We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Coming off Stepchange to self manage DMP

I am on one at the moment! Been working at this all yesterday, and I'm absolutely determined to get sorted. I've read all the direct advice I've been given so far and read lots of other threads as well.

I've decided to come off Stepchange and stop paying unsecured debt for both me and my husband, we have a DMP each with them. Then I will negotiate repayment of a HMRC tax debt. I went through all our details today, updating everything in a new spreadsheet. I have 10 creditors owing 5k, 9 of them already defaulted. He has 7 creditors owing 4.5k and 3 are defaulted. We both have vehicle loans to get us to work, public transport not an option here, and I have this tax debt.

So for the 5 creditors that aren't defaulted, I know I should pay nothing until they do. What happens with the already defaulted ones? Some of them I don't know where to pay, Stepchange did it all for me, but once I get the letter with details on, should I pay a token payment until my tax debt is clear?

I'm planning on putting money away from working freelance to do full and final settlements on some of them, or self managing a DMP, or even going back to Stepchange on a joint DMP, once the tax is sorted.

I'm also considering a DRO. I had one 6 years ago in November, but I have a car worth about 5k this time that I still have finance on until next July. I know I have to have less than £75 a month spare, if I stop freelancing then I'll be there. I found confusing advice about my self assessment debt, whether that would be included or not, I thought probably not but some places say yes. Might be worth downsizing my car slightly to do it, although not sure I can both clear the car finance and buy another and I need it to get to work.

Thanks again for any help.

22/08/2024: £25577.87

18/08/2025: £17434.47

Difference: -£8143.40

Percentage of debt paid off: 31%

Diary - A Lifetime of Debt

Comments

-

you won't get a dro with a car worth £5k and not until November anyway. so that's out the picture. wait till it reaches £4k in value

you won't get a dro with a car worth £5k and not until November anyway. so that's out the picture. wait till it reaches £4k in value

and if you are paying only the debts that defaulted that's preferential treatment which isn't allowed all creditors have to be paid equally prorated in last 2 years if applying for a dro.

except maybe HMRC cos that's a priority debt

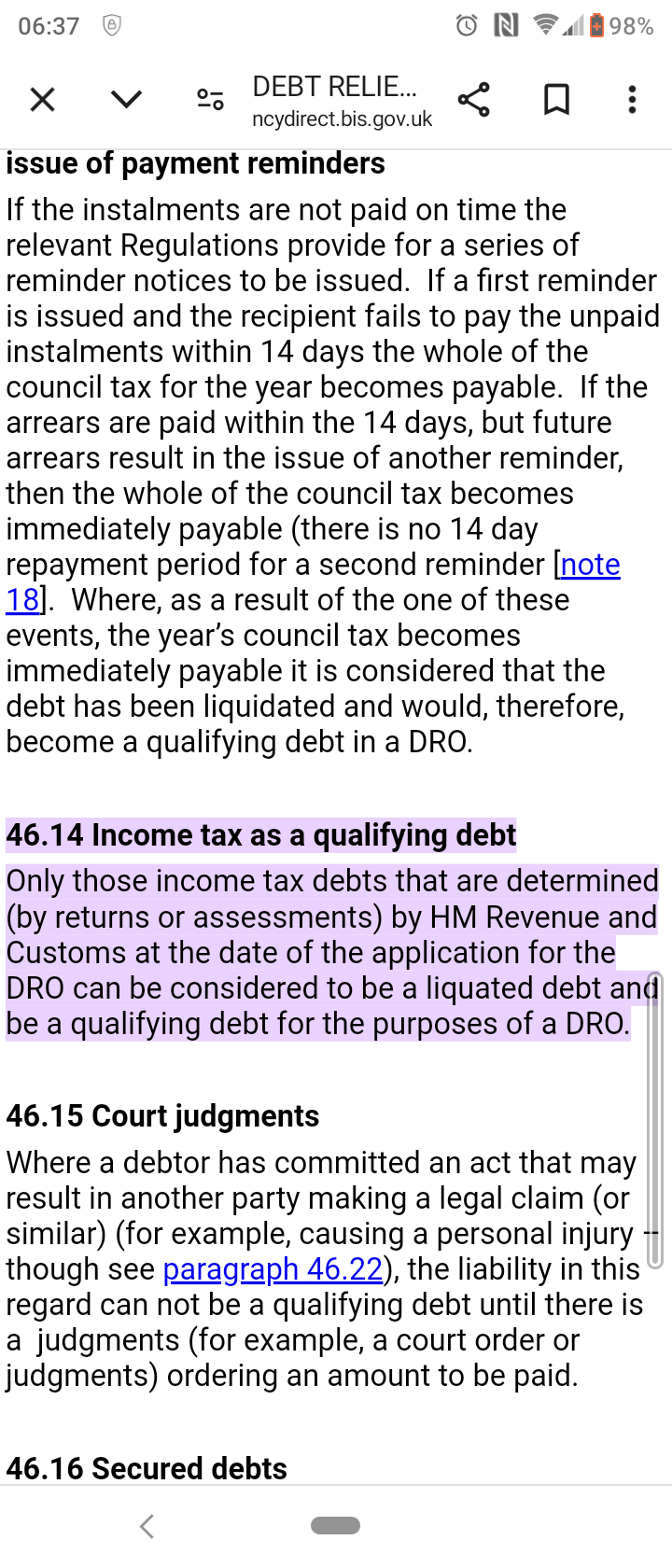

HMRC debt can go in a dro I believe. but HMRC won't wait that long though, till you qualify for a dro

how much you owe HMRC, did stepchange know about the HMRC debt.

debts that have defaulted have the right to take further action against you,

any letters you got from creditors tell you how to pay in the back page of them, look at your letters.

it's also on their websites, pay by standing order, set it up. not direct debit or recurring debit cardChristians Against Poverty solved my debt problem, when all other debt charities failed. Give them a call !! ( You don't have to be a Christian ! )

https://capuk.org/contact-us0 -

could you clear the HMRC debt if you stopped paying all your creditors except car by April next year

your husband can run his own dmp and car payment whilst you just do car and hmrc whilst at same time look out for letters before action in the post from any defaulted creditors

them offer payment to the letter before action creditorsChristians Against Poverty solved my debt problem, when all other debt charities failed. Give them a call !! ( You don't have to be a Christian ! )

https://capuk.org/contact-us0 -

Hi, thanks for responding so early in the AM. That's what I was thinking, I could time the DRO right, my car is in pretty bad shape so it will hit 4k value soon. I'm not sure I understand the prorated bit - do you mean I have to pay all debts equally for 2 years before I apply for a DRO?stu12345_2 said:you won't get a dro with a car worth £5k and not until November anyway. so that's out the picture. wait till it reaches £4k in value

and if you are paying only the debts that defaulted that's preferential treatment which isn't allowed all creditors have to be paid equally prorated in last 2 years if applying for a dro.

HMRC debt can go in a dro I believe.

how much you owe HMRC, did stepchange know about the HMRC debt.

debts that have defaulted have the right to take further action against you,

any letters you got from creditors tell you how to pay in the back page of them, look at your letters.

it's also on their websites, pay by standing order, set it up. not direct debit or recurring debit card

I owe about 6700 to HMRC income tax and NI, child benefit repayments, and student loans. Stepchange don't know about this but I emailed about it yesterday.

I did look through all my creditors and found most I can manage and pay online, just a couple that say call us only and I haven’t had a letter in years as been on Stepchange.Debt owed

22/08/2024: £25577.87

18/08/2025: £17434.47

Difference: -£8143.40

Percentage of debt paid off: 31%

Diary - A Lifetime of Debt0 -

hmrc , child benefit overpayment are priority and must be paid.

student loans only collect once your income hits a certain limit, it can't go into a dro.

all creditors must be paid equally prorata based on how much you owe each one,

in last 2 years, you can't settle one fully via an early full and final offer, and ignore the rest.

or you only pay one and not another in monthly payments .

that's preferential treatment and can block a dro being allowed by the IS

how did you feel about the replies you got on your other thread you did yesterdayChristians Against Poverty solved my debt problem, when all other debt charities failed. Give them a call !! ( You don't have to be a Christian ! )

https://capuk.org/contact-us0 -

Not before April, unless I hammer the freelance work but then I get another big tax bill next year, but maybe by July or August. Yes looking at a HMRC arrangement and our vehicles, then everything else token payments and reduced settlements where I can.stu12345_2 said:could you clear the HMRC debt if you stopped paying all your creditors except car by April next year

your husband can run his own dmp and car payment whilst you just do car and hmrc whilst at same time look out for letters before action in the post from any defaulted creditors

them offer payment to the letter before action creditorsDebt owed

22/08/2024: £25577.87

18/08/2025: £17434.47

Difference: -£8143.40

Percentage of debt paid off: 31%

Diary - A Lifetime of Debt0 -

forget reduced settlements offers if it stops you repaying HMRC by April.

early settlement offers are for those that have lots of spare cash or a relative gives you the money.

you are not in that position

contact HMRC today, not tomorrow or next week,and see what arrangement they will accept.

and has the DWP contacted you about child benefit overpaymentsChristians Against Poverty solved my debt problem, when all other debt charities failed. Give them a call !! ( You don't have to be a Christian ! )

https://capuk.org/contact-us0 -

It's all brilliant advice, and I'm going to contact HMRC to come to an arrangement and stop paying all unsecured debt for now. I'm looking at some tax advice too and I won't take on too much work if it puts me over thresholds from now on, I think I missed out my 1000 trading allowance too so I've updated my return. I think there are other things I'm clueless about too, so I'm learning. Feels great to know it's not worth all the extra work and I should do less, I've been exhausted.stu12345_2 said:hmrc , child benefit overpayment are priority and must be paid.

student loans only collect once your income hits a certain limit, it can't go into a dro.

all creditors must be paid equally in last 2 years, you can't settle one fully via an early full and final offer not cancelled you only pay one and not another in monthly payments .

that's preferential treatment and can block a drop being allowed by the IS

how did you feel about the replies you got on your other thread you did yesterday

Probably DRO not an option then, I'd be sorted much earlier the DMP way.Debt owed

22/08/2024: £25577.87

18/08/2025: £17434.47

Difference: -£8143.40

Percentage of debt paid off: 31%

Diary - A Lifetime of Debt0 -

is the £1000 limit a limit you can earn before it affects benefits?

you may be best posting in benefits or employment forums for advice there about thresholds and child benefit overpayment

but keep your posts clear and conciseChristians Against Poverty solved my debt problem, when all other debt charities failed. Give them a call !! ( You don't have to be a Christian ! )

https://capuk.org/contact-us0 -

You can earn 1000 on top of your job before any income tax is owed, I have gone way over but didn't realise you still include it on your tax return, unless you have more than 1000 deductables. I think I've got that right, I'm still learning and a long way to go. I amended it yesterday and once accepted I'll arrange to pay the new figure. Yep I'm over on the tax forum too bugging them!Debt owed

22/08/2024: £25577.87

18/08/2025: £17434.47

Difference: -£8143.40

Percentage of debt paid off: 31%

Diary - A Lifetime of Debt0 -

It's all in one HMRC debt. I'm hoping I might have spare cash later next year if I can get HMRC cleared and my car paid off, I have small balances across many creditors as well.stu12345_2 said:forget reduced settlements offers if it stops you repaying HMRC by April.

early settlement offers are for those that have lots of spare cash or a relative gives you the money.

you are not in that position

contact HMRC today, not tomorrow or next week,and see what arrangement they will accept.

and has the DWP contacted you about child benefit overpaymentsDebt owed

22/08/2024: £25577.87

18/08/2025: £17434.47

Difference: -£8143.40

Percentage of debt paid off: 31%

Diary - A Lifetime of Debt0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.8K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 246.9K Work, Benefits & Business

- 603.4K Mortgages, Homes & Bills

- 178.2K Life & Family

- 261K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards