We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

We're aware that some users are currently experiencing errors on the Forum. Our tech team is working to resolve the issue. Thanks for your patience.

How to pay money into a specific NI year?

andrewilley

Posts: 21 Forumite

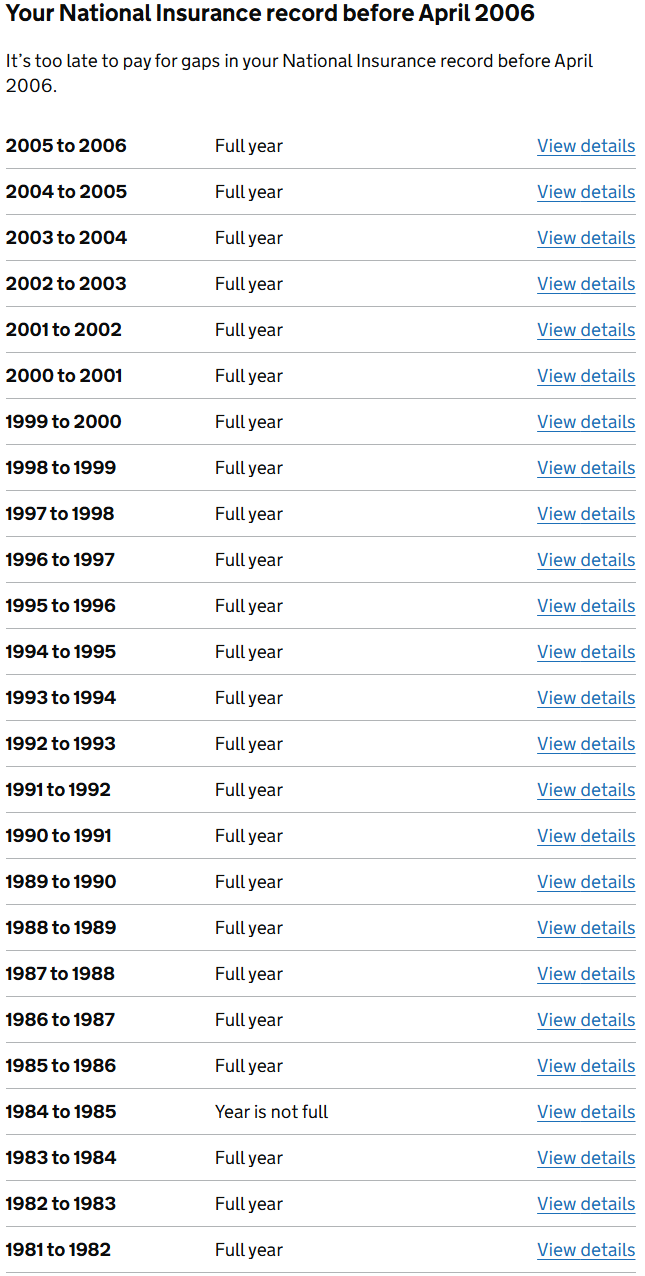

We've checked online for pension predictions for my wife, and currently her prediction is £190.72 per week as she is short by five non-full NI years. Her current income is below the NI threshold so she won't be adding any more years via work between now and her retirement in seven years. Carer years when my daughter was under 12 are fully credited, and we don't think there are any other years that can be added for free.

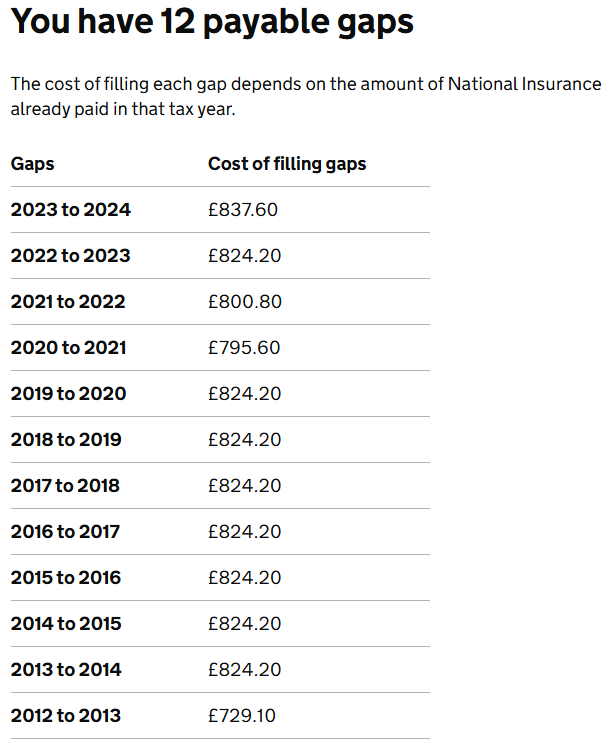

My wife plans to pay off the oldest (partial) year first while she still can - 2012-13, which is listed as costing £729.10 to complete. Some other slightly cheap years are all within the current six-year regular backdateable period - e.g. 2020-21 £795.60, and 2021-22 £800.80 - and she plans to pay them gradually over the next few years prior to her retirement rather doing a larger lump sum now.

Anyway, question is simple: how does she now pay £729.10 into the 2012-13 year to complete that year? We've tried online and it just offers a bizarre set of five random options for varying combinations of 1-5 years from the last five years. But no option to simply pay xxx into year yyyy. Is there an easy way to do this, or do we have to go through all the rigmarole of phoning them?

Andre

My wife plans to pay off the oldest (partial) year first while she still can - 2012-13, which is listed as costing £729.10 to complete. Some other slightly cheap years are all within the current six-year regular backdateable period - e.g. 2020-21 £795.60, and 2021-22 £800.80 - and she plans to pay them gradually over the next few years prior to her retirement rather doing a larger lump sum now.

Anyway, question is simple: how does she now pay £729.10 into the 2012-13 year to complete that year? We've tried online and it just offers a bizarre set of five random options for varying combinations of 1-5 years from the last five years. But no option to simply pay xxx into year yyyy. Is there an easy way to do this, or do we have to go through all the rigmarole of phoning them?

Andre

0

Comments

-

Are you certain that pre 2016 year will actually add to her pension amount?And yes, to pay a specific year you will have to speak to them.2

-

Why wouldn't it? I thought that if you need five missing years to be filled in (30 years are already full) then those could be any five years that are not currently full?molerat said:Are you certain that pre 2016 year will actually add to her pension amount?

Andre

0 -

You have misunderstood that.andrewilley said:

Why wouldn't it? I thought that if you need five missing years to be filled in (30 years are already full) then those could be any five years that are not currently full?molerat said:Are you certain that pre 2016 year will actually add to her pension amount?

Andre

Each person who started to build up an NI record before 2016 is different.

For a lot of people only post 2016 years will increase your State Pension.

1 -

andrewilley said:

Why wouldn't it? I thought that if you need five missing years to be filled in (30 years are already full) then those could be any five years that are not currently full?molerat said:Are you certain that pre 2016 year will actually add to her pension amount?

AndrePost 2016 years will always add value, pre 2016 years are dependent on personal circumstances. Post up the following anonymous info and someone will work it out for you.Current weekly £££.pp amount up to April 2024.

Number of full NI years 15-16 and earlier

Number of full NI years 16-17 and later

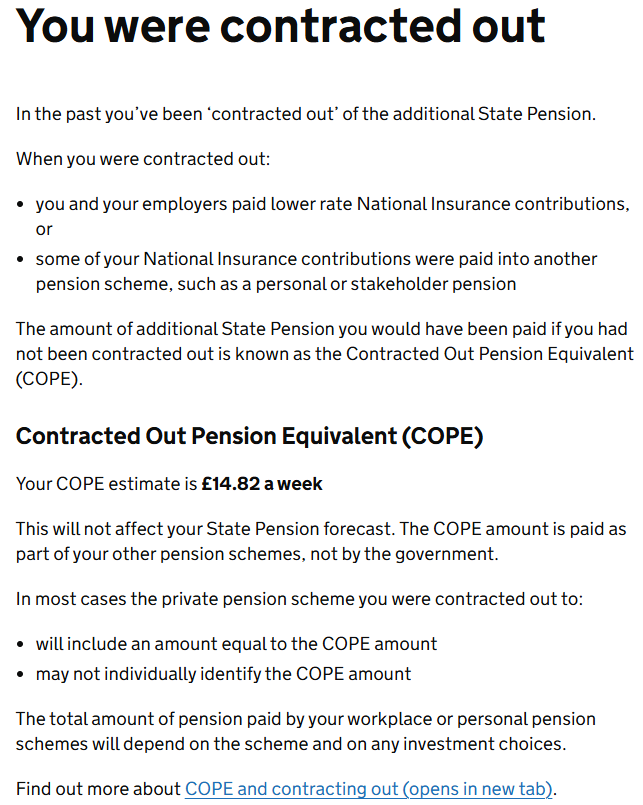

Any COPE amount. If you have "You've been in a contracted-out pension scheme" on your forecast then click

here https://www.tax.service.gov.uk/check-your-state-pension/account/cope whilst logged into your tax account

3 -

Thank you. I think the following covers all of the above questions without any personally identifiable info. Hadn't considered the COPE possibility, must have been a long time ago now and she has no knowledge at all of it now. As I said before, there will be no further full NI years from part-time employment from now until retirement in approx seven years.

0 -

From that info any year 15-16 and earlier will not add to the pension, she needs to fill up from 16-17 and later.At April 2016 she had a starting amount of £134.24 based on old rules against new rules of £118.59. She is limited to 30 years under old rules so cannot add more. If you were allowed to buy more it would simply add to the new rules amount at £4.45 per year so you an see you would need to buy 4 to end up with £2 more pension at 2016 rates.2

-

Molerat has nailed it thereHer starting amount at 6th April 2016 was calculated as greater ofa) (old rules) 30/30 x 119.30 + 14.90 = 134.20 andb) (new rules) (30/35 x 155.65) - 14.82 = 118.59where 119.30 is the basic state pension at 6th April 2016and £155.65 is the new state pension at 6th April 2016and £14.90 is the additional state pension earned to 6th April 2016And the higher of these two figures is £134.20pw (which agrees molerat ignoring rounding errors)And the current amount is 134.20 x 1.025056 x 1.030085 x 1.025859 x 1.039146 x 1.025114 x 1.030902 x 1.100999 x 1.085112 = 190.72where these multipliers are the 2017 to 2024 (inclusive of both) triple lock increasesAs molerat says she could buy the 4 pre 2016 years but that wouldn't change the old rules calculation part of the starting amount in a) above (as the maximum number of years in that part is 30 years) and so most of that money would be wasted bringing the new rules calculation up to the old rules amount, and ultimately would only increase the starting amount in total by about £2pw. And buying 3 years up to 2015/2016 (rather than 4) wouldn't increase her state pension at all.So she needs to fill up from 2016/2017 and later only as that numerically is a better option, as state pension accrual for those years adds on to the starting amount (rather than 2015/2016 and earlier which are components of the starting amount calculation) up until the full new state pension is reached.

I came, I saw, I melted0 -

Thank you. So the fact that she already has 30 full years prior to 2016 is the limiting factor here, not the contracting out bit (which she is adamant that she never would have asked for anyway, so it must have been something a workplace pension company did that she didn't notice).

So she can still fill in her five missing years, but they must be years from 2016-17 onward. Presumably it makes sense to start by filling in the slightly cheaper years first - so 2020-21 and 2021-22 - and then the others can be done over the next few years rather than as a large lump sum, as long as they are completed before she retires.

Or is filling missing years likely to rise in cost significantly over time, so she'd be better off paying three more older £824.20 years (2016-19) while she still can, rather than earning interest on it herself in the meantime?

Andre0 -

It's the contracting out that has reduced her new scheme starting amount to well below the old scheme amount meaning she is governed by the rules of that old scheme so 30 max. She can take as many and whichever 16-17 and later years as she needs.4 years will add £6.32 each and the 5th the final £5.200

-

Yes the fact that she already had 30 years prior to 2016 is the limiting factor (combined with the fact that the old rules calculation is higher than the new rules calculation in her case).Yes filling in cheapest 2016-2017 and after years first makes sense.The first 4 years purchased will each add £6.32pw in 2024/2025 terms and the fifth will add about £5.20pw in 2024/2025 terms as that will be the balancing amount to get her up to the full new state pension.If your wife ever earns more than the lower earnings limit (£6,396 pa or £123pw for 2024/2025) then she may earn a post 2016 year through earnings, and similarly if she might gain a year if she ever qualified for national insurance credits, so if that ever happened it would be wasted money to buy all 5 years. I note she currently earns less than this.I came, I saw, I melted0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards