We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

NEST Sharia - changes to fund.

Comments

-

Agreed. However the NEST Shariah fund was presumably intended for people who choose it for religious reasons rather than high performance. In those circumstances it is surely NEST's duty to ensure their limited range of funds is not well outside the mainstream in their allocations,and should perhaps be similar to a fund a responsible IFA would choose for their more naive customers. Note that the performance of Nest's funds is given on their website with no warnings so any employer pension scheme member could well ill-advisedly choose the Shariah fund purely for performance reasons.Ivkoto said:Linton said:

That is a sophisticated investor reasoning. Though if that is your point of view, buying a Shariah fund seems a half hearted approach. Why not go 100% into Scottish Mortgage?Ivkoto said:Linton said:

The problem with the Sharia fund as was is not that it invested 100% in equities but rather that the allocation to different types of equities was skewed towards the higher risk sectors in the market far more than you would normally find with say a global index fund.dlevene said:

Apologies for starting a new thread inappropriately - I did have a look for an existing thread but didn't see one recently (and I only just got the email from them)MSE_ForumTeam5 said:@dlevene - we've merged your post into the ongoing thread on this topic

Clearly there are a number of people in this thread and in other forums that agree with me!It actually makes the fund much more attractive to the average person as it was far too high risk for mainstream provider with limited fund choice.

You are an outlier. Most people would not come close to your risk level and Nest is geared for the mainstream and not outliers.

Being much more strongly geared towards equities is typical for many people earlier on in their career.

That looked fine and would have attracted naive investors during the past few years when tech outperformed everything else but come the next crash there would many complaints when the fund seriously underperformed.

Well the next crash can only be a great news for anyone, who is drip feeding every month ( almost every employee ). Also I doubt there'll be many, who want to be on this fund with less than 5-7 years investment horizont. So the choice of how everyone wants to invest their money must be down to the people, not the pension provider!

When the markets fall 10-20% we get people asking whether they should sell their pension investments or move into bonds for protection.

Nest funds are presumably intended for the general public with virtually no understanding of investment. The danger is that they will buy purely on the last 5 years peformance, should they see it, and be completely out of their depth when the 60% fall happens.

I doubt, that there is a workplace pension provider, which offers SMT as an option")

I don't know the statistics, but pretty sure, that at least 90% of the workers stay in the default fund for their whole working life, because they are not interested in the pensions or they don't know how it works. But it doesn't mean, that the pension providers should not offer more options for some more financially educated people.

People wanting the more exciting funds would be better advised to go to a general platform where if nothing else full information is available.

0 -

There is no more, or less, information on the Sharia fund than the other funds. It’s all laid out pretty clearly and simply.Linton said:

Agreed. However the NEST Shariah fund was presumably intended for people who choose it for religious reasons rather than high performance. In those circumstances it is surely NEST's duty to ensure their limited range of funds is not well outside the mainstream in their allocations,and should perhaps be similar to a fund a responsible IFA would choose for their more naive customers. Note that the performance of Nest's funds is given on their website with no warnings so any employer pension scheme member could well ill-advisedly choose the Shariah fund purely for performance reasons.Ivkoto said:Linton said:

That is a sophisticated investor reasoning. Though if that is your point of view, buying a Shariah fund seems a half hearted approach. Why not go 100% into Scottish Mortgage?Ivkoto said:Linton said:

The problem with the Sharia fund as was is not that it invested 100% in equities but rather that the allocation to different types of equities was skewed towards the higher risk sectors in the market far more than you would normally find with say a global index fund.dlevene said:

Apologies for starting a new thread inappropriately - I did have a look for an existing thread but didn't see one recently (and I only just got the email from them)MSE_ForumTeam5 said:@dlevene - we've merged your post into the ongoing thread on this topic

Clearly there are a number of people in this thread and in other forums that agree with me!It actually makes the fund much more attractive to the average person as it was far too high risk for mainstream provider with limited fund choice.

You are an outlier. Most people would not come close to your risk level and Nest is geared for the mainstream and not outliers.

Being much more strongly geared towards equities is typical for many people earlier on in their career.

That looked fine and would have attracted naive investors during the past few years when tech outperformed everything else but come the next crash there would many complaints when the fund seriously underperformed.

Well the next crash can only be a great news for anyone, who is drip feeding every month ( almost every employee ). Also I doubt there'll be many, who want to be on this fund with less than 5-7 years investment horizont. So the choice of how everyone wants to invest their money must be down to the people, not the pension provider!

When the markets fall 10-20% we get people asking whether they should sell their pension investments or move into bonds for protection.

Nest funds are presumably intended for the general public with virtually no understanding of investment. The danger is that they will buy purely on the last 5 years peformance, should they see it, and be completely out of their depth when the 60% fall happens.

I doubt, that there is a workplace pension provider, which offers SMT as an option

I don't know the statistics, but pretty sure, that at least 90% of the workers stay in the default fund for their whole working life, because they are not interested in the pensions or they don't know how it works. But it doesn't mean, that the pension providers should not offer more options for some more financially educated people.

People wanting the more exciting funds would be better advised to go to a general platform where if nothing else full information is available.

0 -

dunstonh said:

I was around before the dot.com crash and it was very similar to how it is now with people pro tech and tech could do no wrong. So, to me, it does have a Deja Vu feeling to it. However, nothing is ever the same twice in terms of outcomes but we do have a habit of repeating past mistakes.I agree with this completely, the feel is very very similar. And I think we'll see a similar story play out - many companies talking an AI game right now will outright fail. Many of them are charlatans who don't have a hope in hell, others will just fail in a competitive market. However, just like the Internet, AI tech is not going to go away. It's just impossible to know which three companies will be the giants ten years from now!If you had that answer you could become wildly wealthy. Nobody has that answer though, and the people who claim to have it are selling snake oil.0 -

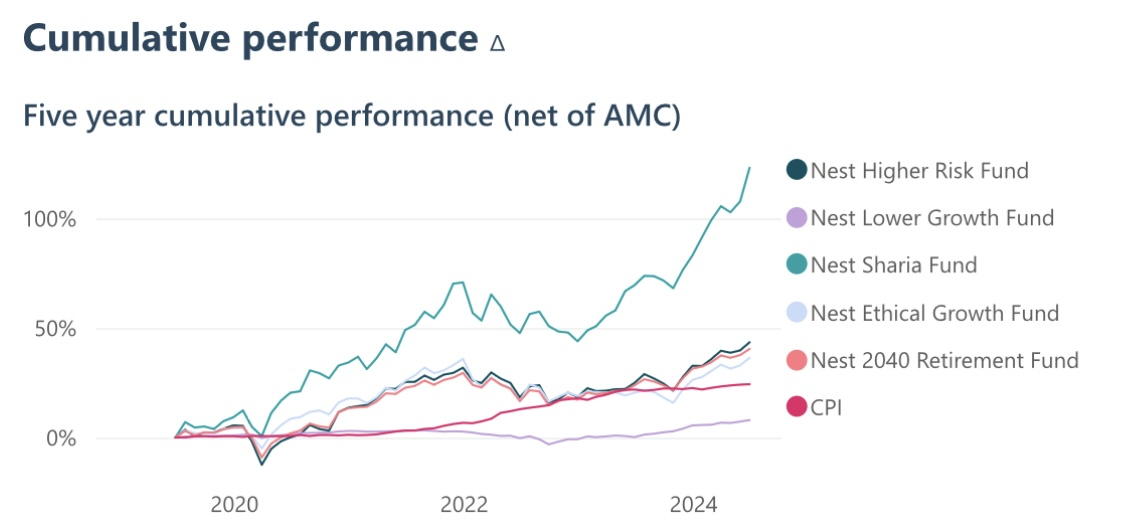

No. The higher risk fund, according to the latest quarterly Nest report, is 68.9% in global equities. The sharia fund is 100% equities and, because it excludes certain sectors, is hugely overweight to the US tech sector. The sharia fund has 37.2% in Microsoft, Apple, Alphabet, Amazon and Meta, whereas HSBC FTSE All World Index has 13.98% in those companies. I've no idea how sukuk works, but something that brings the sharia fund more into line with non-sharia funds looks like very sensible diversification and risk management.monkeys_uncle said:Last time I looked, the 'Higher Risk' fund was about 71% bonds, so it will be interesting to see how that compares with the new Sharia asset allocation.

0 -

Why is it sensible to kill the golden goose in the NEST portfolio of available funds?aroominyork said:

No. The higher risk fund, according to the latest quarterly Nest report, is 68.9% in global equities. The sharia fund is 100% equities and, because it excludes certain sectors, is hugely overweight to the US tech sector. The sharia fund has 37.2% in Microsoft, Apple, Alphabet, Amazon and Meta, whereas HSBC FTSE All World Index has 13.98% in those companies. I've no idea how sukuk works, but something that brings the sharia fund more into line with non-sharia funds looks like very sensible diversification and risk management.monkeys_uncle said:Last time I looked, the 'Higher Risk' fund was about 71% bonds, so it will be interesting to see how that compares with the new Sharia asset allocation.

(I understand your personal risk aversion). 0

0 -

Like most people on here, I am frustrated about the lack of choice with NEST and being now forced to choose between the Sharia and HR funds. I have been in the Sharia fund for the last 3 years and happy with the risk/fund weighting as this sits well with my age to retirement and view on risk.

I have asked NEST to provide the NEW Sharia fund breakdown to show the allocations in the big names, so I can do a comparison to the HR fund. They are a complete shower! Even though they made the change to the 70/30% splits from the 100% equity allocation on the 1st November, they can't tell me (after several simple requests) what the NEW allocation is until the next quarterly report. As I told them, they are investing in it now, so must know the fund breakdown and have a duty to supply the information. How can we be forced to deal with this level of incompetence?1 -

Even though they made the change to the 70/30% splits from the 100% equity allocation on the 1st November, they can't tell me (after several simple requests) what the NEW allocation is until the next quarterly report.Due to the nature of NEST, it works differently to conventional pensions.How can we be forced to deal with this level of incompetence?Its just a very basic option and you are frustrated with the limitations. Its not incompetence.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0 -

The fund is run by HSBC. Their information will be availablerobbie1980 said:Like most people on here, I am frustrated about the lack of choice with NEST and being now forced to choose between the Sharia and HR funds. I have been in the Sharia fund for the last 3 years and happy with the risk/fund weighting as this sits well with my age to retirement and view on risk.

I have asked NEST to provide the NEW Sharia fund breakdown to show the allocations in the big names, so I can do a comparison to the HR fund. They are a complete shower! Even though they made the change to the 70/30% splits from the 100% equity allocation on the 1st November, they can't tell me (after several simple requests) what the NEW allocation is until the next quarterly report. As I told them, they are investing in it now, so must know the fund breakdown and have a duty to supply the information. How can we be forced to deal with this level of incompetence?0 -

I don’t think you will ever get that full fund breakdown. I have scoured online for it; and just can’t find it.robbie1980 said:Like most people on here, I am frustrated about the lack of choice with NEST and being now forced to choose between the Sharia and HR funds. I have been in the Sharia fund for the last 3 years and happy with the risk/fund weighting as this sits well with my age to retirement and view on risk.

I have asked NEST to provide the NEW Sharia fund breakdown to show the allocations in the big names, so I can do a comparison to the HR fund. They are a complete shower! Even though they made the change to the 70/30% splits from the 100% equity allocation on the 1st November, they can't tell me (after several simple requests) what the NEW allocation is until the next quarterly report. As I told them, they are investing in it now, so must know the fund breakdown and have a duty to supply the information. How can we be forced to deal with this level of incompetence?0 -

anyone noticed that Sharia investment seems to have plummeted in the last few weeks?

tried going onto Nest but can't get any data on the fund - just get a "oops something went wrong" message....0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.9K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.7K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.7K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.4K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards