We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

should i take an old DB pension now or leave it?

Comments

-

Firstly, looking at the figures you posted in your original post, the maximum increase appears to have been 5.3%, implying an inflation cap of 5% rather than the 2.5% you've been told (although maybe there are different elements with different inflation increases as you imply in another post).

If you have a spouse/partner does this old pension pay out to a beneficiary on your death (I think 50% is common)?

In terms of comparing whether to hold on or take it now, while the calculations are relatively trivial, making reasonable assumptions is not. For example,

1) You know that in nominal terms the pension will grow by 5% per year + inflation. The inflation element is unknown since future inflation is unknown, and consequently, whether a cap will be applied is also unknown. If you assume inflation of 2% (i.e., the BoE target) then nominal growth will be 7%, while the maximum it can increase by is 10% (assuming a 5% cap or 7.5% assuming a 2.5% cap).

2) Over 5 years, the equivalent pot in a SIPP depends on how it is invested (i.e., equities, bonds, and cash) and could be wildly different. Historically over five year periods the annualised real returns for equities have varied from -13% to 21%, bonds from -17% to 16%, and cash from -11% to 8% (for inflation of 2%, add 2 percentage points to each of these values to get the nominal return).

In other words, trying to guess which would be better over the first 5 years is somewhat tricky.

As others have suggested, looking at potential income at retirement might be a better way.

If you are intending to retire at 65

1) In the first two years, you will have this old DB pension (the real value of which is uncertain because of the inflation cap, but assuming inflation remains below the cap, then £7.2k real if taken at 65) and your current DB pension (£12k) plus whatever income you can derive from savings and DC pensions (for planning purposes, £120k might give you a real income somewhere between £3.5k and £4.0k per year). Roughly a total of £22.7k (you could use more of your savings/SIPP to increase this for 2 years at the expense of long-term income from your SIPP/savings).

2) At 67 you can add in the state pension to this (since no-one has asked have you checked your state pension record - will you receive a full pension?). Roughly, £34.2k in total.

The questions are then, is this income enough for you? Does taking the pension early make much difference to your long-term retirement income? Only you can answer the first question, while I'd suggest that the answer to the second question is 'after 67, not much either way'.

As a secondary consideration, you could consider saving as much as possible into your SIPP over the next five years to improve on the £120k you have there.

1 -

As a general rule it is good to have enough guaranteed income ( like a DB pension + the state pension) to cover your basic needs/expenditure.

Then for your Sipp/ISA etc you can take a bit more risk and it is not a major issue if it has a period of poor performance. You can just rein in your spending a bit.

It is also down to your personality. Some people are scared of investing and prefer as much guaranteed income as possible.

The main thing is not to underestimate the value of guaranteed income, which increases each year, and not to be overconfident about investment returns.2 -

some really interesting comments and observations, thank you everyone. its also helping a financial doofus like me understand my position a little better. ive also been googling and found out how to work out a % increase

"Firstly, looking at the figures you posted in your original post, the maximum increase appears to have been 5.3%, implying an inflation cap of 5% rather than the 2.5% you've been told (although maybe there are different elements with different inflation increases as you imply in another post)."

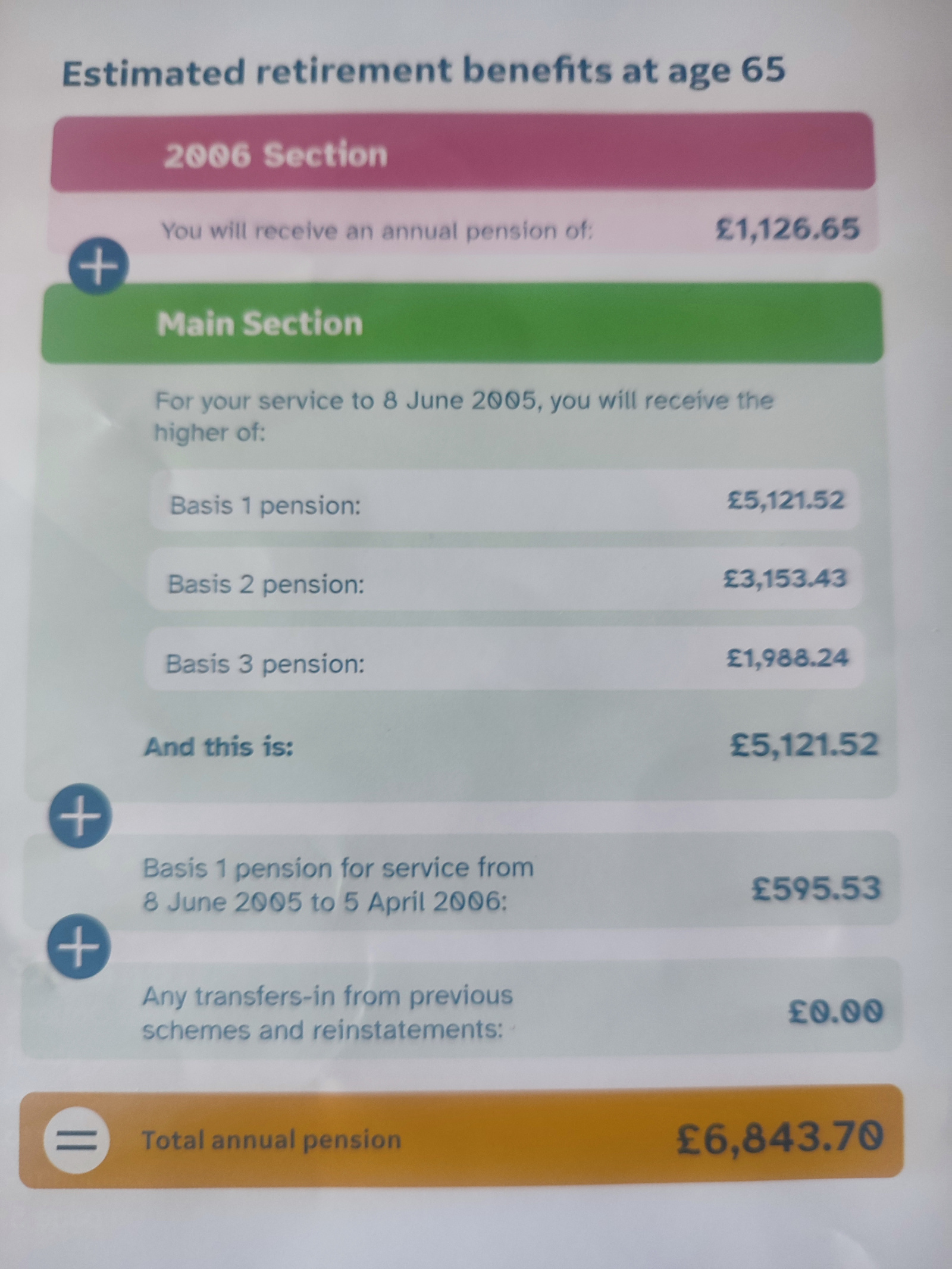

yes, and even tho im understanding it a little better, the different elements are waaaay over my head so i took a photo or two of the terms and conditions. hopefully they may mean something to someone?

this is my confusing statement from last year. im pretty sure theres no personal details included so i feel safe enough to post.

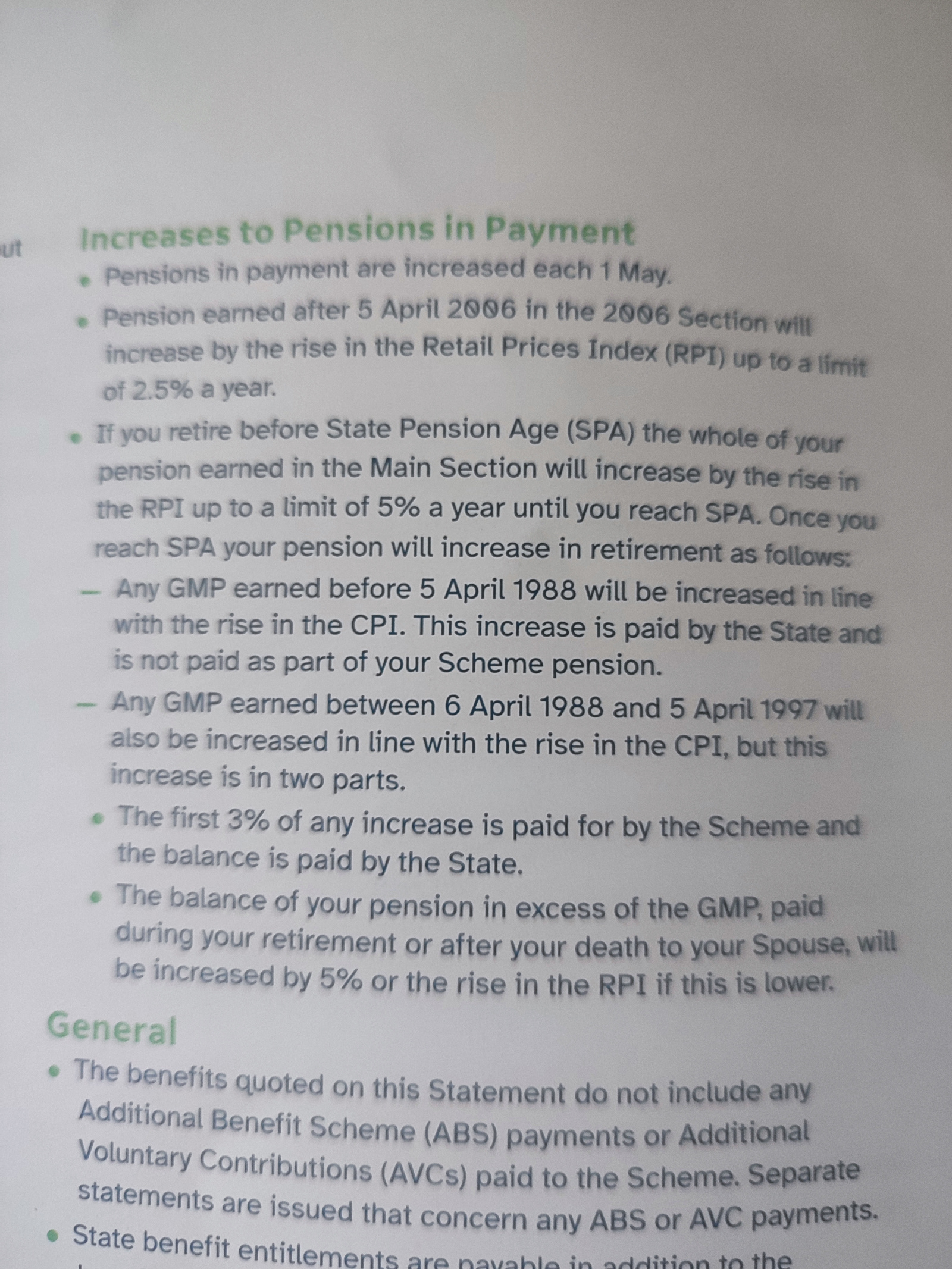

aaaand, the terms and conditions explaining the potential increases.

and if that wasnt enough......

"If you have a spouse/partner does this old pension pay out to a beneficiary on your death (I think 50% is common)? "

its not clear to me. probably. but one part of it is decreased if my wife is more than 10 years younger than me. shes 10 years and 3 months younger

"1) You know that in nominal terms the pension will grow by 5% per year + inflation."

does it? since googling how to calculate the increase, it looks like the last 5 years have seen a growth of 2.53%, 1.39%, 5.01%, 5.34% and 5.21%. so yes, 5% last few years but has been as low as 1.39?

"2) Over 5 years, the equivalent pot in a SIPP depends on how it is invested (i.e., equities, bonds, and cash) and could be wildly different. Historically over five year periods the annualised real returns for equities have varied from -13% to 21%, bonds from -17% to 16%, and cash from -11% to 8% (for inflation of 2%, add 2 percentage points to each of these values to get the nominal return)."

at home now, so just had a look. my SIPP looks to be 7 years old and in that time has grown from £80,000 to £130,000 (50%+). its a mix of 6 different 'funds', with only scottish mortgage losing me money.

i have to go out now so will answer the other comments when i get chance. once again, than you very much for your time and expertise.1 -

Well I recognise the graphics on your statements from my OH’s

") Fashion on the Ration

Fashion on the Ration

2024 - 43/66 coupons used, carry forward 23

2025 - 62/890 -

contd......

"If you are intending to retire at 65

1) In the first two years, you will have this old DB pension (the real value of which is uncertain because of the inflation cap, but assuming inflation remains below the cap, then £7.2k real if taken at 65) and your current DB pension (£12k) plus whatever income you can derive from savings and DC pensions (for planning purposes, £120k might give you a real income somewhere between £3.5k and £4.0k per year). Roughly a total of £22.7k (you could use more of your savings/SIPP to increase this for 2 years at the expense of long-term income from your SIPP/savings).

2) At 67 you can add in the state pension to this (since no-one has asked have you checked your state pension record - will you receive a full pension?). Roughly, £34.2k in total."

yes, i feel ill be in a better place at 67 when the SP kicks in, although still not to the standard of living i currently have, but i suppose thats to be expected. my 120k SIPP pot (actually 130k now ive just checked)....... you say it may give a real income of 3.5- 4k pa. is that because youre including tax (which of course i need to consider). i ask as im sure i keep reading taking 4% per year is probably the figure that will keep it going 'indefinitely'. i suppose thats a side issue anyway, i need to concentrate right now on what to do with THIS old pension :-)

and yes, ive checked my SP details. i contracted out for a few years back in the day, that amound was amalgamated into my SIPP. importantly, my SP says i get the most i can ever get, so theres nothing i can do further to it.

"The questions are then, is this income enough for you? Does taking the pension early make much difference to your long-term retirement income? Only you can answer the first question, while I'd suggest that the answer to the second question is 'after 67, not much either way'."

the first answer is no, its probably not. not if i want to continue my current 'holiday abroad' situation :-) we live pretty frugally anyway, cheap phones, no tv subs, battered old A to B car, our expensive spends are greece twice a year, we live for our holidays. i realise ill have to cut my cloth tho. the second answer ties into it really, i wouldnt take it early to have more money NOW, i do want to maximise my 'medium term' money available (65-80?), hence its simply a question of 'will taking it early give me more return by investing it than leaving it in for 5 more years?'

"As a secondary consideration, you could consider saving as much as possible into your SIPP over the next five years to improve on the £120k you have there."

a very pertinent suggestion, as ive been meaning to do this for some time, but have procrastinated too long as i dont actually know how to do this effectively. firstly, SIPP or ISA? secondly, once thats decided, how do i actually do it? as its invested in S&S. im not sure the most cost-effective way of investing it. if i chuck it into HL the i assume it sits there awaiting my instruction. do i just say to HL please spread all payments over all 6 'funds'? do i do 1 fund one month then another the next month? is it the same if i put it into my ISA? i suppose this warrants a separate thread :-)

"As a general rule it is good to have enough guaranteed income ( like a DB pension + the state pension) to cover your basic needs/expenditure.

Then for your Sipp/ISA etc you can take a bit more risk and it is not a major issue if it has a period of poor performance. You can just rein in your spending a bit."

thats a very good rule of thumb and makes total sense.

thanks everyone, i really appreciate your time and knowledge.0 -

firstly, SIPP or ISA?Assuming you are a basic rate payer now and will be when you come to take funds out then a SIPP currently beats an ISA by 6.25% and you can normally select the same investments in a SIPP as you can in a (S&S) ISA.

Money you add to an ISA can subsequently be taken out tax free. So, ignoring investment growth and fees, if you add £100 then when you come to take it back out you have £100.

But if you add £100 to a SIPP the pension company will add 25% in basic rate tax relief, giving you a pension fund of £125.

When you come to take that £125 out of the pension 25% (£31.25) is a TFLS and the remaining 75% (£93.75) is taxed. £93.75 less basic rate tax is £75.00.

So the total received from the SIPP, after tax, is £106.25 (£31.25 + £75.00).

Personally I'm yet to be convinced that taking your DB pension early is the right choice but if, irrespective of that, you try to add more to your future retirement funds then a SIPP will beat an ISA.

0 -

That's a fun set of terms and conditions (I've snipped the figures to save a bit of screen space). If I'm correct thensadexpunk said:some really interesting comments and observations, thank you everyone. its also helping a financial doofus like me understand my position a little better. ive also been googling and found out how to work out a % increase

"Firstly, looking at the figures you posted in your original post, the maximum increase appears to have been 5.3%, implying an inflation cap of 5% rather than the 2.5% you've been told (although maybe there are different elements with different inflation increases as you imply in another post)."

yes, and even tho im understanding it a little better, the different elements are waaaay over my head so i took a photo or two of the terms and conditions. hopefully they may mean something to someone?

this is my confusing statement from last year. im pretty sure theres no personal details included so i feel safe enough to post.

aaaand, the terms and conditions explaining the potential increases.

and if that wasnt enough......

"If you have a spouse/partner does this old pension pay out to a beneficiary on your death (I think 50% is common)? "

its not clear to me. probably. but one part of it is decreased if my wife is more than 10 years younger than me. shes 10 years and 3 months younger

"1) You know that in nominal terms the pension will grow by 5% per year + inflation."

does it? since googling how to calculate the increase, it looks like the last 5 years have seen a growth of 2.53%, 1.39%, 5.01%, 5.34% and 5.21%. so yes, 5% last few years but has been as low as 1.39?

"2) Over 5 years, the equivalent pot in a SIPP depends on how it is invested (i.e., equities, bonds, and cash) and could be wildly different. Historically over five year periods the annualised real returns for equities have varied from -13% to 21%, bonds from -17% to 16%, and cash from -11% to 8% (for inflation of 2%, add 2 percentage points to each of these values to get the nominal return)."

at home now, so just had a look. my SIPP looks to be 7 years old and in that time has grown from £80,000 to £130,000 (50%+). its a mix of 6 different 'funds', with only scottish mortgage losing me money.

i have to go out now so will answer the other comments when i get chance. once again, than you very much for your time and expertise.

While deferred:

1) Your 2006 section increases by CPI capped at 5% (for pre-2009) or 2.5% (post-2009) - I'm guessing that all/most of your service was pre-2009?

2) Since Basis 1 of your Main section pension is the predominant one, then this increases by RPI capped at 5%.

The two different inflations in use confuse the issue, but explains the sequence of increases. Essentially until our recent bout of high inflation it was increasing by a mix of CPI and RPI and while inflation has been high it has increased by about 5% (quite how it has managed slightly more than 5% is a mystery to me).

When you start to take the pension:

1) Your Section 1 pension will increase by RPI capped at 2.5%

2) Your Main section will increase

a) By RPI capped at 5% until you reach state pension age

b) From state pension age, for non-GMP, by RPI capped at 5% and for non-GMP it depends on when your service is.

In other words, some of the increases are better while deferred than they are in payment. An additional complexity in any calculation.

Death benefits

These appear to consist of a lump sum and payment of some of your pension (only the non-GMP Basis 1?). An exact calculation is way beyond my limited expertise, so it is probably worth contacting the scheme to be certain, although others on these boards may have an answer.

Investments

Does the increase in value of your SIPP include new money? Over the last 7 years, equities have done well, e.g. a world index has increased from 100 to 229 (i.e., more than double, roughly 12% annualised returns) while global bonds have essentially stayed at the same value (i.e., roughly 0% annualised returns). You might want to start another thread on suggestions for investments. FWIW, in my view a global equity fund such as HSBC FTSE All world and a global bond fund such as Vanguard Global bond (or the short-term bond version) in some proportion acceptable to you is probably good enough.

0 -

sadexpunk said:contd......

yes, i feel ill be in a better place at 67 when the SP kicks in, although still not to the standard of living i currently have, but i suppose thats to be expected. my 120k SIPP pot (actually 130k now ive just checked)....... you say it may give a real income of 3.5- 4k pa. is that because youre including tax (which of course i need to consider). i ask as im sure i keep reading taking 4% per year is probably the figure that will keep it going 'indefinitely'. i suppose thats a side issue anyway, i need to concentrate right now on what to do with THIS old pension :-)

and yes, ive checked my SP details. i contracted out for a few years back in the day, that amound was amalgamated into my SIPP. importantly, my SP says i get the most i can ever get, so theres nothing i can do further to it.

Without wanting to get sidetracked, the 4% is the historical 'safe' withdrawal rate for US retirees. For the UK, the figure of 3.0% to 3.5%. Either is probably good enough in your case since it doesn't make a lot of difference to your overall income."The questions are then, is this income enough for you? Does taking the pension early make much difference to your long-term retirement income? Only you can answer the first question, while I'd suggest that the answer to the second question is 'after 67, not much either way'."There are some things no longer required in retirement (no NI contributions, no pension contributions, no commuting costs, etc.) that might make it a bit cheaper.

the first answer is no, its probably not. not if i want to continue my current 'holiday abroad' situation :-) we live pretty frugally anyway, cheap phones, no tv subs, battered old A to B car, our expensive spends are greece twice a year, we live for our holidays. i realise ill have to cut my cloth tho. the second answer ties into it really, i wouldnt take it early to have more money NOW, i do want to maximise my 'medium term' money available (65-80?), hence its simply a question of 'will taking it early give me more return by investing it than leaving it in for 5 more years?'

I think I would say your final question is impossible to answer with any certainty. For example, if you took it early and invested it all in equities (probably not a good idea, but bear with), if equities drop by 50% over those 5 years then it would have been best to take the pension late, while if equities increase by 50%, then it would be best take the pension now. Unfortunately, you will not be in a position to know which was best until afterwards. My own view (FWIW), is that in the long-term you are better taking it later for reasons others have stated (i.e., inflation capped guaranteed income is useful to have in retirement)."As a secondary consideration, you could consider saving as much as possible into your SIPP over the next five years to improve on the £120k you have there."I think you're right about a new thread. I'm not familiar with HL (we've used iweb, vanguard, and fidelity), but, with the exception of iweb (which is somewhat 'no frills'), there is usually a way to direct regular contributions to where you want them to go.

a very pertinent suggestion, as ive been meaning to do this for some time, but have procrastinated too long as i dont actually know how to do this effectively. firstly, SIPP or ISA? secondly, once thats decided, how do i actually do it? as its invested in S&S. im not sure the most cost-effective way of investing it. if i chuck it into HL the i assume it sits there awaiting my instruction. do i just say to HL please spread all payments over all 6 'funds'? do i do 1 fund one month then another the next month? is it the same if i put it into my ISA? i suppose this warrants a separate thread :-)

1 -

"Assuming you are a basic rate payer now and will be when you come to take funds out then a SIPP currently beats an ISA by 6.25% and you can normally select the same investments in a SIPP as you can in a (S&S) ISA.

Money you add to an ISA can subsequently be taken out tax free. So, ignoring investment growth and fees, if you add £100 then when you come to take it back out you have £100.

But if you add £100 to a SIPP the pension company will add 25% in basic rate tax relief, giving you a pension fund of £125.

When you come to take that £125 out of the pension 25% (£31.25) is a TFLS and the remaining 75% (£93.75) is taxed. £93.75 less basic rate tax is £75.00.

So the total received from the SIPP, after tax, is £106.25 (£31.25 + £75.00)."

excellent knowledge thank you, the SIPP it is then. just for clarification, does this mean that any withdrawal from SIPP will have a 25% tax free element? indefinitely? not that im going to, and for simplicity's sake say i had a pot of £100,000, could i take out a TFLS of £25,000. and then any further withdrawals of say £2,000 at a time would also see £500 tax free each time? im sure my thinkings flawed there but not 100% sure.

"Personally I'm yet to be convinced that taking your DB pension early is the right choice but if, irrespective of that, you try to add more to your future retirement funds then a SIPP will beat an ISA."

.....is the impression im starting to get. thank you. and obviously nobody knows the future, but at least nobodys telling me "thats a rubbish pension, you need to take it while you can and invest elsewhere". so if its a close call then i'll leave it.

"While deferred:

1) Your 2006 section increases by CPI capped at 5% (for pre-2009) or 2.5% (post-2009) - I'm guessing that all/most of your service was pre-2009?"

all of it. this pension stopped 31st dec 2008 and we were transferred to a DC pension, of which i paid in for a year then moved jobs. that small DC pot is now part of SIPP.

"Does the increase in value of your SIPP include new money? "

no. ironically, the one fund i put in later (scottish mortgage) has actually lost me a few hundred quid, so it would have been better to have not put any more in crystal ball etc.....

"There are some things no longer required in retirement (no NI contributions, no pension contributions, no commuting costs, etc.) that might make it a bit cheaper."

yep, understood. thats why i try to base all my calculations as 'net'. i know what i get in my hand now, and try to work out what would be in my hand in retirement. if i looked at my top line and then my retirement amount then i'd weep

and yes, i think youre right about future investments and how to do this, i'll start a new thread for adding to SIPP, probably through a DD or something. this was purely a question on whether this pensions got a rubbish growth rate or not (lets face it, one year the growth was down to 1.39%) and whether to take it now and invest elsewhere, or leave it as it is. it seems to be weighing in towards leaving it where it is.

cant thank you enough for your time and expertise.0 -

excellent knowledge thank you, the SIPP it is then. just for clarification, does this mean that any withdrawal from SIPP will have a 25% tax free element? indefinitely? not that im going to, and for simplicity's sake say i had a pot of £100,000, could i take out a TFLS of £25,000. and then any further withdrawals of say £2,000 at a time would also see £500 tax free each time? im sure my thinkings flawed there but not 100% sure.There is a cap on the TFLS (including from a DB scheme) but that is currently ~£268k so may well not be a factor unless the rules change.

There are a number of options when it comes to taking money out of a DC pension like a SIPP.

One very common one is UFPLS, where (subject to the cap) 25% of each withdrawal is a TFLS and 75% is taxable income. Like your example.

Another is where you take the full TFLS upfront and then the remaining crystallized pot (including any investment growth) is taxable when taken out of the pension. For example say you have £200k in the SIPP and take the full 25% TFLS upfront, leaving £150k crystallized in the pension for a few years. That £150k grows back to say £185k. When any of that £185k is taken out of the pension it's all taxable income as you took the full 25% TFLS upfront.

There are other options as well.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.8K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards