We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

5.375% Treasury Gilt 2056

Comments

-

Quite correct. But one aspect of an annuity which bears comparison with the gilt is level vs increasing. Would you buy a level annuity or an increasing one. It is not an obvious answer but most would go with an increasing one because inflation will make a level annuity worth less as time goes by. This gilt will be paying the same coupon in 2056 as in 2026 but as others have pointed out that coupon will be worth a lot less by then. Index Linked gilts may be the answer to that but they seem more complicated (to me) and usually have much lower coupons than this one.k6chris said:QrizB said:You'll need to balance the likely value of your capital in 2056 vs. the increased income from an annuity. Per a recent thread, even a 55-yo would get a higher income from a level annuity than the gilt is paying.

Agree, but the gilt route allows you to revert back to capital (with risk of fluctation based on underlying bond rates) vs an annuity which is a one-way decision. I think that is correct??1 -

For those wanting a component of fixed/guaranteed income in retirement there are broadly three tools available

1) A single gilt (as in this thread) which has the benefit of providing a known nominal or real income, being simple to set up and operate, and returns the principal (in real or nominal terms), but has the disadvantages that the level of income may be relatively small (e.g., the highest coupon for a longish term inflation linked gilt is 1.875% for TR49).

2) A collapsing gilt ladder (whether nominal or inflation protected) which has the advantages that the income may be tailored exactly to that required, the income level is higher than a single gilt (e.g., for a nominal 30 year ladder, a payout rate of about 6.5% is currently available, see https://lategenxer.streamlit.app/Gilt_Ladder and about 4.3% for a 30-year RPI ladder) and that there is some legacy provided death occurs before the end of the ladder. The disadvantages are that initial complexity is relatively high (although simple enough once in operation), the retiree may outlive the income stream, and the income can be 'lumpy' (a mix of coupons and maturing bonds).

3) An annuity (whether nominal or inflation protected) which has the advantages that the payout rate will probably be highest out of the three tools although this depends on survivor benefits (e.g., a single life annuity at 65 is currently has a payout rate of 7.9%, but is 7.2% for a joint life with 50% survivor benefits), income will last a lifetime, and is simple in operation (others will have to comment on the complexity of purchase). The disadvantage is a lack of short-term legacy (although a 20 year or so guarantee period will help with this at the expense of reducing the payout rate - effectively, a guarantee period is equivalent to a ladder). For joint life with 100% survivor benefits, a long guarantee has a smaller effect on payout rate than for a single life, as a play with the moneyhelper annuity tool at https://www.moneyhelper.org.uk/en/pensions-and-retirement/taking-your-pension/compare-annuities demonstrates).

In each case, nominal income will be larger initially but has the potential for being eroded by inflation, while inflation-protected income is smaller at the start, but will not be eroded with time.

There is no reason why the options cannot be combined.

9 -

Is this issue on the secondary market yet?

I can't find it0 -

HL say the allocations are being announced today so may appear tomorrow.1

-

Why not just invest in Ultra short duration bond fund such as ERNS and reap 5.3% dividend that it's currently paying?? Then if performance drops bail out of that fund and choose something else?

https://www.hl.co.uk/shares/shares-search-results/i/ishares-gbp-ultrashort-bond-ucits-etf-gbp?msockid=1b221165b57a6ad923c30410b4006b9d

Why this complexity of buying this Gilt directly? Am I missing something???0 -

Well tne gilt locks in 5.3% for 31 years. Rates could go lower again but I doubt we will see 1% base rates again.MetaPhysical said:Why not just invest in Ultra short duration bond fund such as ERNS and reap 5.3% dividend that it's currently paying?? Then if performance drops bail out of that fund and choose something else?

https://www.hl.co.uk/shares/shares-search-results/i/ishares-gbp-ultrashort-bond-ucits-etf-gbp?msockid=1b221165b57a6ad923c30410b4006b9d

Why this complexity of buying this Gilt directly? Am I missing something???0 -

ERNS currently has a yield to maturity (see https://www.morningstar.co.uk/uk/etf/snapshot/snapshot.aspx?id=0P0000ZRP7&tab=3&InvestmentType=FE) of 4.79%, so pretty good. Whether it will do better than the gilt over 31 years is unknown. If ultra short interest rates (i.e. less than 1 year) spend the next 30 years higher than 5.3% then buying the gilt will have been a bad decision, if ultra short interest rates spend the next 30 years lower than 5.3% then buying the gilt will have been a good decision. The point is that the gilt will provide certainty in income whereas the fund will not. Whether that is important is a different question!MetaPhysical said:Why not just invest in Ultra short duration bond fund such as ERNS and reap 5.3% dividend that it's currently paying?? Then if performance drops bail out of that fund and choose something else?

https://www.hl.co.uk/shares/shares-search-results/i/ishares-gbp-ultrashort-bond-ucits-etf-gbp?msockid=1b221165b57a6ad923c30410b4006b9d

Why this complexity of buying this Gilt directly? Am I missing something???

I note that, at least with an iweb ISA buying individual gilts on the secondary market is as simple as buying a fund.

1 -

Just checked trading on T56, got a quote of 97.9p on HL to buy.FIREDreamer said:DRS1 said:

Might be priced close to £1 par given current gross redemption yields on 30 year gilts.Stupid question but what will it cost?

Can you get £1 nominal for £1?

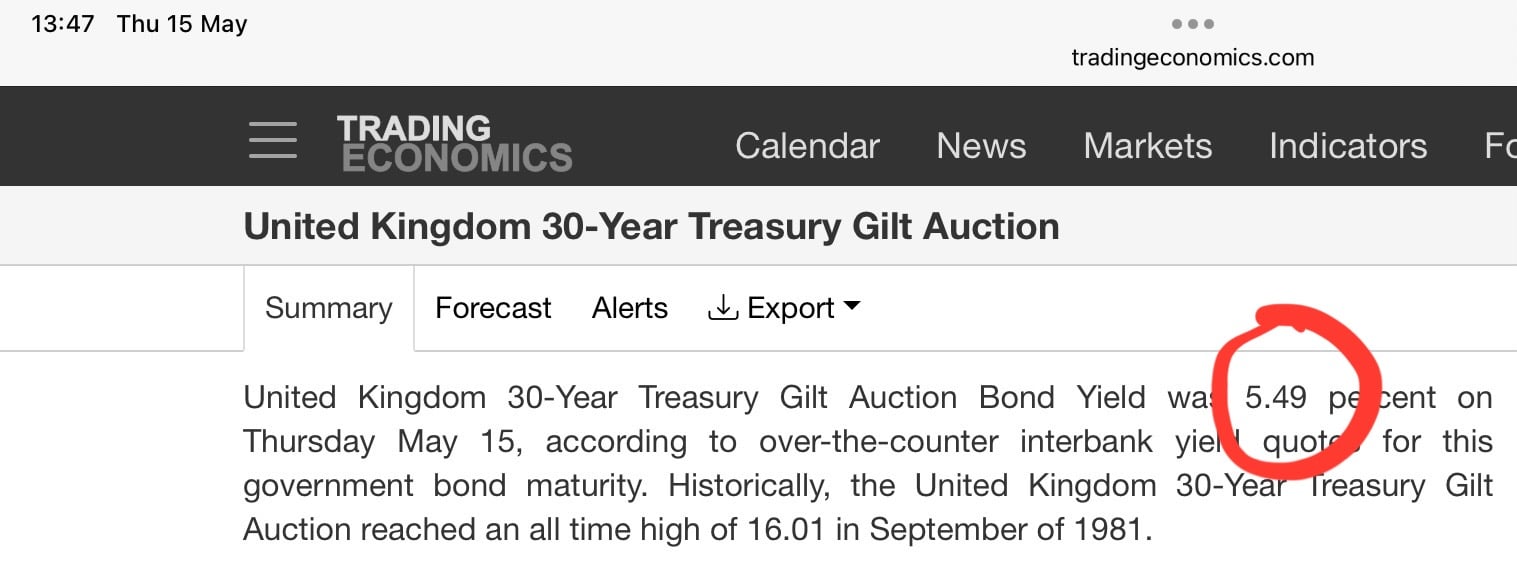

Interested to know if anyone who may have subscribed at the auction did a little better. Yield pretty much spot on the 5.49% quoted above.

0 -

poseidon1 said:

Just checked trading on T56, got a quote of 97.9p on HL to buy.FIREDreamer said:DRS1 said:

Might be priced close to £1 par given current gross redemption yields on 30 year gilts.Stupid question but what will it cost?

Can you get £1 nominal for £1?

Interested to know if anyone who may have subscribed at the auction did a little better. Yield pretty much spot on the 5.49% quoted above.You can see the result of the syndication process (nb: not auction - not that the difference matters much to retail investors) at https://www.dmo.gov.uk/data/datareport?reportCode=D10AThe launch price was 99.57 with an issue yield of 5.4047%1 -

I did wonder if the market would mark it down further. However, since the earlier quote this morning discount has tightened appreciably and HL now quoting 99.94p.phlebas192 said:poseidon1 said:

Just checked trading on T56, got a quote of 97.9p on HL to buy.FIREDreamer said:DRS1 said:

Might be priced close to £1 par given current gross redemption yields on 30 year gilts.Stupid question but what will it cost?

Can you get £1 nominal for £1?

Interested to know if anyone who may have subscribed at the auction did a little better. Yield pretty much spot on the 5.49% quoted above.You can see the result of the syndication process (nb: not auction - not that the difference matters much to retail investors) at https://www.dmo.gov.uk/data/datareport?reportCode=D10AThe launch price was 99.57 with an issue yield of 5.4047%0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.7K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.5K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards