We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Please help me understand PCSPS / Alpha Ill Health Pension Options (Civil Service)

Comments

-

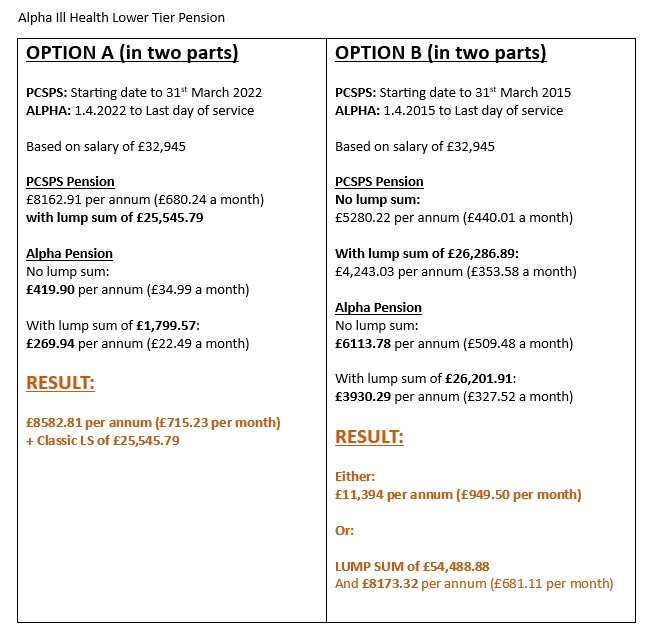

Think you need to check your Option A figures PCSPS should be £8k p/a pension PLUS £24k automatic lump sum, not OR0

-

If you forget the ill health early retirement this is basically a McCloud judgement decision that has to be made.

Option A is taking the judgement and Classic pension continues through to 2022, OR ignore the McCloud ruling (OptionB) and accept the move to Alpha in 2015. As I mentioned earlier I have the very same decision to be made sometime next year when my pack comes through. When I retired in 2022, I was retired with effectively Option B as it hadn't been fully completed through Parliament at that time. Its good to see how the options pack will look.1 -

Thanks for the comments.

Would this be a fair summary? I'm obviously going to advise her to go back to them to check all the figures and get some professional advice. Just want to make it a bit simpler for her:

0 -

JillyC8 said:Thanks for the comments.

Would this be a fair summary? I'm obviously going to advise her to go back to them to check all the figures and get some professional advice. Just want to make it a bit simpler for her:

You have done the same thing with option B as you did with option A.

The PCSPS comes with an automatic PCLS of 3x the annual pension (£15,840)

The way you have written it indicates that you can give up pension of £1,037 in return for a lump sum of £26k but that is not possible.

You get £15,840 come what may, giving up £1,037 of the pension only gets you an extra £12,448. The normal (poor) 12:1 rate.

You are also quoting a total lump sum of £26,286 but it should be £28,286 according to the earlier screenshot you posted.0 -

Setting aside the outstanding issues to resolve:

- Why is no WPS refund payable under PCSPS Option B?

- Why is the interest on the WPS refund under Option A so low?

Aside from specific queries such as those above, MyCSP will not check any calculations.

Not sure what professional advice you would be seeking, given it is clear that B >A. Would it be around whether to take standard or maximum lump sum? I really wouldn't think it worth shelling out for professional advice about that, but up to individuals obviously. There are other differences, such as survivor benefits (which are probably better under B anyhow), but those are very unlikely to change the conclusion.

0 -

Thank you so much all. I will pass this back to her and never offer to look at something like this again :-). This should give her a clearer indication of what her options are. Much appreciated.0

-

Does she realise if she takes minimum pension income and maximum lump sum she is giving up 25 to 30% inflation linked income for life (compared to the balanced matched lump sum option)? She is 55 and could live to 85+. Over 30 years that is a huge loss of income for taking the extra £29k lump sum now. Unless there is a serious (almost emergency or life defining need) for that extra lump sum (i.e. why isn't £25.5k enough?) then it is generally a poor financial decision to take it.

1 -

I've explained to her the downfall of taking the maximum lump sum but now it's up to her. I'm not sure what other pension provisions she has in place.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards