We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Should I Start paying into my more recent work based pension instead?

textbook

Posts: 893 Forumite

When I left my first job in 2016 I carried on paying into it but believe the pension investments are based 2016 situation so I've been paying into a pension based on advice which hasn't changed since 2016 now I've just lost my most recent job and I also had a work-based pension there and I'm guessing the financial advice for that pension is going to be better because it's more up-to-date. Should I switch from my old pension all my money to this new pension because the financial advice is going to be more up-to-date ?

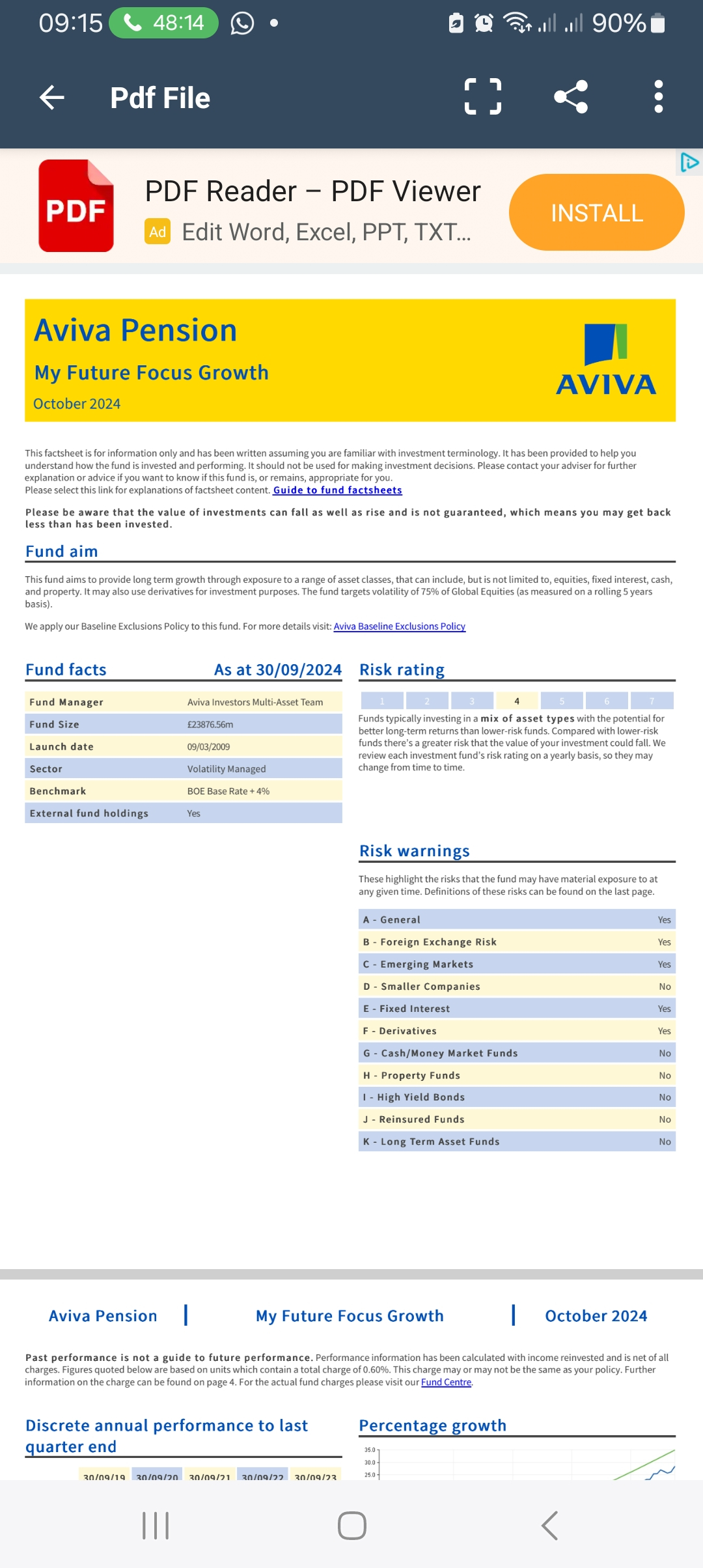

I've attached my old pension info

0

Comments

-

The fund looks to me like a reasonable modern mixed asset pension fund. I dont believe the advice for long term investing would be very different from that in 2016. The fund's performance for example is rather better than the similar risk but perhaps better known Vanguard LifeStrategy 80 fund

One thing confuses me is that you say you are still paying into it. I assume this was an employer's pension scheme but normally new contributions would cease when you left employment.0 -

'Financial advice' is a defined term, covering personalised advice given by a regulated person, so if you want financial advice then you'd need to commission it and pay for it. If you're simply wondering whether one investment is better than another for your requirements, then you might get some guidance (not advice!) on here but you'd need to share more information about what those requirements are, as well as the investments involved.textbook said:When I left my first job in 2016 I carried on paying into it but believe the pension investments are based 2016 situation so I've been paying into a pension based on advice which hasn't changed since 2016 now I've just lost my most recent job and I also had a work-based pension there and I'm guessing the financial advice for that pension is going to be better because it's more up-to-date. Should I switch from my old pension all my money to this new pension because the financial advice is going to be more up-to-date ?0 -

I’ve had a couple of workplace pensions, the default fund each was invested in was probably the best option (from a limited range) for the majority of future pensioners. But that doesn’t mean each person has been reviewed/advised, nor that the fund(s) are the optimum choice for every individual.

I still track how these former funds perform, even though I’ve now got my pot in a self-invested pension, and I think they’re better than I realised. I’m doing okay by myself but the trade off is that I’m in more risky and hence volatile funds.Fashion on the Ration

2024 - 43/66 coupons used, carry forward 23

2025 - 62/890 -

Certain types of workplace DC pension, ( Group Personal Pensions schemes for one) come with you when you leave the company. So effectively they become just another personal pension, although often with the benefit of lower charges that the employer negotiated. You can normally add new contributions to these pensions.Linton said:The fund looks to me like a reasonable modern mixed asset pension fund. I dont believe the advice for long term investing would be very different from that in 2016. The fund's performance for example is rather better than the similar risk but perhaps better known Vanguard LifeStrategy 80 fund

One thing confuses me is that you say you are still paying into it. I assume this was an employer's pension scheme but normally new contributions would cease when you left employment.1 -

I have mine in the Risk 4 out of 7 default fund. I'm 57 and will be wanting the money soon though. Were I 40 or so I'd have it in the Risk 6 out of 7.0

-

I'm 50. So if my fund looks quite safe, shall I just carry on paying into it (like ive been as a self employed person for years) and avoid expensive financial advisors?MetaPhysical said:I have mine in the Risk 4 out of 7 default fund. I'm 57 and will be wanting the money soon though. Were I 40 or so I'd have it in the Risk 6 out of 7.0 -

I have Aviva work place pensions too, all at default 4/7 risk, I’m 40 and as above am deliberating about upping the risk for the next decade before reducing it again

who’s best places to get such advice from? I’ve spoken the Aviva but they were pretty useless, an independent financial advisor or a specialist pensions advisor?

also I have three pensions with Aviva all have different retirement ages not sure the impact of this, again Aviva we’re little help in this0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.8K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 246.9K Work, Benefits & Business

- 603.4K Mortgages, Homes & Bills

- 178.2K Life & Family

- 261K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards