We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Pensions Advice

Comments

-

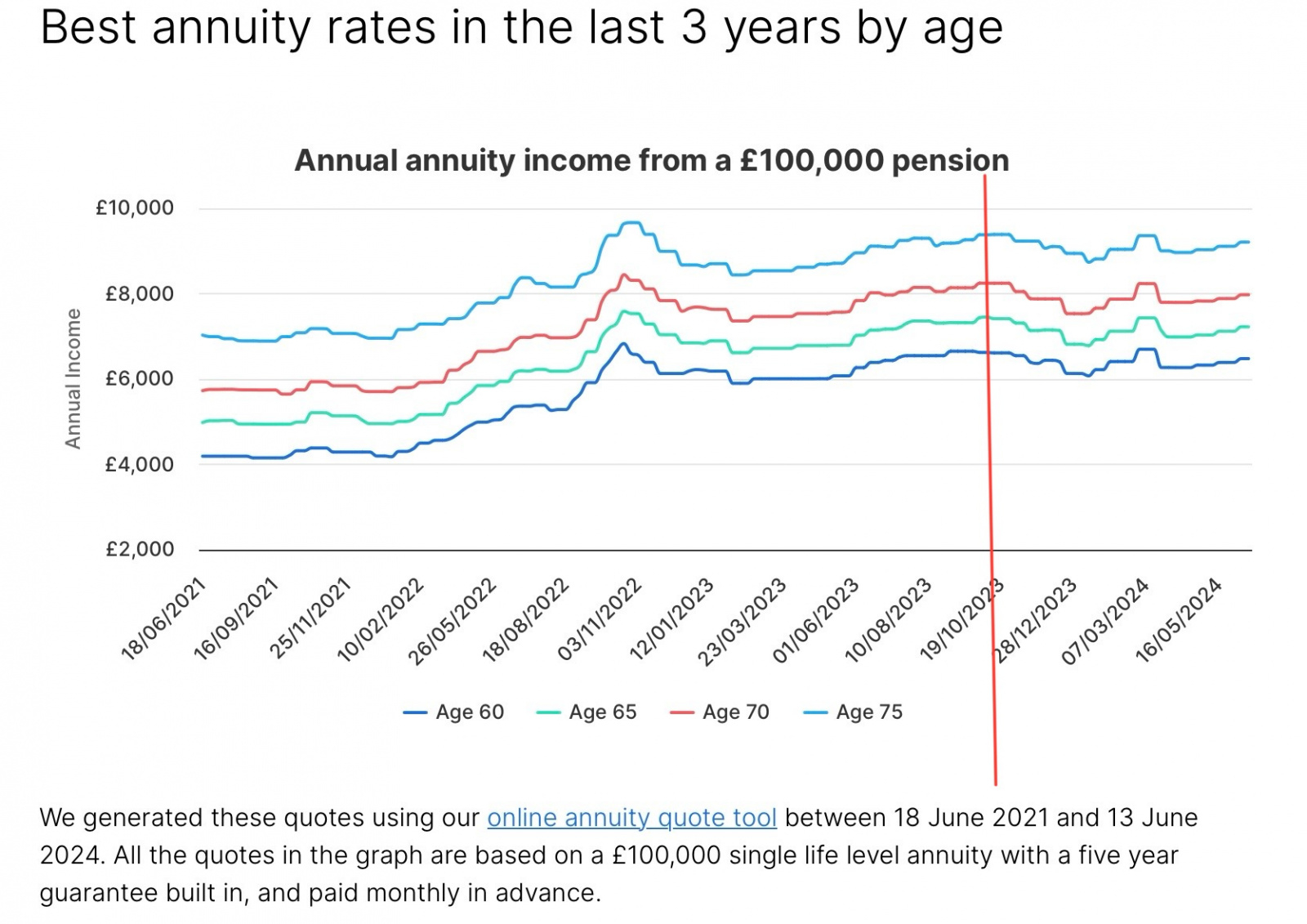

The problem here is when annuity rates are volatile and some providers change their annuity rstes daily.For an annuity, yes. If you buy an annuity via the internet, they are still allowed to take commission. That commission is factored into the annuity rate (i.e. you get a lower annuity rate). An IFA cannot take a commission but would charge a fee. That fee is taken from the pension pot and uses the nil-commission annuity rate. So, the pot will be lower due to the fee but the annuity rate will be higher. (the fee can also be paid after the TFC is taken or externally)

There comes a point where the IFA fee is lower than the commission for the direct option (providing you don't use a greedy IFA). e.g. if the IFA fee is £1500 and the commission option is £2500. Smaller pots tend to favour

Plus,the insurers have said that IFAs generally get better rates because the quality of the medical disclosures tends to be better than non-advised distribution. I get that because I have done quotes for people who have used a direct option for a quote and via us, and the medical form they filled in was low detail, and I had to do a fair bit of extra questioning to get the detail, and it makes a difference. Extra information can never lower the annuity rate. It can only leave it the same or improve it. The direct options don't question the info they are given as they are non-advised. Like most quote engines on various products, they quote on what they are told.

I was happy to press the buy button last October for an RPI annuity via Hargreaves Lansdown. The best annuity was a lot higher than the other 5 providers on that quote. So I went for it. Only minor health issues but a GP report had to be supplied.

Had I gone through an IFA the quote could have been lower due to more time needed as index linked annuity rates dropped shortly afterwards.

(Could have gone the other way of course.)

I had been running quotes on H-L regularly and when I saw the quote I wanted I just took it.

I still have 1/3 of my pension in a drawdown pot (plus two defined benefits in payment) so I can draw more as and when required.

When annuity rates are more stable, or health is poor, then fair enough - use an IFA.

I retired yesterday, no regrets.

2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.7K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.5K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards