We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

State Pension, buying back missing years, restricted to 2006-2016?

My wife was born April 15 1965 and is due to receive her pension in 2032 at the age of 67.

She has received her pension forecast which states she is 4 years short of full pension and has 3 payable gaps, for

2020-21

2021-22

2022-23

We haven't been told why this is, her N.I. contribs were paid from 1982 until she retired from full time in 2020. We can only assume it's because she was contracted out of SERPS

However according to the information here:

https://www.moneysavingexpert.com/savings/voluntary-national-insurance-contributions/

"You've got until 5 April 2025 to buy back any missing National Insurance years from 2006 to 2016"

Does this mean her unpaid years 20-23 can't be bought back?

Comments

-

No - the current rules say that you can always buy back the most recent six tax years - which include the years your wife is missing.

When the new state pension was introduced in 2016 it included a new limit that State Pension was only payable to those with at least ten full years NI contributions, and so there was a (not so) temporary change to allow people to buy years further back, as far as 2006. The window to buy back these years closes on 5th April 2025.

1 -

The reference to 2006 to 2016 is a special extra ability to catch up because of the 2016 changes. The normal rule still applies though that you can pay the preceding 6 years, so all of those can still be paid. 20/21 may be a cheap one if she is part paid. 22/23 she can still pay at the then rate as it's less than two years past the end of the tax year. 21/22 would now be at the current year price.1

-

We haven't been told why this is,

At 6/4/16, (at which time contracting out ended completely), two calculations were done to establish her starting amount for

NSP .

It was the higher of

Old Rules

NI qualifying years/30 (max) x Full Basic State Pension + ( Additional State Pension - Deduction for Contracting Out).

New Rules

NIQY/35 (max) x Full NSP - (Contracted Out Pension Equivalent).

She would have been in one of three positions.

(a) Starting Amount equal to a Full NSP (£155.65 at that time).

(b) Starting Amount more than a Full NSP (£155.65 at that time).

(c) Starting Amount less than a Full NSP (£155.65 at that time).

She was in position (c)

Her contributions 6/4/16 - 5/4/20 will have improved her forecast but clearly not up to the full amount.She can pay voluntary contributions for 20/21, 21/22/, 22/23 and 23/24.

Check here

https://www.gov.uk/pay-voluntary-class-3-national-insurance/pay-online-state-pension-forecast

1 -

Thank you for all 3 replies, very helpfulCan we assume that the April 2025 deadline doesn't apply as we are talking about the last 6 years?Xylophone, I am still not quite clear:How have her contributions 6/4/16 - 5/4/20 improved her forecast and why those dates specifically?Will we have to pay voluntary contributions every year until she retires or will the voluntary ones for 20/21, 21/22/, 22/23 and 23/24.be sufficient to bring her up to scratch for retirement on full pension? (Assuming no further legislation change)Finally: we will delay paying the extra in the mean time as we believe she can get transferred NI credits for the 2 1/2 years she has just spent looking after grandchildren full time. Hopefully this will make up more than half of the missing years.

0 -

The deadline still applies but as you are only looking at buying years within a period of the last 6 years, it has no impact on you.benawhile said:Thank you for all 3 replies, very helpfulCan we assume that the April 2025 deadline doesn't apply as we are talking about the last 6 years?Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!1 -

Can we assume that the April 2025 deadline doesn't apply as we are talking about the last 6 years?

Yes. Years cost their original price for 2 years after the end of the year then increase to the current year price each year until 6 years after the end of the year when they cease to be available.

How have her contributions 6/4/16 - 5/4/20 improved her forecast and why those dates specifically?The new pension was introduced in April 2016. A line was drawn at that point and you were given the higher of the old or new calculations. You were limited to 30 or 35 years depending on which calculation was used. Contributions for 2016-17 and onwards could then add to that amount, prior year gaps would not add value if you had already hit the relevant limit.Will we have to pay voluntary contributions every year until she retires or will the voluntary ones for 20/21, 21/22/, 22/23 and 23/24.be sufficient to bring her up to scratch for retirement on full pension?The forecast will quote how many years are needed to reach the full amount. It is quite simple to work it out yourself, (£221.20 - current amount achieved) / £6.32. That will likely not give a whole number so you can see how much the final year will give and you can work out if it is worth paying for - multiply £6.32 by the decimal leftover. You do not have to buy any more beyond that point.As long as the person receiving the child benefit is receiving credits from another source then they will be able to transfer the credits - well worth it, MrsM saved around £3K on the class 3 cost.

1 -

ThanksMolerat, I'm somewhat clearer but what does this mean?"prior year gaps would not add value if you had already hit the relevant limit."How can prior year gap add value? Prior to what?

0 -

Years prior to 2016-17 are often available to purchase but may or may not add to the pension amount depending on personal circumstances.

1 -

It seems to be the case that in your wife's case all pre 2016 years are full.

It seems that 16/17,17/18, 18/19 and 19/20 are full.

She has still not reached full NSP (£221.20) but is still under SPA by around seven/eight years.

It seems that she needs four years' contributions/credits to reach the full amount.

She can use years up to the last full tax year before she reaches SPA.1 -

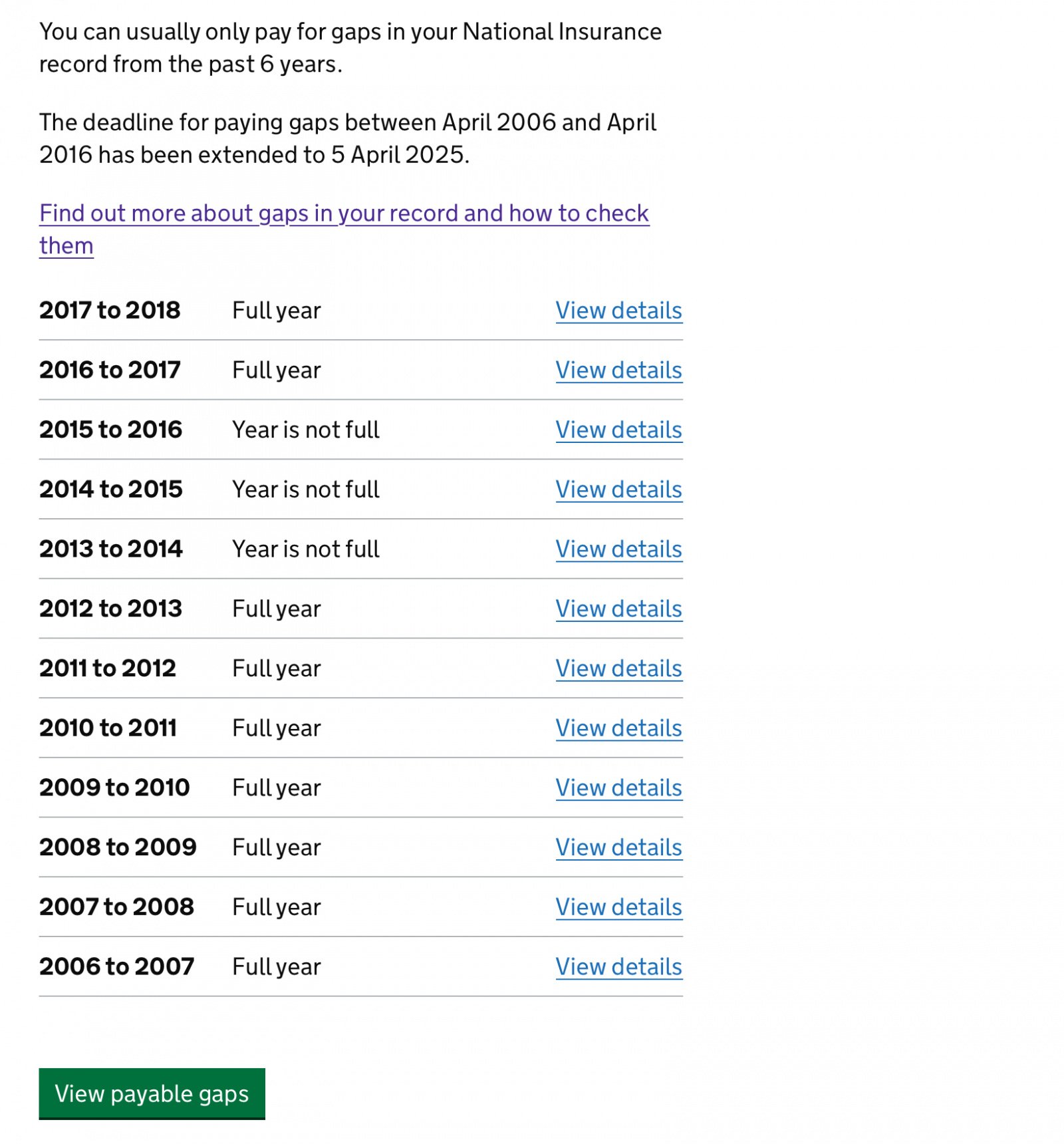

I still receive less than the full pension having already purchased 2 missing years of NI contributions . I have asked why I cannot buy more years as I have a gap, but have been told that I have purchased the maximum due to being contracted out. I asked how I was able to purchase 2 years previously but was told by the operative that she didn’t have the calculations but it would be correct, and that most customers ask this question. Really helpful answer! This is my record showing the 3 missing years previous to the 2 I previously purchased. Anyone shed any light on how this is worked out?

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.9K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.7K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.7K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards