs, but a 40 page form is ADHD kryptonite 😔 it takes me long enough to get around to replying to you helpful people!0 -

You will need help to complete the PIP forms, do you have a CAB near you?If you go down to the woods today you better not go alone.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards