We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Scottish Widows AMC’s - too high or not?

Forever_Red

Posts: 176 Forumite

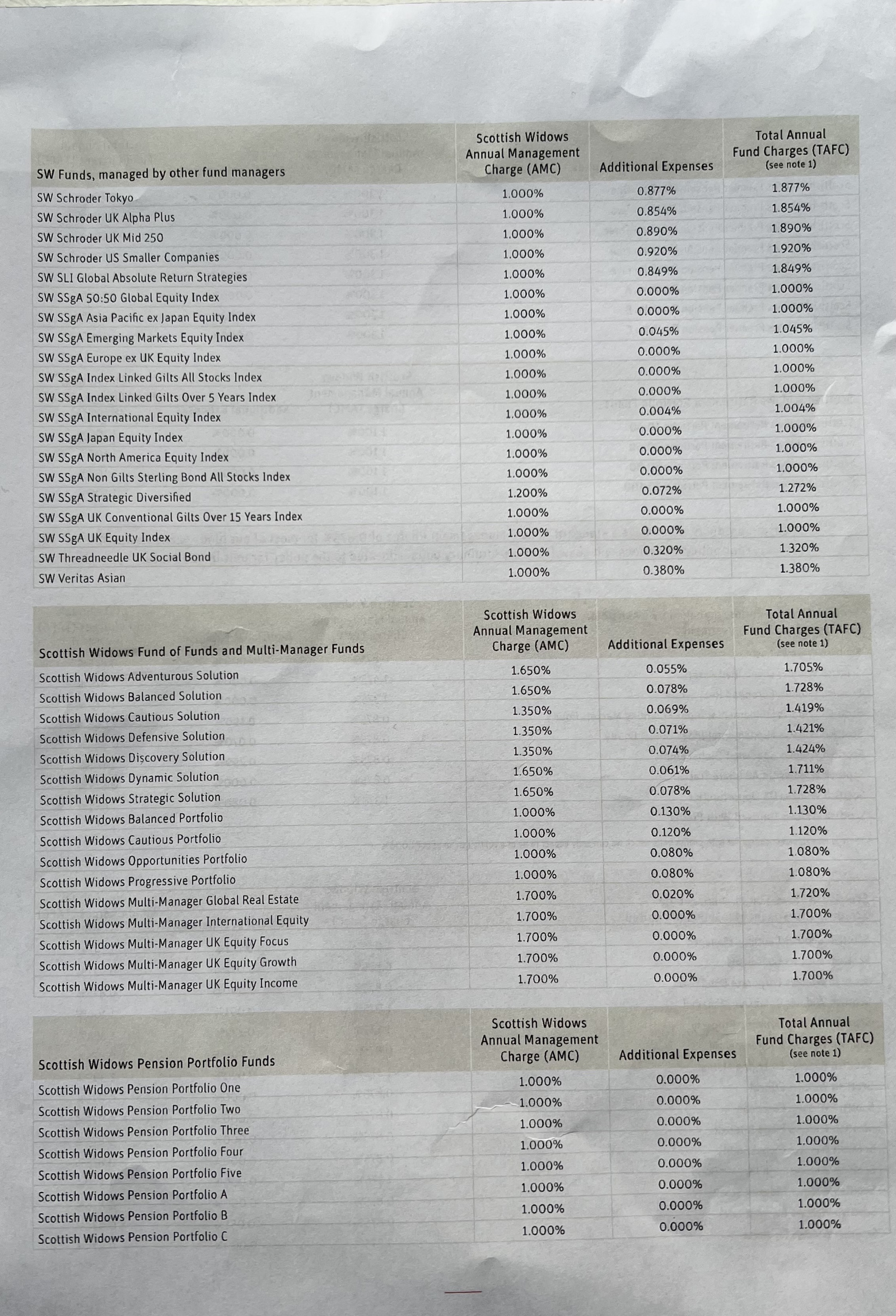

I’m trying to sort out my daughter’s Scottish Widows pension and switched out of the default fund as she’s 24 and has the time to go with a higher risk fund.

I’ve chosen the SW SSgA International Equity Index and see the charges listed as 1.004% (1% AMC and 0.004% additional charge) even though she’s actually charged 0.754% (0.65% SW fund based charge, fund charges AMC 0.1% & fund expenses 0.004%) maybe a discount through her employer 🤷♂️.

Even with the discount, does the charge seem high? Looking at the 4 pages of funds and charges, they are all over 1% and even as high as 2.3%.

Do these seem excessively high?

Thanks

Forever Red

Even with the discount, does the charge seem high? Looking at the 4 pages of funds and charges, they are all over 1% and even as high as 2.3%.

Do these seem excessively high?

Thanks

Forever Red

F.C United - Onwards and Upwards

0

Comments

-

The additional expenses column can be ignored. That equates to the transaction charges figure on OEICs/UTs. its a synthetic calculation rather than an explicit fee and there are multiple ways to calculate it and inconsistency across the fund houses. So, it is largely meaningless and ignored by most investors.Do these seem excessively high?No. There is better available, but they are not excessive either. As you say, it's 0.65% all in, so that is not bad.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

The total charges are 0.754% but I thought the general consensus (YouTubers and Diyers) was avoid paying more than 0.4 - 0.5% all in 🤷♂️dunstonh said:As you say, it's 0.65% all in, so that is not bad.F.C United - Onwards and Upwards0 -

You asked if the charge was excessive. It is not excessive and, as I said, you can get cheaper.Forever_Red said:

The total charges are 0.754% but I thought the general consensus (YouTubers and Diyers) was avoid paying more than 0.4 - 0.5% all in 🤷♂️dunstonh said:As you say, it's 0.65% all in, so that is not bad.

However, workplace schemes have a 0.75% cap on internal funds and its the employer that picks the workplace scheme. So, you don't have a choice to change provider with your current employer. Free money from the employer is far more important that a 0.2x% difference/

Also, those YouTubers and DIYers won't be including the TC figure in that 0.4-0.5% range. You are including it.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.2 -

As said , 0.65% all in is not excessive but not cheap either.

As it is the provider her employer has chosen, then there is not a lot that can be done about it.

In any case as presumably her level of funds is not that high yet, then in cash terms it is not a lot.

Differences of 0.2% etc tend to become more of an issue when the funds build up to a more significant sum.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards