We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Debt help

Anon_09

Posts: 14 Forumite

Hi all,

Really struggling mentally and feel like I’m in a hole that just seems to be getting deeper and darker. Need some advice on how to proceed and get life back on track.

Stupidly through my own fault I have racked up around £45-£50k debts through unsecured loans and credit cards.

Really struggling mentally and feel like I’m in a hole that just seems to be getting deeper and darker. Need some advice on how to proceed and get life back on track.

Stupidly through my own fault I have racked up around £45-£50k debts through unsecured loans and credit cards.

One issue that has caused this is I had 2 seperate credit files for ClearScore and Experian. One had my old address and the other, my new address. This somehow allowed me to borrow more debt than realistically I should have been able to, which at the time was needed but it’s now put me in a position where I just cannot survive financially due to the outgoings this has brought on. It’s frustrating really as I feel it’s 50/50 as the lender shouldn’t have let me borrow across 2 different files due to the different address. However I understand it’s my fault for taking on the responsibility of this debt.

I am unsure what to do, whether I go down the route of step change or something similar?

I have a mortgage on a property with about £90k equity. My deal is due to finish on our fixed rate in October 2025.

We really want to upsize our house due to now having a bigger family but I am completely unsure on how best to proceed.

If I go through step change now is that going to affect my remortgage options with my same lender (nationwide)?

Am I ever going to be able to get a bigger property and move?

Thank you for reading, I appreciate any support.

I have a mortgage on a property with about £90k equity. My deal is due to finish on our fixed rate in October 2025.

We really want to upsize our house due to now having a bigger family but I am completely unsure on how best to proceed.

If I go through step change now is that going to affect my remortgage options with my same lender (nationwide)?

Am I ever going to be able to get a bigger property and move?

Thank you for reading, I appreciate any support.

0

Comments

-

Hi anon, I didn’t want to read and run. I don’t have any specific advise but others will follow who can definitely help. It’d be used to start getting details of your debts, income and outgoings together.Debt is a problem that can be solved.You’ve made a start by asking for help.There’s light at the end of the tunnel.All the bestMFW 2021 #76 £5,145

MFW 2022 #27 £5,300

MFW 2023 #27 £2,000

MFW 2024 #27 £6,055

MFW 2025 #27 £5,075

MFW 2026 #27 0/£10001 -

You might need to get advice on your existing mortgage capability, due to your high debt?

With respect to your existing house, you will be able to choose the best fix offered by your current provider without a credit check.If you've have not made a mistake, you've made nothing1 -

With that much debt, you are unlikely to pass the affordability tests for a higher mortgage.

But you should still be able to get a new fix, called a product transfer, from your existing lender (who is it?) without affordability/credit checks. Do you will be able to get a DMP for all your debts.

I suggest you update both CRAs so they both have the current and previous address. This neat trick has actually ended you up in a big mess,0 -

It’s Nationwide I am with.ManyWays said:With that much debt, you are unlikely to pass the affordability tests for a higher mortgage.

But you should still be able to get a new fix, called a product transfer, from your existing lender (who is it?) without affordability/credit checks. Do you will be able to get a DMP for all your debts.

I suggest you update both CRAs so they both have the current and previous address. This net trick has actually ended you up in a big mess,

So with my partners very good credit score and my fairly decent income does this still mean we’re screwed and never going to be able to get a bigger property?

Thanks everyone for the replies.

Is it best I go down the route of the DMP with StepChange?

thanks0 -

There is alwaya a solution for debt but it takes time. You will only get a bigger mortgage when the lender is confident that you can afford it, and it sounds like you are quite a long way from being able to at the the moment. Remortgaging with your current lender should always be possible as thst doesn't require a credit check. Its probably best if you post a statement of affairs so people can advise in detail.

Dont lose hope, there is alwaya a way out. I got into £45k of credit card debt and started a DMP in 2021, I'm now really on top of it and have got it down to £1800 and in a few years time I'll have a clean credit record and be able to get a bigger mortgage should I wish to. I have four defaults and was able to get a new fixed rate with Santander with no problems at all, all it took was two minutes in my online banking.1 -

It’s Nationwide I am with.

They will offer you a new fix with no affordability checks, so your credit score and amount of debts wont matter, provided you dont have any mortgage arrears

So with my partners very good credit score and my fairly decent income does this still mean we’re screwed and never going to be able to get a bigger property?

No one is saying Never, but to a mortgage lender you havent been able to manage well financially with a lower mortgage, and also possibly lower interest rates, which doesnt look good. You need to see sorting out your debt as a big part of the key to ever being able to get a larger mortgage.

Is it best I go down the route of the DMP with StepChange?

A DMP is a likely option for you, that choice is separate from who manages your DMP which comes afterwards in your decision making.

Can you post a Statement of Affairs to first talk about the DMP? Include both your incomes and all debts, with names of lenders and the interest rates if possible https://www.stoozing.com/soa.php0 -

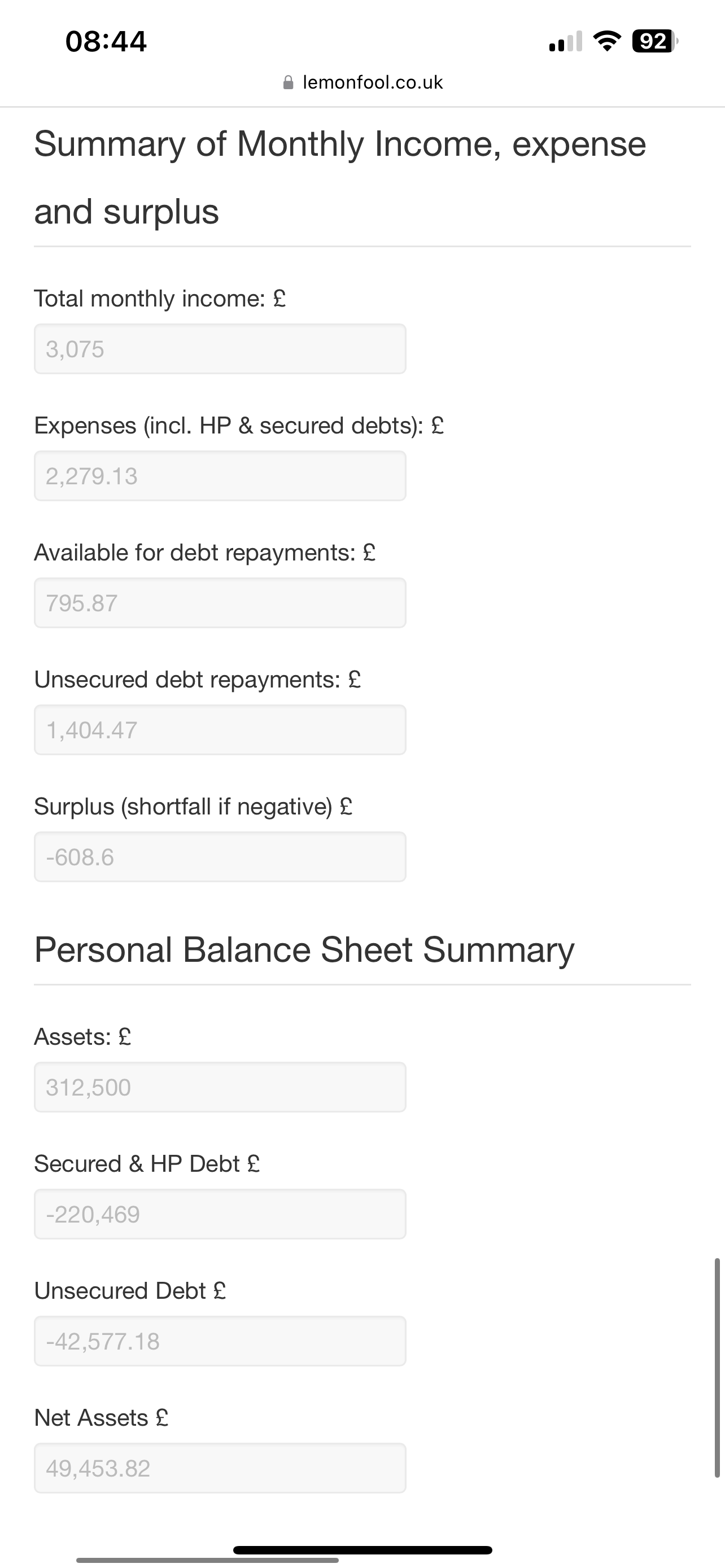

It’s not letting me copy it properly however I have screenshotted the summary below.

Rather than go down the route of a DMP could I use my equity in the house to clear it all and start fresh? 0

0 -

Securing nonpriority debt on your house would be folly, even assuming you could find a lender who would let you do it.

You have nearly £800 for a dmp. More than enough.

Your choice is whether to use a fee-free provider, like Stepchange or Payplan, or do it yourself.1 -

Thanks for the reply.fatbelly said:Securing nonpriority debt on your house would be folly, even assuming you could find a lender who would let you do it.

You have nearly £800 for a dmp. More than enough.

Your choice is whether to use a fee-free provider, like Stepchange or Payplan, or do it yourself.

Well we are planning on moving house anyway, what I meant by this was selling the house to remove ALL debt leaving us with £40-£50k equity as our next deposit for a slightly bigger house.I’m just wondering if a DMP is worth it at all I’ve I still have no spare cash at the end of the month to save up for things.

If I go down the route of a DMP is it best to cancel the DD’s and let it all default first?

thank you again0 -

That's magical thinking.Anon_09 said:

Well we are planning on moving house anyway, what I meant by this was selling the house to remove ALL debt leaving us with £40-£50k equity as our next deposit for a slightly bigger house.fatbelly said:

You are not removing ALL debt; you are just shifting relatively safe consumer debt to your more serious and dangerous secured debt load.

Even if your mortgage provider allows you, which they may not. You'll be paying for that holiday for the next 20 years, which racks up even on a low APR.

With respect to the DMP, the reason people here encourage others to share is that many SOAs are aspirational, based on what people think they spend.

Unless they actually track their spends, they miss all the occasional but intermittent items. They buy £233 of food, and spend another £150 on clothes and toys for the kids or pets and the "middle" "aisle." They may not go on holiday, but VFR requires chocolates or flowers and a bottle or 6 pack, every weekend.If you've have not made a mistake, you've made nothing1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.5K Banking & Borrowing

- 254.1K Reduce Debt & Boost Income

- 455K Spending & Discounts

- 246.5K Work, Benefits & Business

- 602.8K Mortgages, Homes & Bills

- 178K Life & Family

- 260.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards