We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Aviva pension query

cdbe11

Posts: 59 Forumite

We recently (last week) opened 2 Aviva sipp type pensions (to cut a long story short - I'm a non earner so put in £2,880 for the tax relief, wife put £6k in to avoid higher rate tax and losing child benefit). New to all this but I believe it's a good idea.

So now have we lost all our money??

It appears not - wife is in this and has lost as of today £119.

My £3,600 appears to still be in "cash" and I've received £2 interest.

It was a mad rush to open these before the end of the tax year (after being let down by standard life) so I presume I didn't choose a fund at the time.

Two questions - should we just leave wife's money where it is or is there something safer till the markets settle

and, should I be putting my cash into a fund (probably the same safe (if it is) option) and now or wait a bit?

Thanks

So now have we lost all our money??

It appears not - wife is in this and has lost as of today £119.

Aviva Insured Funds Universal 2027 Retirement S14

My £3,600 appears to still be in "cash" and I've received £2 interest.

It was a mad rush to open these before the end of the tax year (after being let down by standard life) so I presume I didn't choose a fund at the time.

Two questions - should we just leave wife's money where it is or is there something safer till the markets settle

and, should I be putting my cash into a fund (probably the same safe (if it is) option) and now or wait a bit?

Thanks

0

Comments

-

Non earner? Take £3602 out, use a bit of the personal allowance, pop £2880 back in grossed up to £3600, £720 to you and you've got £3600 back in your SIPP. I think.0

-

That fund has over 40% in bonds so its not exactly high risk. Probably won't shoot up as much if there is a recovery.

What is the significance of 2027?0 -

That may be a valid option but I suspect the op may not be aufait with the potential MPAA issue when taking that option. Or what could be done to mitigate it.kempiejon said:Non earner? Take £3602 out, use a bit of the personal allowance, pop £2880 back in grossed up to £3600, £720 to you and you've got £3600 back in your SIPP. I think.

And although they are a "non earner" we have no idea what taxable income they do have. Other than it is presumably less than the wife's.

From the op it is possible that Marriage Allowance could be a factor here as well although it's not immediately clear how a £6k (or £7.5k) contribution achieves the dual benefits of avoiding higher rate tax and Child Benefit 🤔. Unless it's avoiding some higher rate tax?0 -

Assuming OP is at least 55...kempiejon said:Non earner? Take £3602 out, use a bit of the personal allowance, pop £2880 back in grossed up to £3600, £720 to you and you've got £3600 back in your SIPP. I think.Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0 -

Op is 55 in May (from another thread).Marcon said:

You're assuming OP is at least 55...no indication in the post of age that I can see.kempiejon said:Non earner? Take £3602 out, use a bit of the personal allowance, pop £2880 back in grossed up to £3600, £720 to you and you've got £3600 back in your SIPP. I think.0 -

Thanks all. Just to clarify - yes I'm 55 next month so understand I can withdraw 25% tax free and repeat annually. I have income from rentals (about 18k net) and nothing else, I have a deferred CS pension of £14k at 60. I'm really hoping I can sell them in the next few years so can draw down the remaining bit of SIPP pension if I have a period of no income for my allowance.

My wife (TPS scheme) paid 6k in higher rate tax - hence the pension - last year she crept into higher rate - we had to repay child benefit and she'd had the marriage tax allowance from me (we transferred it years ago when my income was very low) so we owed tax because of this. She will retire at 55 ish (3 years) so may drawdown her SIPP (assuming it's then worth around (3x 6k contributions) 20K) and defer her TPS for a year to reduce the AR.

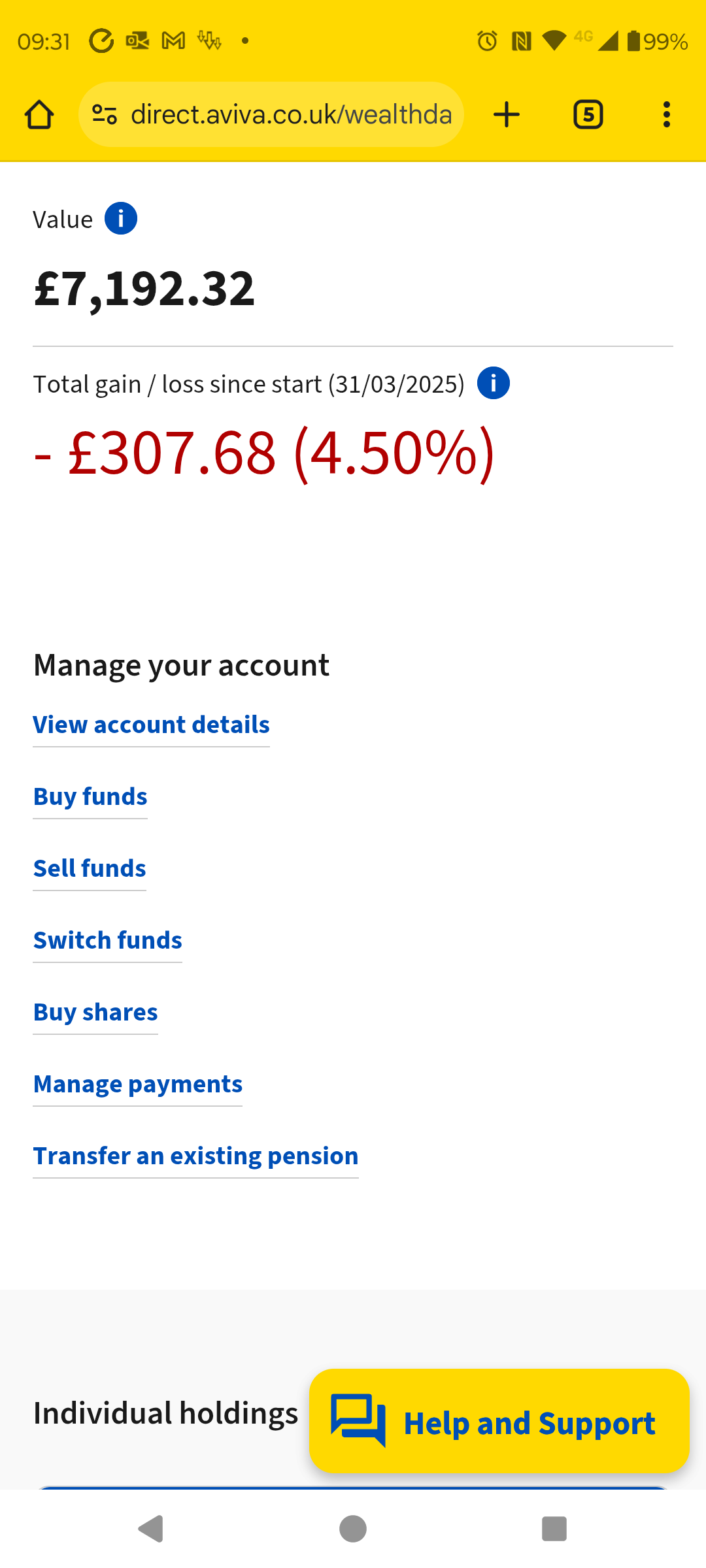

Today's news. (Obviously laughable to those who've genuinely lost lots of money).

0 -

I bet tomorrow it will look even better.0

-

So now have we lost all our money??

The markets went down about 15% ( now less) so why would you think you could have lost all your money ?

In fact as less than half of your wife's investment is actually invested in the stock market, then any impact is diluted anyway.

As your money was still in cash you have not lost anything.0 -

Thanks all. Just to clarify - yes I'm 55 next month so understand I can withdraw 25% tax free and repeat annually.If you draw the 25% up front then you cannot repeat that every year. Only if you do not draw it up front will have you some available in future years.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.9K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards