We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Payplan £26k debt - F&F Payment

I’m currently in £26k worth of debt. I have been with Payplan since July 2024, making £703 monthly payments.

It’s my husband and I’s goal to be debt free by the beginning of 2026.

Since starting my DMP, my husband started a new job which pays him very well and has allowed him to be able to pay his debt (currently £9k) quicker than expected and then save some money on the side. We are budgeting to have around £10k saved by the end of December. By that point my debt should stand at £18.4k

So we wanted to know how likely or how can we prepare ourselves to offer final payment settlements to my creditors. I have read that debt sold to third parties are more likely to accept 40-55% of the debt.

I have gone through my list of creditors and I can see that some of them haven’t been sold to a debt recovery agency. Eg Tesco, I believe this is because the monthly payment offered to them by Payplan is actually more than what the agreed monthly repayment is. To the point where every month I get a letter from them thanking me for my overpayment. For this reason, I was thinking of “changing the outgoings” when doing my Payplan yearly DMP calculation so my monthly payments are reduced and hopefully Tesco ends up selling my loan too. Is this a plausible idea? What do you recommend me to do?

Also, I’m not sure if this is relevant but I’m planning to get pregnant in June-July, which would mean I’m going to go on maternity leave in March-April 2026 so my salary will reduce to SMP.

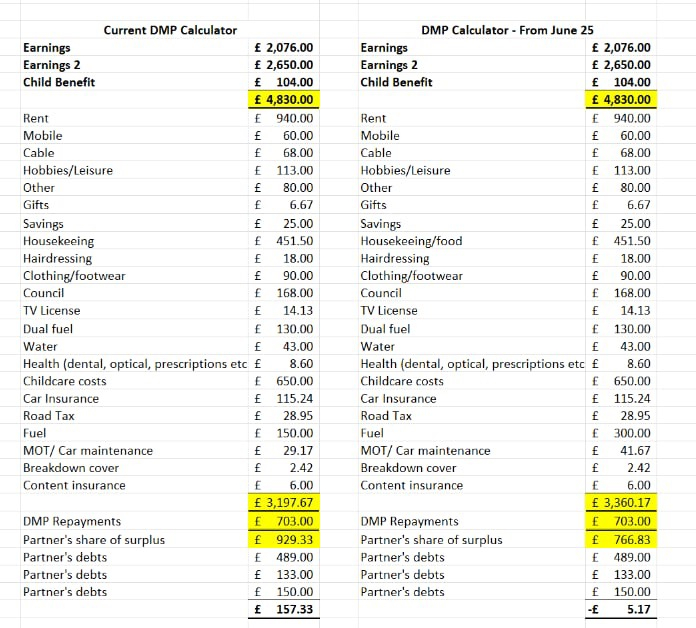

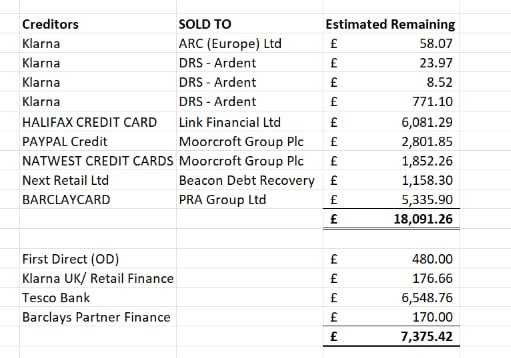

I have attached my current DMP and creditor list.

Tia, a mum on her way to be debt free.

Comments

-

If you want to do full and finals, you probably need to self manage. There is a whole thread on people's most recent successes.If you've have not made a mistake, you've made nothing0

-

https://forums.moneysavingexpert.com/discussion/115430/full-and-final-settlement-help-thread#latest

That’s the thread that RAS was referring to I think.

Self manage means that you cancel your DMP with Payplan and deal with your creditors yourself.

Have all your debts defaulted? If Tesco has not defaulted you are probably under an arrangement to pay and if you are actually paying more than what your monthly payment should be there is no incentive for the creditor to accept a reduced full and final payment.

In a self managed DMP you stop paying creditors until they default the debt and then you can start paying reduced amounts to whoever owns it. Some creditors keep the accounts in house, others instruct debt collectors to deal with it and others sell the debt. Then further down the line they normally accept full and final payments at a reduced amount.

Also with Payplan they will probably insist in sharing whatever money you have available for full and final payments between all your creditors. In a self managed DMP you decide how you manage your payments.

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.8K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards