We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

DMP 9k owed - Need help

s12c

Posts: 19 Forumite

Hi all,

I am currently on a debt management plan, I'm 29.

My financial situation has occurred due to being stupid with money but also due to some unfortunate circumstances beyond my control.

My personal situation is that I'm not in a relationship, I don't have any family members who I can rely on/answer my calls and my parents are sadly no longer with us. Of course, it goes without saying that there was no inheritance to speak of.

I currently owe £9700 - I've been paying £350 per month.

I have an income of £38,000 per annum - but with student loan and pension contributions mean I take home around £2300 per month. My fixed expenses total £1300 (rent, bills, insurance) and then the DMP is £350 per month and I have £650 for variable costs (food, transport, presents, fees etc)

I don't have any money in savings, I need new furniture (bed) and I'm starting to feel really insecure about it all. I am worried my job will start making cuts as other parts of the organisation are cutting back and I haven't even been there long enough to qualify for statuary redundancy.

I really feel like I'm struggling to pay for things and I want to get a second job. But, the problem is if I declare it, It will be eaten up within the DMP as I can't justify expenses within the budget, but I need to save money because its hurting my mental health to not have it.

What are the risks in doing this? I know it isn't particularly ethical and I recognise that I owe the money and it must be paid - but this is becoming a real source of concern for me.

I don't want to pad the DMP budget because I need to pay it back as soon as possible.

I am also generally higher level of pay jobs. In a previous role, I earned in excess of 50k per year so I believe it could be realistic. But my question in this regard is, what if the money I can offer to the DMP exceeds the contractual minimum payment?

Also, should I consider stop paying pension contributions? I think I have around £26k in pensions savings currently.

I am currently on a debt management plan, I'm 29.

My financial situation has occurred due to being stupid with money but also due to some unfortunate circumstances beyond my control.

My personal situation is that I'm not in a relationship, I don't have any family members who I can rely on/answer my calls and my parents are sadly no longer with us. Of course, it goes without saying that there was no inheritance to speak of.

I currently owe £9700 - I've been paying £350 per month.

I have an income of £38,000 per annum - but with student loan and pension contributions mean I take home around £2300 per month. My fixed expenses total £1300 (rent, bills, insurance) and then the DMP is £350 per month and I have £650 for variable costs (food, transport, presents, fees etc)

I don't have any money in savings, I need new furniture (bed) and I'm starting to feel really insecure about it all. I am worried my job will start making cuts as other parts of the organisation are cutting back and I haven't even been there long enough to qualify for statuary redundancy.

I really feel like I'm struggling to pay for things and I want to get a second job. But, the problem is if I declare it, It will be eaten up within the DMP as I can't justify expenses within the budget, but I need to save money because its hurting my mental health to not have it.

What are the risks in doing this? I know it isn't particularly ethical and I recognise that I owe the money and it must be paid - but this is becoming a real source of concern for me.

I don't want to pad the DMP budget because I need to pay it back as soon as possible.

I am also generally higher level of pay jobs. In a previous role, I earned in excess of 50k per year so I believe it could be realistic. But my question in this regard is, what if the money I can offer to the DMP exceeds the contractual minimum payment?

Also, should I consider stop paying pension contributions? I think I have around £26k in pensions savings currently.

0

Comments

-

Hi, priorities are rent, CT, utilities, travel to work, food, clothing. You should make a monthly allowance for all the things like Christmas and presents, insurance, clothing, medical and dental and an emergency fund.

How much you pay towards your consumer debts depends what you have left. Have all your debts defaulted, or are you getting AP markers? Who is managing your DMP?

If you've have not made a mistake, you've made nothing1 -

I think all of my debts are defaulted and some have transferred to debt management companies.RAS said:Hi, priorities are rent, CT, utilities, travel to work, food, clothing. You should make a monthly allowance for all the things like Christmas and presents, insurance, clothing, medical and dental and an emergency fund.

How much you pay towards your consumer debts depends what you have left. Have all your debts defaulted, or are you getting AP markers? Who is managing your DMP?

Stepchange are managing this for me. I don't know what an AP marker is.

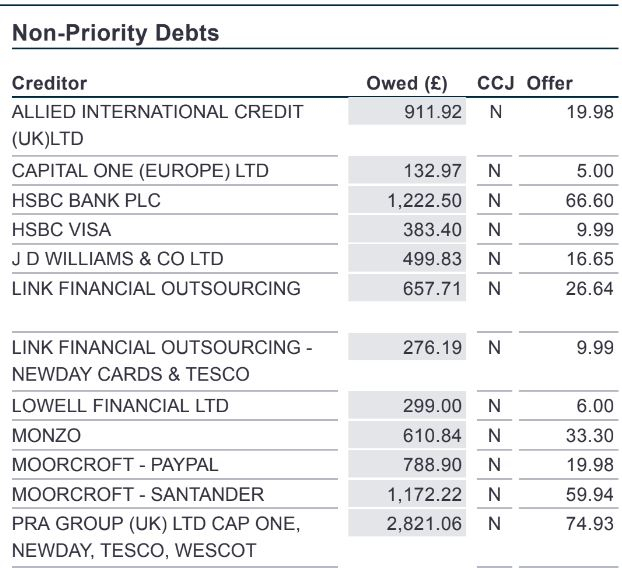

The debt breakdown is as follows:

I don't have any non-consumer debt included in my DMP

I take home around £2300 per month. My fixed expenses total £1300 (rent, bills, insurance) and then the DMP is £350 per month and I have £650 for variable costs (food, transport, presents, fees etc)

0 -

You can change to self managed and tell the companies what you are going to give them without showing the your SOA.Statement of Affairs (SOA) link: https://www.lemonfool.co.uk/financecalculators/soa.phpFor free, non-judgemental debt advice, try: Stepchange or National Debtline. Beware fee charging companies with similar names.0

-

Glad you are with Stepchange as there are others that charge monthly fees.

But you do need to check all three credit records to ensure that the debts are all defaulted.

One of the issues with Stepchange is that they encourage people to sign up quickly, rather than acquiring an emergency fund which helps them weather issues like bergered beds. You can ask them to halt payments for a month or two allow you to pay for repairs and necessary purchases, but it might be better if you'd developed a large enough fund to cover the bed purchase.

When was your last review of income and expenditure?If you've have not made a mistake, you've made nothing0 -

be wary if your debts haven't defaulted( default means Interest, late fees etc can no longer ever be added)and you get pay rise/ second job enough to pay the regular min payment, then you will be considered back to a regular customer that can pay credit debts, even if it's min payment and interest will kick in again.( you are no longer insolvent on min monthly payment credit card debts, I explain)

I was with stepchange and they warned me about that.they normally can stop interest straight away on your debts in a DMP, even before debts have defaulted.

but if your earnings improve and they distribute your dmp monthly amounts pro rata amongst your creditors, there is a chance credit card debts hit the contractual min regular payments.

stepchange pay more of your dmp to payday loans or bank loans per month as the contractual agreement on those is/was higher than credit cards., cos they had an original end dates on the loans

but as credit cards only require a regular customer to pay a min monthly amount , that's why credit card debt is dangerous as the debt could run for years and years on min paymentsChristians Against Poverty solved my debt problem, when all other debt charities failed. Give them a call !! ( You don't have to be a Christian ! )

https://capuk.org/contact-us0 -

My last review was March. I don't think I can pause for a month because I had to do this once already due to a personal situation. I used to have a side job but I've been told its not allowed by my employer due a non-compete clause.RAS said:Glad you are with Stepchange as there are others that charge monthly fees.

But you do need to check all three credit records to ensure that the debts are all defaulted.

One of the issues with Stepchange is that they encourage people to sign up quickly, rather than acquiring an emergency fund which helps them weather issues like bergered beds. You can ask them to halt payments for a month or two allow you to pay for repairs and necessary purchases, but it might be better if you'd developed a large enough fund to cover the bed purchase.

When was your last review of income and expenditure?0 -

This is a completely informal arrangement. You can pause if you need to, or just terminate the deal if you want to manage the debts yourself. How much is in your statement of affairs/budget for emergencies?

I'm also a bit surprised you are renting and have to provide you own bed. Is it unfurnished?If you've have not made a mistake, you've made nothing0 -

Of course you can miss a month, you should be in charge of what and who you pay.

The best way forward would be to cancel your payment to Stepchange and work out how to self manage your DMP.

That will mean firstly checking how many of your debts have defaulted, if any haven't you defiantly don't pay them until they have, saving up an emergency fund and then deciding what to pay your creditors.

You must have jumped into a DMP without researching first the best way to go about it.

If you go down to the woods today you better not go alone.0 -

Most rental properties are generally offered unfurnished. Some might come furnished but wouldn't appeal to many, since such tenants would need to then put their own furniture into storage.RAS said:This is a completely informal arrangement. You can pause if you need to, or just terminate the deal if you want to manage the debts yourself. How much is in your statement of affairs/budget for emergencies?

I'm also a bit surprised you are renting and have to provide you own bed. Is it unfurnished?0 -

I did do my research before - but things changed after I did it. I had a big emergency fund (£2500 ish) but something dramatic happened and that ate that. Happy to explain exactly what by DM but I'd prefer not to post here if you're interestedGrumpelstiltskin said:Of course you can miss a month, you should be in charge of what and who you pay.

The best way forward would be to cancel your payment to Stepchange and work out how to self manage your DMP.

That will mean firstly checking how many of your debts have defaulted, if any haven't you defiantly don't pay them until they have, saving up an emergency fund and then deciding what to pay your creditors.

You must have jumped into a DMP without researching first the best way to go about it.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.7K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 246.8K Work, Benefits & Business

- 603.3K Mortgages, Homes & Bills

- 178.2K Life & Family

- 260.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards