We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Confused about new LTA rules

Neversurrender

Posts: 108 Forumite

Hi,

I have been trying to understand this Lifetime allowance stuff, especially since the new rules werwe introduced.and was wondering if anyone could assist please.

The more I google and ask the more confusing it gets, and my priovider just bombards me with acronyms and other jargon

I'm aware the old rules calculated lifetime allowance as a percentage.

Heres my case.

Pension is a SIPP platform with A J Bell.

1) I have made about 3 drawdowns before new rules introduced this April 2024

Each drawdown included a tax free element of 25%

2) And I have made a drawdown which occured this April after the new rules introduced, again with a tax free elemenmt of 25%

Do I now simply add up the total of all the tax free I have taken in each drawdown and deduct from the new limit of £268,275 to work out what allowance I have left?

Any help much appreciated,

Thanks

0

Comments

-

Do I now simply add up the total of all the tax free I have taken in each drawdown and deduct from the new limit of £268,275 to work out what allowance I have left?

Basically yes.

1 -

If you drew down when the LTA was lower than £1,073,100 it would be worth looking at a Transitional Tax-Free Amount Certificate.1

-

Many thanks. Will doshortseller09 said:If you drew down when the LTA was lower than £1,073,100 it would be worth looking at a Transitional Tax-Free Amount Certificate.

0 -

Just reread your post - if you have drawn down this financial year i.e. after April 6th, then I don't beleive you are eligible for a TTFAC, apologies for any misunderstanding.1

-

2) And I have made a drawdown which occured this April after the new rules introduced, again with a tax free elemenmt of 25%As mentioned above, this prevents you from applying for a certificate. You must apply for the certificate before a BCE occurs after 6th April 2024.

Do I now simply add up the total of all the tax free I have taken in each drawdown and deduct from the new limit of £268,275 to work out what allowance I have left?

No. You have lost that option. You are now limited to using the lifetime allowance figures.Remaining lump sum allowance = £268,275 – (25% x previously used % of lifetime allowance on 5 April 2024 x £1,073,100).

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

I'd be most grateful for some added clarity here please. My position is that I had crystallised a percentage of the Lifetime Allowance pre 6th April 2024, via my SIPP, taking 25% tax free at that time.dunstonh said:2) And I have made a drawdown which occured this April after the new rules introduced, again with a tax free elemenmt of 25%As mentioned above, this prevents you from applying for a certificate. You must apply for the certificate before a BCE occurs after 6th April 2024.Do I now simply add up the total of all the tax free I have taken in each drawdown and deduct from the new limit of £268,275 to work out what allowance I have left?

No. You have lost that option. You are now limited to using the lifetime allowance figures.Remaining lump sum allowance = £268,275 – (25% x previously used % of lifetime allowance on 5 April 2024 x £1,073,100).

I am now hoping very shortly to initiate a defined benefit pension (so post 6th April 2024) and take an element of the offered tax free cash. My understanding was that the tax free cash soon to be taken with the initiation of the defined benefit pension would just be added to the previous SIPP tax free cash and be counted towards the maximum of the £268,275 tax free cash available to me.

I am intending later this year to crystallise more of the available uncrystallised SIPP to erode what will be left of the maximum tax free limit of £ 268,275.

Would this sequence require any specific certificate as I had assumed all would be straightforward?

0 -

AFAIK, it should be straightforward.JamesP8 said:

I'd be most grateful for some added clarity here please. My position is that I had crystallised a percentage of the Lifetime Allowance pre 6th April 2024, via my SIPP, taking 25% tax free at that time.dunstonh said:2) And I have made a drawdown which occured this April after the new rules introduced, again with a tax free elemenmt of 25%As mentioned above, this prevents you from applying for a certificate. You must apply for the certificate before a BCE occurs after 6th April 2024.Do I now simply add up the total of all the tax free I have taken in each drawdown and deduct from the new limit of £268,275 to work out what allowance I have left?

No. You have lost that option. You are now limited to using the lifetime allowance figures.Remaining lump sum allowance = £268,275 – (25% x previously used % of lifetime allowance on 5 April 2024 x £1,073,100).

I am now hoping very shortly to initiate a defined benefit pension (so post 6th April 2024) and take an element of the offered tax free cash. My understanding was that the tax free cash soon to be taken with the initiation of the defined benefit pension would just be added to the previous SIPP tax free cash and be counted towards the maximum of the £268,275 tax free cash available to me.

I am intending later this year to crystallise more of the available uncrystallised SIPP to erode what will be left of the maximum tax free limit of £ 268,275.

Would this sequence require any specific certificate as I had assumed all would be straightforward?

The transitional certificate comes into play if you have previously taken a pension which used a % of LTA, but you did not take any tax free cash. This can happen with a DB scheme for example, where the max pension was taken with no TFC.

With transitional certificate this TFC will still be available, if you have sufficient DC funds to take advantage of it.

There are I think other niche areas where a certificate would be useful as well.1 -

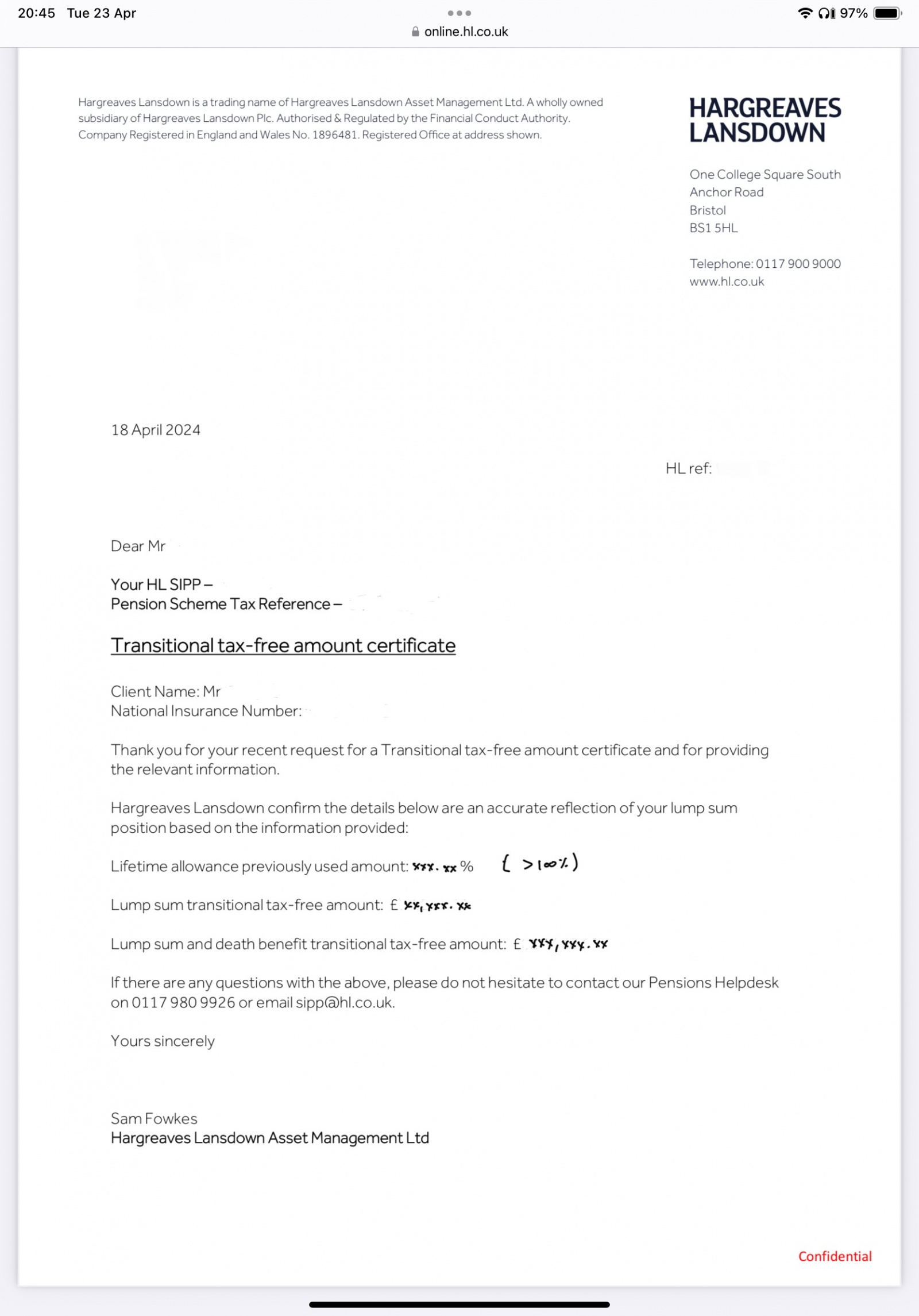

As I posted on another thread, the certificate looks like this …

2 -

Thanks to you both for your input, which is very helpful.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.6K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.6K Work, Benefits & Business

- 603K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards