We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Variable Pension / annual allowance

mindboggles

Posts: 3 Newbie

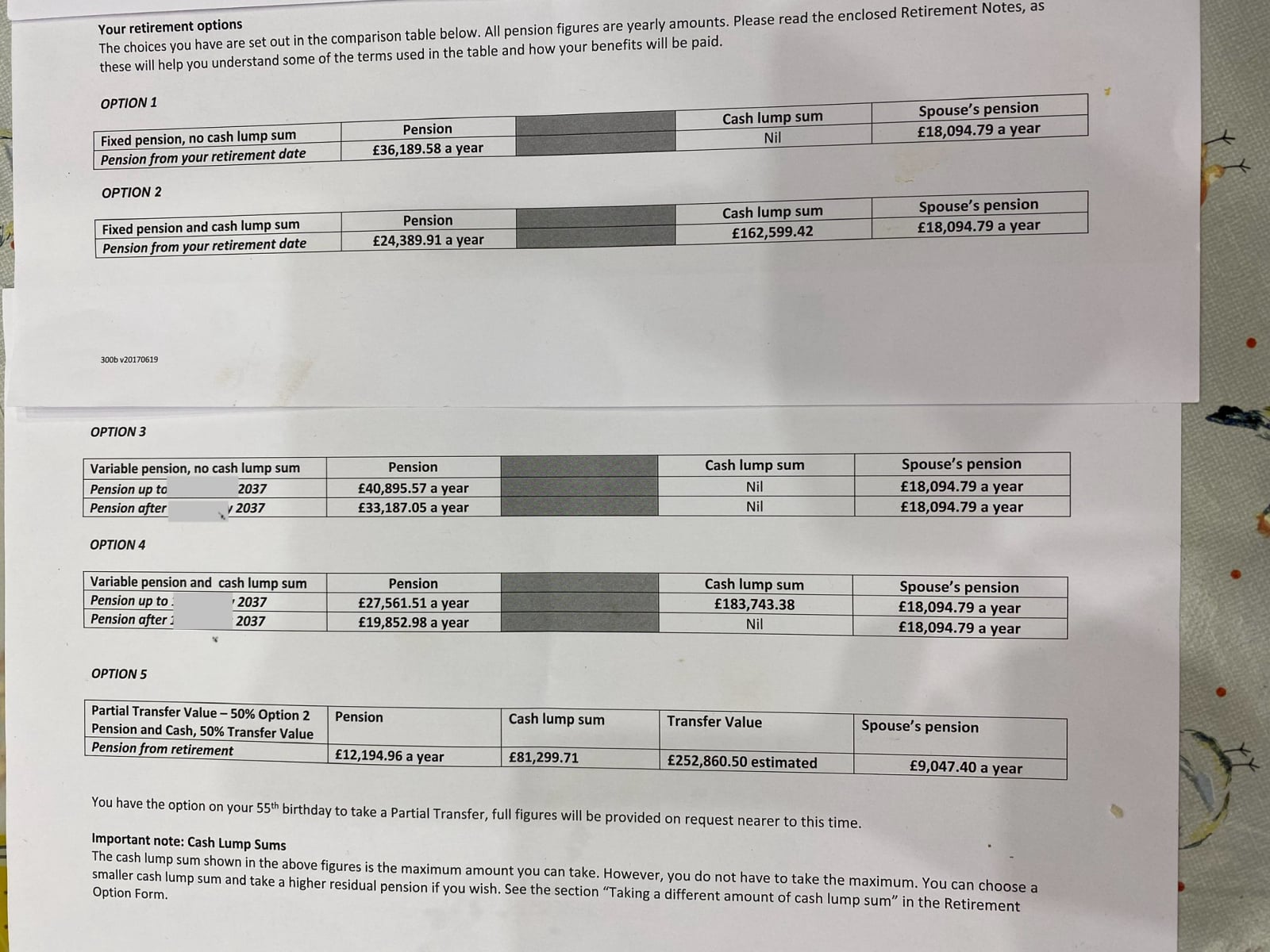

Hi all. My husband was made redundant a few years ago and therefore is entitled to receive his defined benefits pension when he is 55 in the new year. We’ve received the different options as to how to split a lump sum and the annual payments etc. one of the options is a Variable Option, in which you receive a higher pension from 55 to 67, and then it reduces with the state pension making up the difference. However, this option comes with a warning that this May result in a tax bill as you may exceed your annual pension allowance. My husband has not worked since September 2020 so has not paid any money in to his pension since then. We would like to go with this option but how can we work out what the likely tax bill will be? Also why would this option incur tax when the fixed annnual pension option doesn’t? Can anyone help clarify this? Thanks

0

Comments

-

However, this option comes with a warning that this May result in a tax bill as you may exceed your annual pension allowance

Are you sure that is exactly what it said ? Did it maybe say annual personal allowance ?1 -

Not sure I follow. Just sounds like a bridging pension which are pretty common these days. Designed to smooth the income taking the state pension into account.What is his projected DB pension at 55-67 and then from 67?

If he isn’t working he’ll have the standard tax allowance and then pay 20% on anything over that, unless it is over the 40% bracket.1 -

There are no special tax rules in play because it is a variable option. For each option you have been given, just apply the normal tax allowances as usual. So no tax below £12,570/ annum; 20% above £12,570 to £50,270 and 40% above £50,270. You are likely to pay more tax on the variable option just because you will get more money per year (at least until 67).

1 -

The issue is that the "pension input amount" (PIA) for a DB pension is worked out using a formula of 16x the increase in the annual pension value, after accounting for inflation. It's not based on the actuarial value of the pension. So although taking an initially higher pension which drops at state pension age will likely be actuarily the same (ie cost the scheme the same assuming average life expectancy etc), the increase in the initial annual pension could mean there could be a substantial PIA in the year you decide to do this.

This is quite a complicated area and there is a deferred member's carve-out, but not sure it would apply as the increase is probably bigger than allowed. The scheme should be able to give you an estimate of the likely PIA taking this option would generate. But he is likely to have substantial carry forwards available if he's not worked since 2020, so may have enough.

Some in-depth stuff here

PTM053900 - Annual allowance: pension input amounts: deferred members: contents - HMRC internal manual - GOV.UK

But really you need to ask the scheme what PIA taking this option would generate. They should give you a value. Then use a carry forwards calculator like this one:

Unused Pension Carry Forward & Annual Allowance Calculator | HL

If he's not worked and not contributed to any pension since April 2021 he should have £200k of AA available, so if the uplift is £12.5k or less he'll probably be OK. Assuming he's not triggered the MPAA (eg taken taxable income from a DC pension eg SIPP - google "MPAA triggers" if you think this may apply).

4 -

From the handbook of a scheme that offers a bridging option: "The temporary increase in Scheme pension counts as extra pension for the Annual Allowance limit... to calculate the amount that counts towards the Annual Allowance as a result of taking this option, the temporary increase to your Scheme pension needs to be multiplied by a factor of 16".

If there is nothing in the information you have been provided, I suggest you contact the Trustees/Scheme Admin to confirm whether/how this applies in your instance.3 -

Thank you all, this has given some clarity as we couldn’t work out why the bridging pension impacted the annual allowance when the fixed one didn’t. I’ve added a photograph of our 4 options, so what we need to do next is ask the provider for the PIA so we can work out the likely tax charge. My husband has been a stay at home Dad since September 2020 and will not return to employment so that does mean he will keep rolling over his pension allowance each year? And therefore any tax charge is likely very low?

0

0 -

I think you'll be OK, I can't see there being any tax charge as the difference between the fixed and variable is under £5k, so the PIA should be under £80k and he should have £200k available AA inc carry forwards.

(BTW you might read rubbish online like "you can't use carry forwards if you earn under £60k" or "the AA is the lower of your earnings and £60k". Ignore, it's complete rubbish. It's people mixing the tax relief limit with the AA, there is no tax relief here so that limit is not relevant, only the AA, and there's nothing in the AA rules saying you can't use carry forwards if you're a low/zero earner. You just need to be a member of a pension scheme in those years you're carrying forwards from, which he clearly was).

3 -

Thank you so much!zagfles said:I think you'll be OK, I can't see there being any tax charge as the difference between the fixed and variable is under £5k, so the PIA should be under £80k and he should have £200k available AA inc carry forwards.

(BTW you might read rubbish online like "you can't use carry forwards if you earn under £60k" or "the AA is the lower of your earnings and £60k". Ignore, it's complete rubbish. It's people mixing the tax relief limit with the AA, there is no tax relief here so that limit is not relevant, only the AA, and there's nothing in the AA rules saying you can't use carry forwards if you're a low/zero earner. You just need to be a member of a pension scheme in those years you're carrying forwards from, which he clearly was).0 -

Thank you for clarifying that, it’s very helpful. I’m in an almost identical situation to the original posters husband.zagfles said:I think you'll be OK, I can't see there being any tax charge as the difference between the fixed and variable is under £5k, so the PIA should be under £80k and he should have £200k available AA inc carry forwards.

(BTW you might read rubbish online like "you can't use carry forwards if you earn under £60k" or "the AA is the lower of your earnings and £60k". Ignore, it's complete rubbish. It's people mixing the tax relief limit with the AA, there is no tax relief here so that limit is not relevant, only the AA, and there's nothing in the AA rules saying you can't use carry forwards if you're a low/zero earner. You just need to be a member of a pension scheme in those years you're carrying forwards from, which he clearly was).

May I ask, if I did slightly edge over the 60k allowance, would HMRC automatically apply any carry forwards or would I need to raise it with them?0 -

I was surprised to find that you don’t have to formally tell HMRC that you are exceeding the AA, you just need to be confident you have carry forward to cover this in case they query it.Fatboy_McSpeed said:

Thank you for clarifying that, it’s very helpful. I’m in an almost identical situation to the original posters husband.zagfles said:I think you'll be OK, I can't see there being any tax charge as the difference between the fixed and variable is under £5k, so the PIA should be under £80k and he should have £200k available AA inc carry forwards.

(BTW you might read rubbish online like "you can't use carry forwards if you earn under £60k" or "the AA is the lower of your earnings and £60k". Ignore, it's complete rubbish. It's people mixing the tax relief limit with the AA, there is no tax relief here so that limit is not relevant, only the AA, and there's nothing in the AA rules saying you can't use carry forwards if you're a low/zero earner. You just need to be a member of a pension scheme in those years you're carrying forwards from, which he clearly was).

May I ask, if I did slightly edge over the 60k allowance, would HMRC automatically apply any carry forwards or would I need to raise it with them?Fashion on the Ration

2024 - 43/66 coupons used, carry forward 23

2025 - 62/891

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards