We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

NI contributions for early retiree

Comments

-

NI creditsAre you sure that you have not already reached the maximum?

What exactly is shown on your state pension forecast?

https://www.gov.uk/check-state-pension

0 -

If you already meet the requirements for the full state pension you don't need further NI, if you so you'll only get NI credits by claiming a welfare benefit."You've been reading SOS when it's just your clock reading 5:05 "1

-

Following up on this question, I have a similar one . . . .

I retired in 2017, my last year was as a self employed sole trader (I paid Class 2 NICs on those earnings). At that point I had 41 years of full NIC contributions. I then started taking money from my DC pension scheme.

The HMRC website tells me that subsequent years, are "not full", i.e., I need to make contributions for the "missing" years to get the full state pension.

Is this true? I had no employment earnings in those years, only Pension, am I not exempt from future NIC contributions and entitled to the full state pension after contributing for the 41 years?

Should I have told HMRC that I had retired?

0 -

Maybe you could tell us how much State Pension you have already accrued (read the whole of your forecast to find that out).

1 -

Are you mixing up your NI record, which is a record of fact about your contributions, with your state pension forecast ?

What precisely does your pension forecast state with reference to what you have already accrued and what you need to do further ?

It will clearly state both of those points with no room for confusion.

41 years is of no relevance to someone with a pre 2016 record.

0 -

I don't think being a pensioner exempts you from NICs. You do not pay NICs on pensions though.

And NICs normally don't apply once you hit state pension age.

If you are below state pension age, have no employment income, no self employed earnings and only a pension then you won't pay any NICs. That means your tax year will show as Not Full.

One way to fill a year without paying NICs is to qualify for NIC credits (eg sign on for unemployment benefit or whatever they call it these days or look after your grandkids).

If you don't qualify for credits then you can pay voluntary NICs which is what you are being told you can do by the sound of it.

If you don't pay the voluntary NICs then your year will remain Not Full. That may or may not impact on your state pension. As has been mentioned already you can check your state pension forecast to see if you are at the max already or if you need to fill more years and if so how many. You can also see the years available to be filled and their costs. Be warned the costs will probably go up in April. And be aware that not all the years since 2017 will be available to be filled now even though they may show as Not Full. You may have missed the boat for anything pre 2019.

0 -

Hi Guys

thanks for taking the time to reply

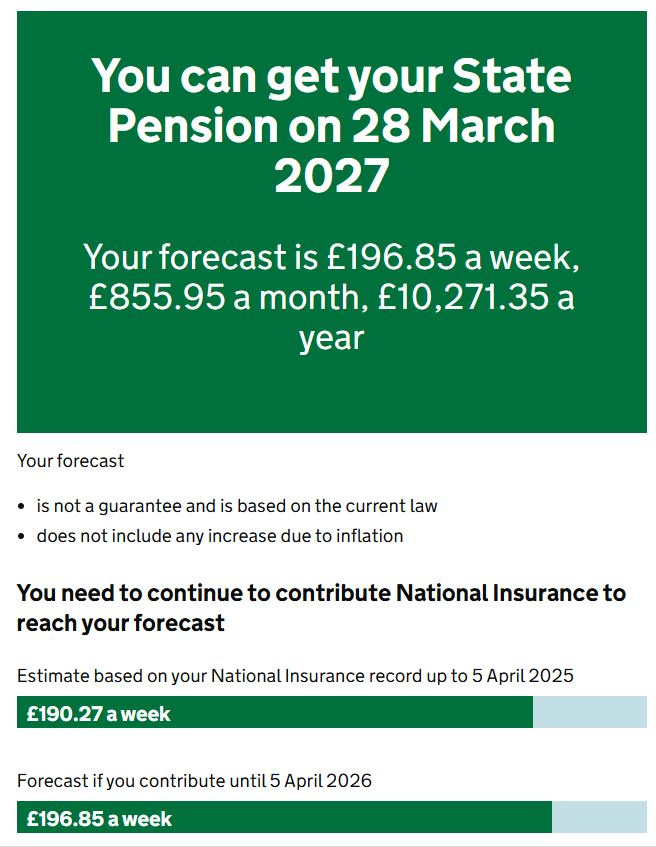

OK, dumps from HMRC Pension forecast attached

To get to the forecast of £196.85 p/w, it's telling me that I need to contribute until 5th April 26, otherwise, I only get £190.27. That means that I am expected to contribute with no salary earnings, only pension. Is that how it works? I thought that Nics weren't due on pension only earnings?

Similarly, the "gaps" in my record are due to the period after I retired and now, so it seems that I won't get a full pension without contributing after I retired?

0 -

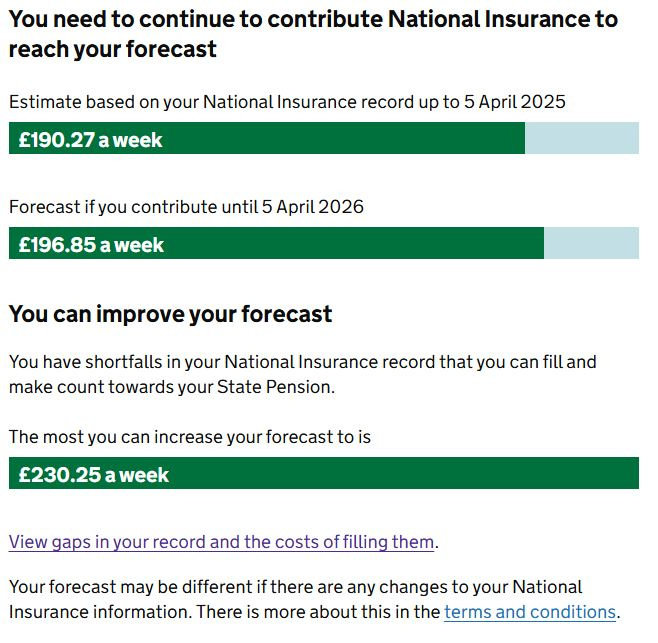

NI contributions are only due on earned income but without contributing you cannot get the benefit, that is where voluntary contributions come in. To increase your pension you then need to make up 6 years to get close to the full pension - the 7th will only add 51p. You currently have 7 available, 19-20 to 25-26. The earliest, 19-20, ceases to be available from April 6th and all years 23-24 and earlier will increase from the price shown in your NI record to £956.80. Any contributions you make will be returned gross in around 140 weeks once your pension comes into payment, an absolute bargain the same as at least a 37.5% single life increasing annuity - where else could you buy that.

Also further down the forecast there will be a statement about contracting out - to be in this situation, needing more than 35 years, you will have been.

2 -

You seem to be a winner under the new system, presumably having paid lower NI for many years when contracting out but now with the chance to reach the standard new State Pension 👍

But you don't need to do anything and don't need to pay NI when retired if you would prefer not to. No NI is payable on pension income and nothing needs to be paid if you have no earnings.

But you can voluntarily pay NI to increase your State Pension, that is entirely your personal choice.

Buying six years will take you to £229.74/week, an extra one will only add the final £0.51/week. At current rates those six years are adding just over £2k (before tax) to your State Pension.

So likely to be a no brainer from a financial perspective, especially considering the triple lock protection (currently) in place. The seventh year isn't such a great deal and isn't really a good option at Class 3 rates.

2 -

Thanks a lot for the replies, I think that I get it now.

So, it seems that there isn't a maximum number of years that you need to contribute to get a full pension, you have to contribute every year until state retirement age, working or not?

I can see the benefit of buying extra years, as good a deal as it seems, it's not necessarily as good as at first sight though. The money used to buy the additional years will come out of earned income and the added benefits will be taxed at your marginal rate, so those conditions need to be factored in, but it still seems like a good deal - assuming that I live long enough to reap the benefit :-)

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards