We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

We're aware that some users are currently experiencing errors on the Forum. Our tech team is working to resolve the issue. Thanks for your patience.

Should I buy these 4 pre 2016 vol NIC years?

Cheeznmite

Posts: 12 Forumite

Just after some advice please…

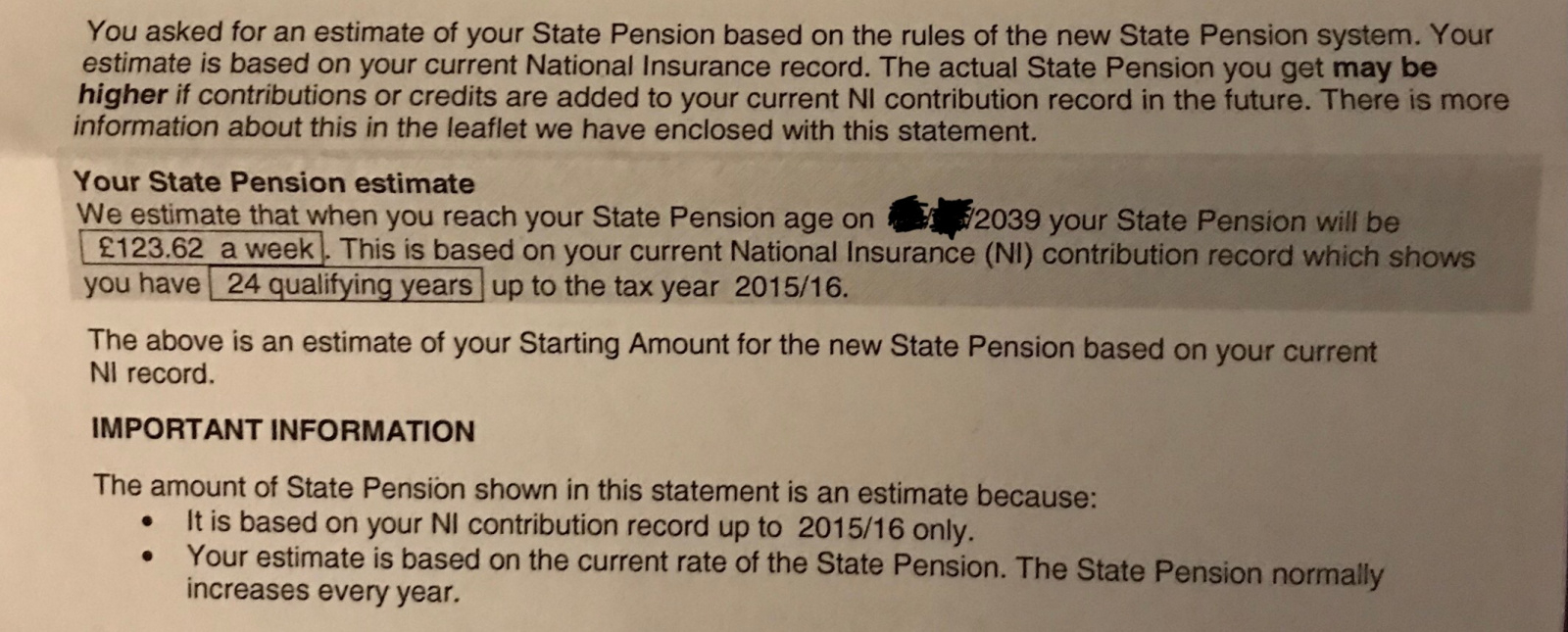

Paid 24 full yrs NIC from 1988-2012 but none since.

State Pension Statement in 2016 estimated my Starting Amount at £123.62/week back then.

No COPE.

Paid 24 full yrs NIC from 1988-2012 but none since.

State Pension Statement in 2016 estimated my Starting Amount at £123.62/week back then.

No COPE.

I can buy all 11 years from 2012/13 to 2022/23 to get 35 total. HMRC sent me a Schedule.

Would buying the 4 before 2016 do anything for my starting amount? Should I just get ones since 2016 and then worry about getting more later?

With April 2025 looming I am keen to send off a cheque to HMRC. I have no current passport/photo ID just paper driving license & birth certificate, so haven’t been able to set up the digital route. Pay as you go mobile too so hanging on the phone is pricey.

I have read lots of helpful replies on here so I thought I would ask! Thanks.

Would buying the 4 before 2016 do anything for my starting amount? Should I just get ones since 2016 and then worry about getting more later?

With April 2025 looming I am keen to send off a cheque to HMRC. I have no current passport/photo ID just paper driving license & birth certificate, so haven’t been able to set up the digital route. Pay as you go mobile too so hanging on the phone is pricey.

I have read lots of helpful replies on here so I thought I would ask! Thanks.

0

Comments

-

What relevance do you think 35 years has?

Have you got your current amount accrued?0 -

Assuming that amount is post April 2016, what exactly does it state, I make your current amount £175.68 so needing another 8 years to reach the full amount. Your starting amount was based on the old rules so any pre 2016 years will add £5.65 each as against £6.32 for a post 2016 year. 7 post 2016 years would leave you £1.28 short, 4 pre + 3 post would leave you £3.95 short so if those pre 2016 years are cheaper it may be worth it, you will need to work out the cost / benefit of either option.

1 -

Is it not 35 years of NI contributions you need to get the full weekly pension amount?

Do you mean current amount of National Insurance contributions?0 -

Only if you start accruing NI credits post 2016, there are numerous topics on this and every time ML mentions 35 it confuses hundreds of thousands.Cheeznmite said:Is it not 35 years of NI contributions you need to get the full weekly pension amount?

Do you mean current amount of National Insurance contributions?

I was born in 1959 and needed over 48 as I was contracted out most of my working life.

0 -

Cheeznmite said:Is it not 35 years of NI contributions you need to get the full weekly pension amount?

No - 35 years only applies to those born this century, whose working lives will fall entirely under the new State Pension scheme. The rest of us are under transitional rules and may need more or less depending on our individual NI records - some as few as 29, others as many as 50.

I suspect that Dazed means the actual value of your pension accrued to date - easy to get if you can get online, but you say you can't get past the id checks in which case you'll need to complete a paper form and post it.Cheeznmite said:Do you mean current amount of National Insurance contributions?

Check your State Pension forecast - GOV.UK

(As an aside, you are going to find it more and more difficult to get things done these days without some form of recognised photo-id, so converting your old paper driving licence to a photo one may be well worth doing).1 -

Thank you all for your replies. This is my first ever forum post so this is new for me.Poohsticks - I was planning to send off my driving license next thing! As few as 29 years? I didn’t realise that!

Molerat - thanks for crunching the numbers (I hoped you would!) Please see statement pic below. I figured I would be on about 79% of a full weekly payment and got £175.68 but couldn’t figure the rest. All the years are £824.20 each to buy except for 2020/21 and 2021/22.

I appreciate lots of people older than me are having to pay NI for all different numbers of years to get the full amount of state pension and those born after 2016 need minimum 10 maximum 35. I am 52 so somewhere in the middle, just trying to get my head round what it means for me. 0

0 -

When was that letter generated?Cheeznmite said:Thank you all for your replies. This is my first ever forum post so this is new for me.Poohsticks - I was planning to send off my driving license next thing! As few as 29 years? I didn’t realise that!

Molerat - thanks for crunching the numbers (I hoped you would!) Please see statement pic below. I figured I would be on about 79% of a full weekly payment and got £175.68 but couldn’t figure the rest. All the years are £824.20 each to buy except for 2020/21 and 2021/22.

I appreciate lots of people older than me are having to pay NI for all different numbers of years to get the full amount of state pension and those born after 2016 need minimum 10 maximum 35. I am 52 so somewhere in the middle, just trying to get my head round what it means for me.

0 -

That was back in August 2016 after they brought in the new pension rules. I sent off a BR19 form to DWP.0

-

I see you have started your own thread…thank you and cheerio!ni_formular said:Out of interest re Class 2 payments, can i only go back 6 years?

Can those that were self-employed, e.g 2006-2016, fill any gaps needed back to 2006? and pay at the class 2 rate? I have had read other posts and used that information to say i can, but after 3 attempts to put my case HMRC say NO. The last adviser did say a i could write a letter to them but that could take months to get any reply, leaving me in limbo or having to pay at class 3 rate now.0 -

To reach the full amount you need 8 more years, get a new forecast to confirm. You have 14 (maybe 15 as you blanked out the month) to get there so paying back years may not be cost effective at the moment, you could pay that £6K today and get hit by a bus tomorrow. Also in the future you may be entitled to benefits that will fill years or maybe there are grandchildren you could be looking after, a good source of freebie years. I would be tempted to put that money away in a high interest account and consider starting to buy those 8 years around 2030. The price increases with inflation each year and you can buy years at the in year price for 2 years after the end of the year so for instance 2030-31 does not need to be purchased until just before April 2033. Yes it is not going to be as cheap as buying these £800ish years now but the additional cost (offset by interest) could be considered an insurance premium against losing the money by popping off too early - voluntary NI is like a reverse life insurance, you only collect if you live long enough

") 1

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards