We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

CCA - reconstituted agreement provided

Hello

Many thanks for all your help previously on this Forum about my debts, it’s been a great support mentally for what is a really frightening and stressful situation. As an update: All accounts have now defaulted and I have sent away for CCA for the accounts that have been sold. I have now had back from Cabot a reconstituted copy of my credit card agreement for one of my cards.

They ‘consider that the agreement is now enforceable and therefore we are entitled to obtain a Count Court Judgement against you. However, we would prefer that you work with us to set up a repayment plan to settle your outstanding balance.’

They have also included a signed ‘Statement of Account’, but this is from Cabot and just includes how much is outstanding, how much I am required to pay, that I can’t use the account anymore. Should they have included actual Credit Card Statements, or is this enough to fulfil their legal obligations?

I know that I now need to work out a repayment plan with Cabot for this card, and they have asked me to call them. I don’t want to speak to anyone (would be too stressful), so can I just go on to their website and set up a monthly amount I can afford? (working on the basis that I have other credit card debts which I might/will have to start a repayment plan for, so can’t allocate all my ‘spare’ money to this one card and I don’t have a lump sum to offer for a settlement.)

If I set up a payment plan, can they still take me straight to court if they want the amount to be higher? Do I have to e.g. give them payslips/details of who I work for, etc? And can I ask them to only contact me via the post? (even though this CCA request took over a week to arrive).

Any help and advice greatly appreciated.

Comments

-

Yes they should have provided you with statements, you could argue that by not doing so, they have not properly fulfilled their obligations under section 77, so you might want to remind them of that.

Forget all talk of going to court, although its not something you should be afraid of, you don`t actually attend, its all done by post and online, and will not happen once you set up a payment plan, and you have no more disputes to settle.

Affordability is key these days,, they are under strict instructions from the FCA to make certain payments are affordable, so they will ask for proof of income, but you can simply refuse if you wish, they cannot penalise you, but they may refuse your payments if they have reason to think you can`t afford them.

You can pay online as and when you wish.

And to answer your last question, yes you can tell them to contact you in writing only, quote GDPR to them (General Data Protection Regulations), and tell them what you want them to do.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter1 -

Many thanks @sourcrates - does that mean then that by not providing the actual credit card statements the debt remains unenforceable? And if so, should I write to them first and ask for all the statements before setting up a repayment plan? Thanks0

-

By not providing historic statements they have failed in their duty to fully comply with sec 77, now does that mean the debt is unenforceable ?

Well a previous poster got their creditor to admit their debt was unenforceable because they had failed to provide historic statements when asked, but in reality, only a court can actually decide whether that is the case or not.

This certainly puts you in a good position, as I said above you may want to address this with Cabot before you agree to pay anything.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter1 -

Many thanks @sourcrates - really appreciate the advice, I’ll write to Cabot and see what they say.0

-

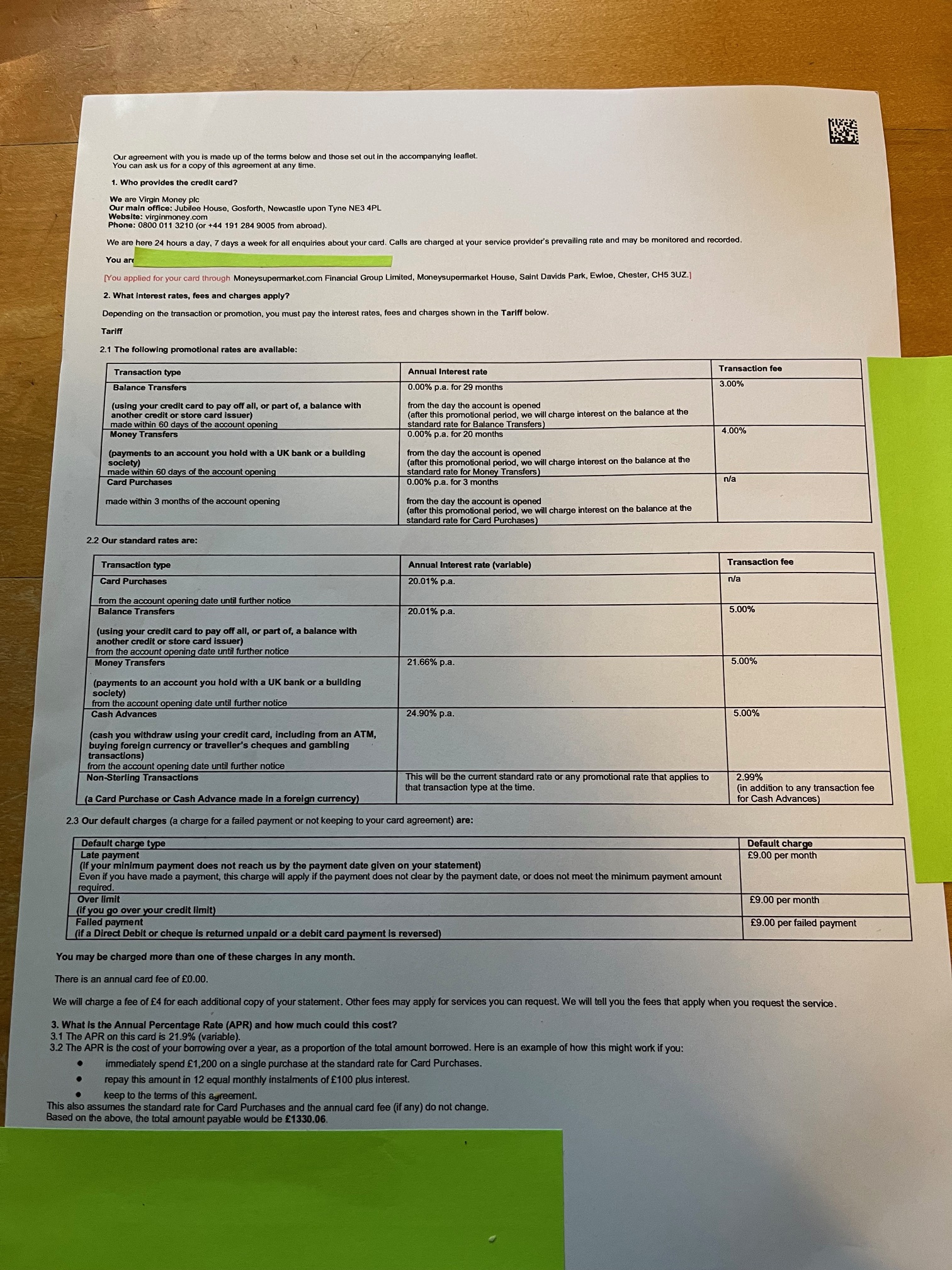

Hello - still ongoing with Cabot as per the above comments, but have now had a CCA request back from Lowell who bought my Virgin Credit Card.

I’ve been sent all the actual monthly statements, but for what I assume is supposed to be the CCA, just 2 x versions of the attached sheet (with different interest rates). This doesn’t feel like a full CCA, and is not as complete with T&Cs as the one Cabot sent me for a different card?

Should I go back to Lowell and query this or in your opinion(s) is this enough to meet the legal requirements of sections 77 & 78 of the Consumer Credit Act 1974? (I’ve also noticed in section 3.1 it’s quoting the incorrect APR, although this rate is on both sheets received in this section). All advice very much appreciated.

0

0 -

Its always difficult to advise on these matters, as we always point out, only a court can decide what is ,and what isn`t compliant when it comes to copy agreements.

Debt Camel sets out the criteria for what you should expect to be included on any copy credit agreement:

Debts - why, how & when to ask for the CCA agreement · Debt Camel

If you think its deficient in some way, then you must convince Cabot of that, and hope they don`t test that theory by issuing court papers, because if you rely on this as a defence, you should be prepared to go all the way with it, so you must be certain of your position.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter2 -

Hello - I’ve been thinking about this and am going to write back to Lowell and say I don’t they have provided the actual full Credit Agreement as the information provided does not include all the information it should have (have had a look as well at advice posted on and by Debt Camel and Legal Beagles). Should I tell Lowell what I believe is missing or just say that what they have sent me doesn’t meet the requirements under the CCA 1974 and they shouldn’t state that it does as that is misleading? Any advice or info on similar previous experience very much appreciated. Thank you0

-

You can tell them you believe the paperwork is defective, you can also point out what you think is missing from it that doesn't make it compliant, but do not get too caught up in legalities, you are a layman, not a solicitor, just state the facts, nothing more.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.6K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.7K Work, Benefits & Business

- 603K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards