We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Advice Needed: Pension Consolidation and Financial Advisor Costs

Comments

-

Really easy and highly recommended. 😃Marcon said:

Practical suggestion as requested!artyboy said:

Oh dear god...Ibrahim5 said:The difference is that the financial advisor takes his fees from your pension whereas your decorator, mechanic, gardener or cancer doctor can't. So they can charge crazy amounts for filling a few forms in. They charge much, much more than a real professional like a cancer doctor whose job is much, much more complicated.

OP, welcome. A first suggestion, please take what this poster says with a very very large pinch of salt. They have clearly been burnt by financial advice in the past and now feel it is their mission to slate, denigrate and abuse them and their profession at every turn.I urge you to check their other posts if you don't wish to take my word for it. Others will be along with better practical suggestions than I can give, but please don't be put off on your first thread.

OP - look up to the top right of the screen and you'll see some icons on the dark green bar. To the right of the envelope icon is your own user icon.

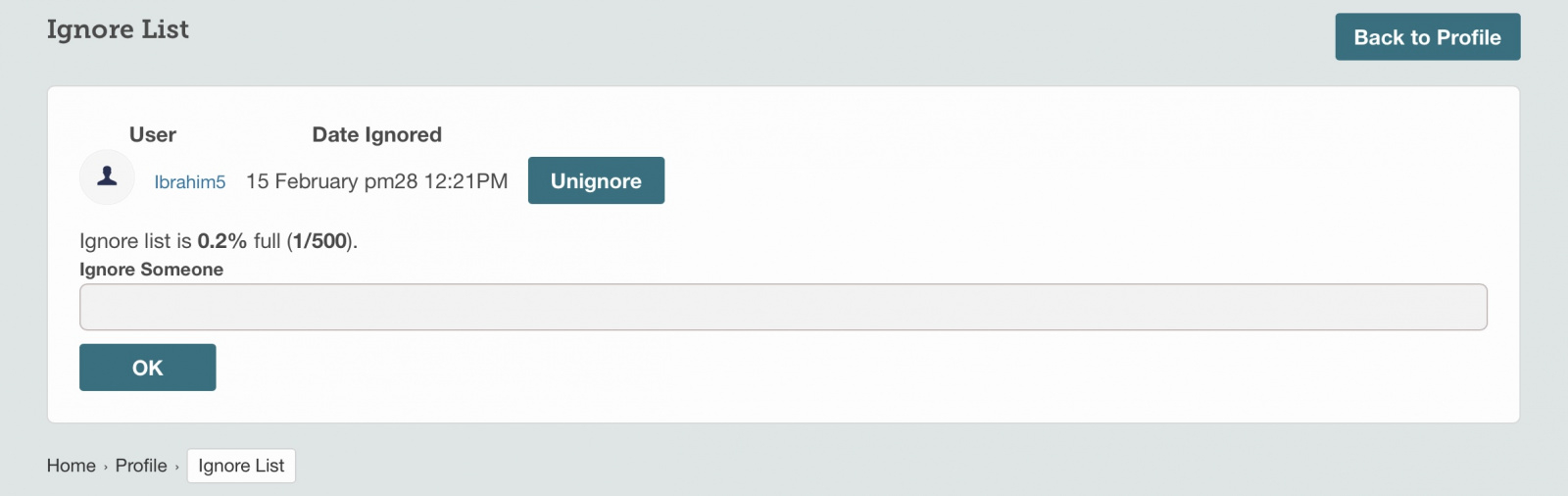

Click on that and then hit 'Account and Privacy Settings' (immediately underneath your posting name and email address). Click on 'Ignore' list and add any posters whose posts aren't in your opinion worth reading.

It's a really useful function and means you don't have to keep reading nonsense from people who keep posting the same pointless and unproductive nonsense.

2 -

Warning - anyone ignoring me will miss out on top tips and could end up much poorer as a result.0

-

As apparently the last surviving member of the once populous forum's IFA haters club, I will not ignore you as you are now probably an endangered species !Ibrahim5 said:Warning - anyone ignoring me will miss out on top tips and could end up much poorer as a result.1 -

Always worth reading for amusement. Please let us know when the top tips are due.Ibrahim5 said:Warning - anyone ignoring me will miss out on top tips and could end up much poorer as a result.

3 -

It isn’t difficult at all to do it yourself, and you’re likely to save tens of thousands in costs over the lifetime of investing. Whilst IFAs and similar have their uses, a simple pension (as distinct from, say, some of the tax planning aspects) should be understandable to almost all.

At the very simplest end, transfer your pensions to a low cost provider such as Vanguard and use one of their basic funds such as life strategy. Set the equity component to a level consistent with how much risk you want to take (they have tools to help with this) and then forget about it. The only issue with this approach is that it isn’t the absolute cheapest (though still much cheaper than SJP and their ilk) and, depending on your current pension arrangements, you might need to transfer future employer pension contributions into the funds periodically (e.g. annually) yourself.

If you want more control you can set up on a platform where you have the universe of funds to choose from. To minimise costs you can see which platforms work best using comparison tools on sites such as Monevator or Bankeronwheels. These sites also have plenty of good advice on funds and investing.2 -

A pretty solid first post there, to the newbie OP 👍Labtebricolist said:It isn’t difficult at all to do it yourself, and you’re likely to save tens of thousands in costs over the lifetime of investing. Whilst IFAs and similar have their uses, a simple pension (as distinct from, say, some of the tax planning aspects) should be understandable to almost all.

At the very simplest end, transfer your pensions to a low cost provider such as Vanguard and use one of their basic funds such as life strategy. Set the equity component to a level consistent with how much risk you want to take (they have tools to help with this) and then forget about it. The only issue with this approach is that it isn’t the absolute cheapest (though still much cheaper than SJP and their ilk) and, depending on your current pension arrangements, you might need to transfer future employer pension contributions into the funds periodically (e.g. annually) yourself.

If you want more control you can set up on a platform where you have the universe of funds to choose from. To minimise costs you can see which platforms work best using comparison tools on sites such as Monevator or Bankeronwheels. These sites also have plenty of good advice on funds and investing.

For general advice on investing, I’m broadly a fan of the Lars approach - spend 20 minutes listening to his videos at https://kroijer.com. TL/DR - invest in the world at the lowest cost 🤷♂️

My only other suggestion would be that your choices should only be between DIY (eg, a Vanguard pension or similar) or IFA - the I (Independant) being the important bit 💪

There isn’t a barge pole long enough to make me touch the likes of SJP - when they claim to be about Wealth Management, remember it is likely to be their wealth they are improving the most 😉Plan for tomorrow, enjoy today!1 -

You're new to this forum and it shows... Have a read of some of the previous threads and you'll realise that your perfectly sensible sentiment is massively wide of the mark - something most of us who have worked in pensions for decades can confirm from empirical evidence!Labtebricolist said:It isn’t difficult at all to do it yourself, and you’re likely to save tens of thousands in costs over the lifetime of investing. Whilst IFAs and similar have their uses, a simple pension (as distinct from, say, some of the tax planning aspects) should be understandable to almost all.Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0 -

Thanks for that. I’ve no personal dog in this race, and make no comment on what seems to be your assumption that most people are too dumb to understand a pension.Marcon said:

You're new to this forum and it shows... Have a read of some of the previous threads and you'll realise that your perfectly sensible sentiment is massively wide of the mark - something most of us who have worked in pensions for decades can confirm from empirical evidence!Labtebricolist said:It isn’t difficult at all to do it yourself, and you’re likely to save tens of thousands in costs over the lifetime of investing. Whilst IFAs and similar have their uses, a simple pension (as distinct from, say, some of the tax planning aspects) should be understandable to almost all.My view is that people should look into this sort of thing themselves. If they then feel they need to and can afford to pay for advice then they should do so, but they shouldn’t go into long-term decisions from the starting point of dependence on others.0 -

The level of understanding of personal finance in the general public is abysmal, not helped by a lot of people being poor at basic arithmetic.Labtebricolist said:

Thanks for that. I’ve no personal dog in this race, and make no comment on what seems to be your assumption that most people are too dumb to understand a pension.Marcon said:

You're new to this forum and it shows... Have a read of some of the previous threads and you'll realise that your perfectly sensible sentiment is massively wide of the mark - something most of us who have worked in pensions for decades can confirm from empirical evidence!Labtebricolist said:It isn’t difficult at all to do it yourself, and you’re likely to save tens of thousands in costs over the lifetime of investing. Whilst IFAs and similar have their uses, a simple pension (as distinct from, say, some of the tax planning aspects) should be understandable to almost all.My view is that people should look into this sort of thing themselves. If they then feel they need to and can afford to pay for advice then they should do so, but they shouldn’t go into long-term decisions from the starting point of dependence on others.

If you stopped 10 people in the street and asked them to explain the difference between DC and DB pensions, you would get at least 9 blank looks .

Probably a similar result if you asked them what an ETF or a multi asset fund was.2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.3K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards