We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Take DB pension early or not as part of 'bridging the gap'? (inheritance vs longevity risk)

Comments

-

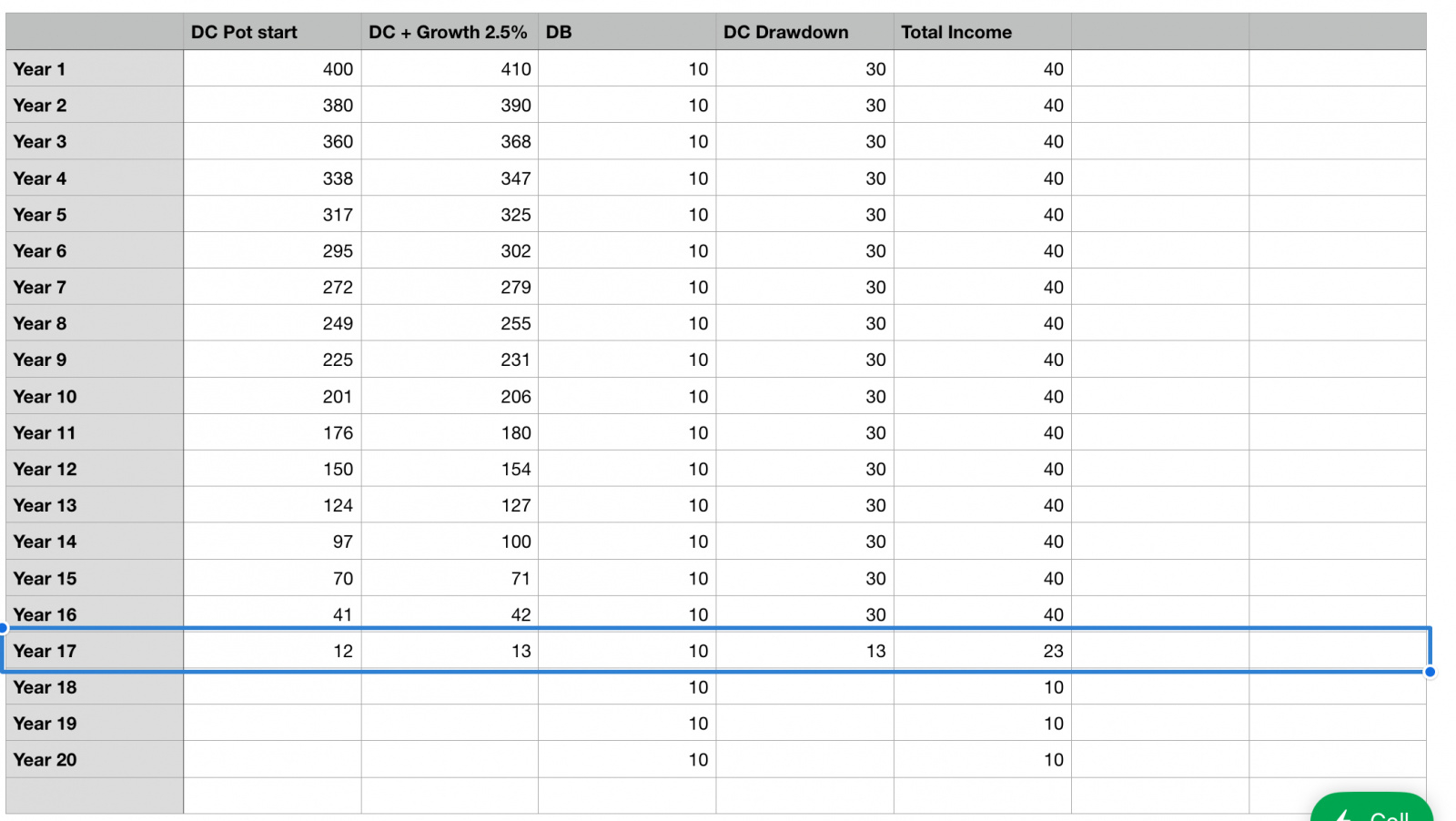

Which is why is said "Depends on your DC fund choices/strategy, how much you are planning to take from your DC and how much relative DB to DC you have." Each person's circumstances will be different.michaels said:I'm happy that the actuarial reduction is fair for expected life span. But where DB can win is if you are one of those who live longer than the average expectation - hence the normal advice to backload DB.

However if you then hit the other end of the longevity distribution then putting the DB off will mean you have spent more of the potentially inheritable resource (DC) whereas the DB dies with you (or on the second death anyway) so have less to pass on.

Personally I don't buy the 'more time for DC growth' argument above - whilst on average DC will grow faster than inflation, what matters to safe retirement income is the reasonable worst case path not the average path.0 -

A simplistic example. Let's assume a requirement for £40k a year, a DC pot of £400k and a reduced DB of £10k starting at 57. With annual growth of 2.5% on the DC pot. The DC pot is exhausted at year 17:michaels said:

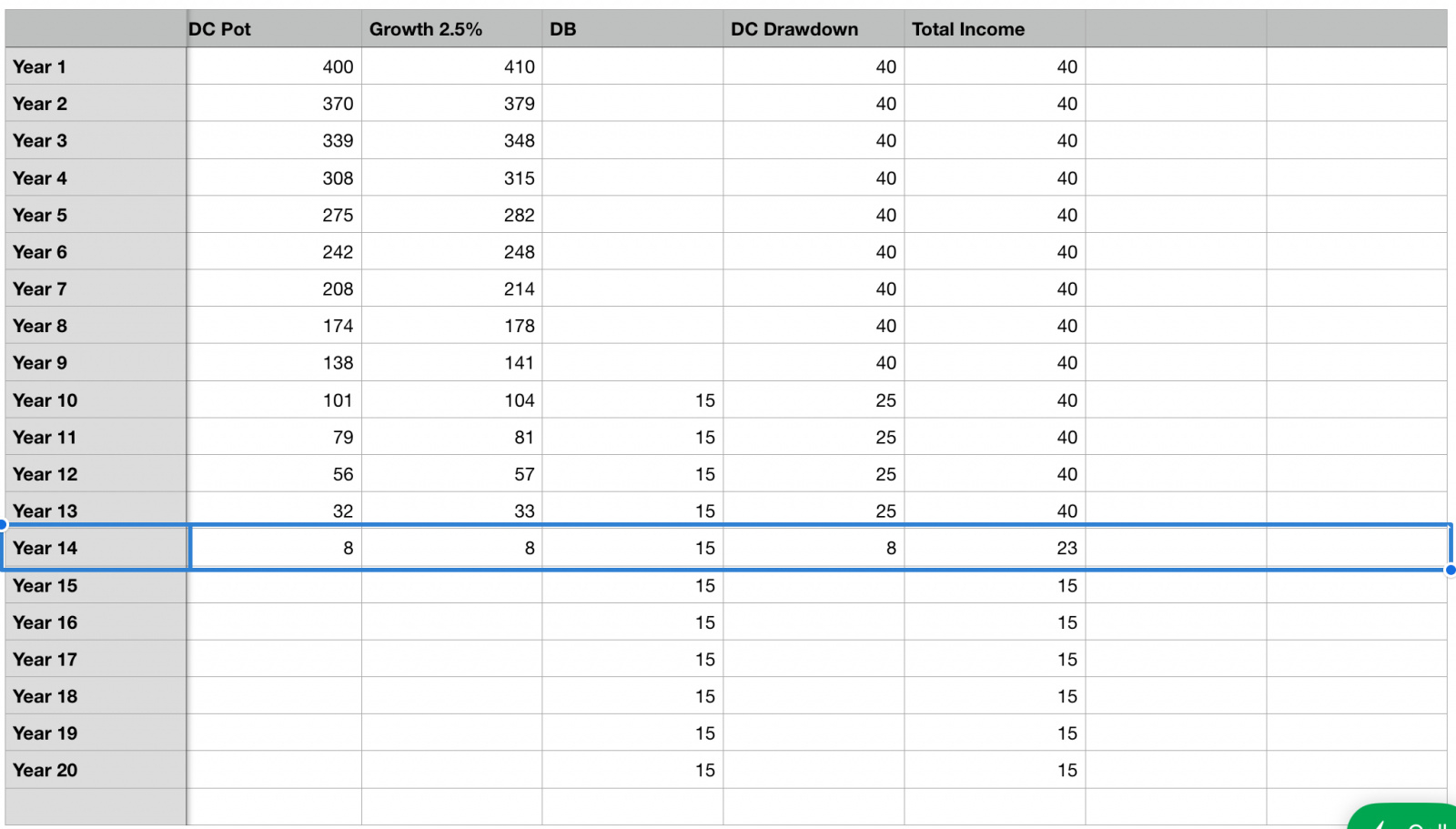

Personally I don't buy the 'more time for DC growth' argument above - whilst on average DC will grow faster than inflation, what matters to safe retirement income is the reasonable worst case path not the average path. Now the same £40k a year, a DC pot of £400k and an unreduced DB of £15k starting at 67. With the same annual growth of 2.5% on the DC pot. The DC pot is now exhausted at year 14:

Now the same £40k a year, a DC pot of £400k and an unreduced DB of £15k starting at 67. With the same annual growth of 2.5% on the DC pot. The DC pot is now exhausted at year 14: The difference in the DC balance at year 10 is quite marked - £100k. The flip side in the 2nd example is that you have £15k DB guaranteed from year 10 onwards but then don't forget SP will also kick in so assuming a full SP then you are talking £22k vs £27k guaranteed income from that point onwards. If you are a couple both entitled to full SP then your guaranteed minimum is obviously higher.My own attitude is that as a couple we will need less money as we get older so the difference in the DB isn't as big an issue as it might seem on paper. The combination of DB (reduced) and 2* SP will provide our minimum requirement at age 67.It's just an example to show the difference in approaches, actual growth would differ year on year, some years could be bigger, some years could be negative. If you are taking less from the DC pot year on year then the potential for growth remains longer.0

The difference in the DC balance at year 10 is quite marked - £100k. The flip side in the 2nd example is that you have £15k DB guaranteed from year 10 onwards but then don't forget SP will also kick in so assuming a full SP then you are talking £22k vs £27k guaranteed income from that point onwards. If you are a couple both entitled to full SP then your guaranteed minimum is obviously higher.My own attitude is that as a couple we will need less money as we get older so the difference in the DB isn't as big an issue as it might seem on paper. The combination of DB (reduced) and 2* SP will provide our minimum requirement at age 67.It's just an example to show the difference in approaches, actual growth would differ year on year, some years could be bigger, some years could be negative. If you are taking less from the DC pot year on year then the potential for growth remains longer.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards