We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

The Old Regular Savers Discussion Thread 28/12/24-29/1/26

Comments

-

clairec666 said:

One pro for the Beverley account is that it appears to be open-ended, so your money won't mature into a lower-paying account after a year. The benefits of this are somewhat negated by the strict withdrawal conditions and the massive interest drop if you make a withdrawal.subjecttocontract said:There was no criticism meant on my part, I just wanted to understand why the Beverley account seemed to be so attractive.......in case I was missing something. The comments on here have persuaded me that the Manchester reg saver will make an ideal easy access account which I will open. Many thanks.

It might be a helpful account for some people, if for example they know they're unlikely to need access to the money, if they've already maxed out their ISA and all higher-paying regular savers, etc.Another possible reason - an old favourite - is having at least one account with a provider to potentially qualify for loyalty products.Depositing £10 per month into an online-only account paying 5.5% might be seen by some as better than sticking £1 in the instant access passbook account at 2%. Opinions are likely to vary though.3 -

I think another positive for the Beverley BS account is that it's available as a joint account if required, which I think is quite rare for a Regular Saver. I can only think of this and the Co-Op Bank RS off the top of my head which are available in joint names.Section62 said:clairec666 said:

One pro for the Beverley account is that it appears to be open-ended, so your money won't mature into a lower-paying account after a year. The benefits of this are somewhat negated by the strict withdrawal conditions and the massive interest drop if you make a withdrawal.subjecttocontract said:There was no criticism meant on my part, I just wanted to understand why the Beverley account seemed to be so attractive.......in case I was missing something. The comments on here have persuaded me that the Manchester reg saver will make an ideal easy access account which I will open. Many thanks.

It might be a helpful account for some people, if for example they know they're unlikely to need access to the money, if they've already maxed out their ISA and all higher-paying regular savers, etc.Another possible reason - an old favourite - is having at least one account with a provider to potentially qualify for loyalty products.Depositing £10 per month into an online-only account paying 5.5% might be seen by some as better than sticking £1 in the instant access passbook account at 2%. Opinions are likely to vary though.

Does anyone know of any others?0 -

You can search Moneyfacts for Regular Savers which allow joint accounts.hgt said:

I think another positive for the Beverley BS account is that it's available as a joint account if required, which I think is quite rare for a Regular Saver. I can only think of this and the Co-Op Bank RS off the top of my head which are available in joint names.Section62 said:clairec666 said:

One pro for the Beverley account is that it appears to be open-ended, so your money won't mature into a lower-paying account after a year. The benefits of this are somewhat negated by the strict withdrawal conditions and the massive interest drop if you make a withdrawal.subjecttocontract said:There was no criticism meant on my part, I just wanted to understand why the Beverley account seemed to be so attractive.......in case I was missing something. The comments on here have persuaded me that the Manchester reg saver will make an ideal easy access account which I will open. Many thanks.

It might be a helpful account for some people, if for example they know they're unlikely to need access to the money, if they've already maxed out their ISA and all higher-paying regular savers, etc.Another possible reason - an old favourite - is having at least one account with a provider to potentially qualify for loyalty products.Depositing £10 per month into an online-only account paying 5.5% might be seen by some as better than sticking £1 in the instant access passbook account at 2%. Opinions are likely to vary though.

Does anyone know of any others?

I believe there are around 40 listed.3 -

I don't think it's criticism. It's a discussion of the pros and cons of an atypical account.friolento said:trickydicky14 said:

Am I missing something, why not open the new Manchester B.S regular saver. Same rate 5.5% also variable and up to £500 a month and with easy access without all the conditions. And it runs for 2 years. And the system is fast, my deposit showed within an hour plus you get a text and email to tell you it's arrived.subjecttocontract said:

I still don't understand the accounts attraction unless, you already have the many other reg savers that pay more than 5.5%.Stargunner said:

That is correct.subjecttocontract said:

Well it's hardly easy access. I thought that if you withdraw money from the account..... doesn't the interest paid stay at 1% ?Stargunner said:

5.5% is higher than my EA savings accounts, so I have gone for it.subjecttocontract said:Yes I can understand that, the 4.15% would annoy me as well.

The Beverley 5.5% would annoy me as well, that's why it's not being opened by me. It would get shown up by all the others that provide a better return.

i don’t need it to be easy access, but as it pays more than my easy access accounts I have gone for it.

What's all the criticim of people who opened accounts that you wouldn't open? Why do you assume that those who opened the Beverley one don't already have at least one Manchester one?

I really appreciate these posts as I'm on the fence about it at the moment.5 -

Yes, a big thumbs up to the people who keep us up to speed with changing interest rates.s71hj said:

The risk associated with the loss of interest if the rate reduces such that you want to withdraw seems to be totally offset if I understand correctly that in the event of an interest reduction you have 30 days to withdraw. I say totally offset, it depends on you noticing a rate change buried in your email inbox, another reason to obsessively follow this thread!!!!clairec666 said:

One pro for the Beverley account is that it appears to be open-ended, so your money won't mature into a lower-paying account after a year. The benefits of this are somewhat negated by the strict withdrawal conditions and the massive interest drop if you make a withdrawal.subjecttocontract said:There was no criticism meant on my part, I just wanted to understand why the Beverley account seemed to be so attractive.......in case I was missing something. The comments on here have persuaded me that the Manchester reg saver will make an ideal easy access account which I will open. Many thanks.

It might be a helpful account for some people, if for example they know they're unlikely to need access to the money, if they've already maxed out their ISA and all higher-paying regular savers, etc.

You're right, there's a get-out clause on the Beverley account if interest rates drop. Although in the unlikely event that interest rates suddenly soar and Beverley decide not to raise theirs, there's no such clause. In which case, it's the perfect excuse to make a spreadsheet to decide whether it's better to lose the bonus rate to move your money elsewhere 0

0 -

Just opened the AIB RS - guess that's my Monmouthshire (I live in NI)

It was annoying me that the Mon RS wasn't available to those of us in NI1 -

And another note... like Mon, AIB is so slow0

-

Can anybody help?

For the AIB RS, what do they count as a month for the max £500?

Does it reset at the start of the month like many, or is it (like the Zopa RS) every month when opened?

Have set up an instruction to add £ on 1st Oct. Condition of account. Earliest that can take effect.

Thinking I could however deposit a full £500 this month if it was calendar month...

Just can't go over, as the interest rate goes down.

0 -

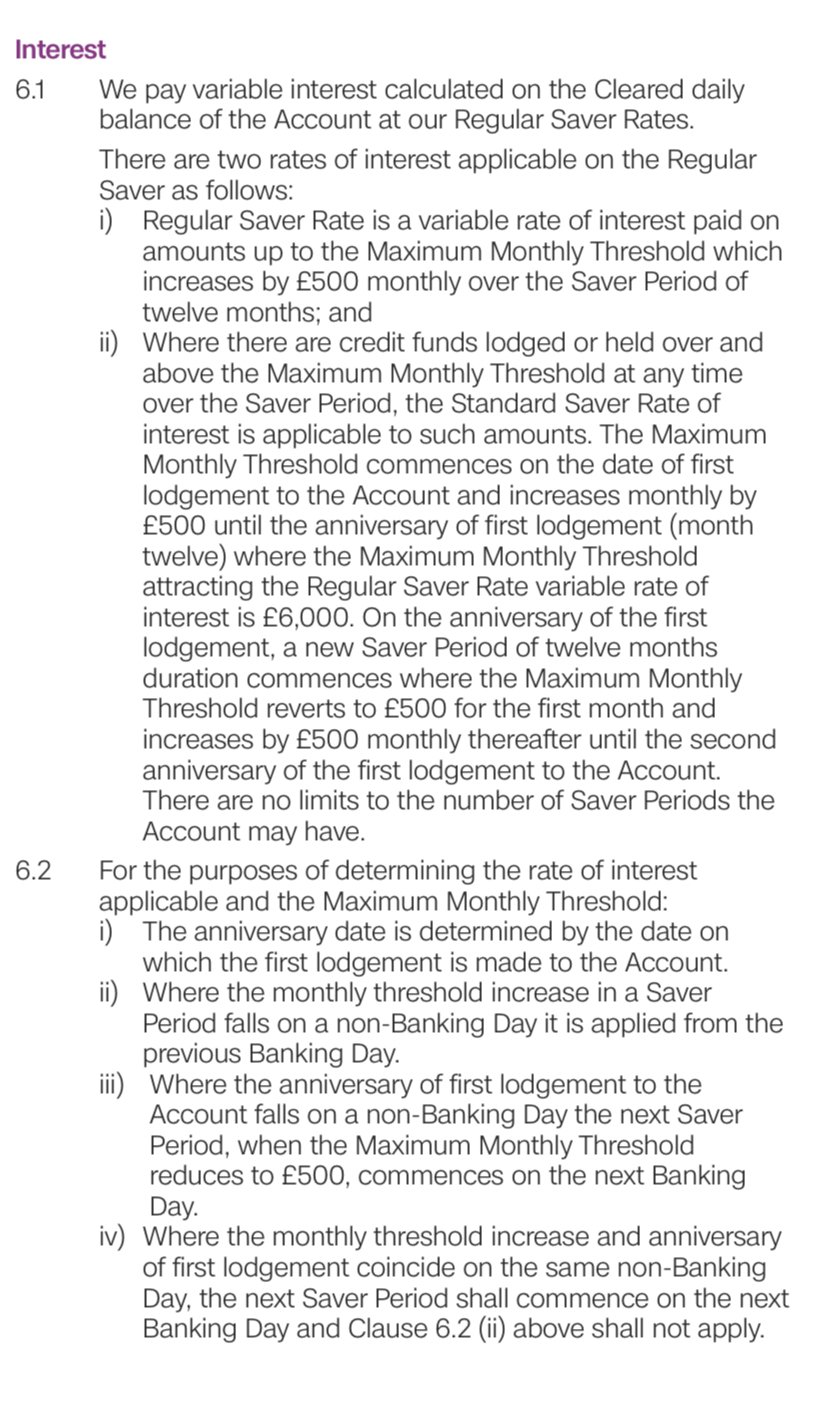

The AIB RS does not start until funded. The months for deposits are then set from the date of your first deposit. For example, if you open today the 26th, every AIB Month for your account would start on the 26th and you would be able to fund up to £500 each month, i.e up until the 25th.topyam said:

Can anybody help?

For the AIB RS, what do they count as a month for the max £500?

Does it reset at the start of the month like many, or is it (like the Zopa RS) every month when opened?

Have set up an instruction to add £ on 1st Oct. Condition of account. Earliest that can take effect.

Thinking I could however deposit a full £500 this month if it was calendar month...

Just can't go over, as the interest rate goes down.

EDIT: Use the following link and look at "How does it work?" and the first Aid in particular Regular Saver - AIB (NI) Personal Banking1 -

There is no maximum monthly pay in limit. The amount you can earn the 6% on increases by £500 each month on the same date that you made your first payment in. Anything in the account above the threshold earns pittance.topyam said:

Can anybody help?

For the AIB RS, what do they count as a month for the max £500?

Does it reset at the start of the month like many, or is it (like the Zopa RS) every month when opened?

Have set up an instruction to add £ on 1st Oct. Condition of account. Earliest that can take effect.

Thinking I could however deposit a full £500 this month if it was calendar month...

Just can't go over, as the interest rate goes down.1

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.6K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.6K Work, Benefits & Business

- 603K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards