We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Grandparents childcare credit reconsideration?

Cakeobsessive

Posts: 7 Forumite

Hi there, firstly apologies if this has been already covered elsewhere this is my first post and I couldn’t see a similar query.

I am just here with my mum for the Easter weekend and we happened to start chatting about the outcome of our recent claim for grandparents childcare credits and our confusion with why this hasn’t resulted in a top up to her state pension.

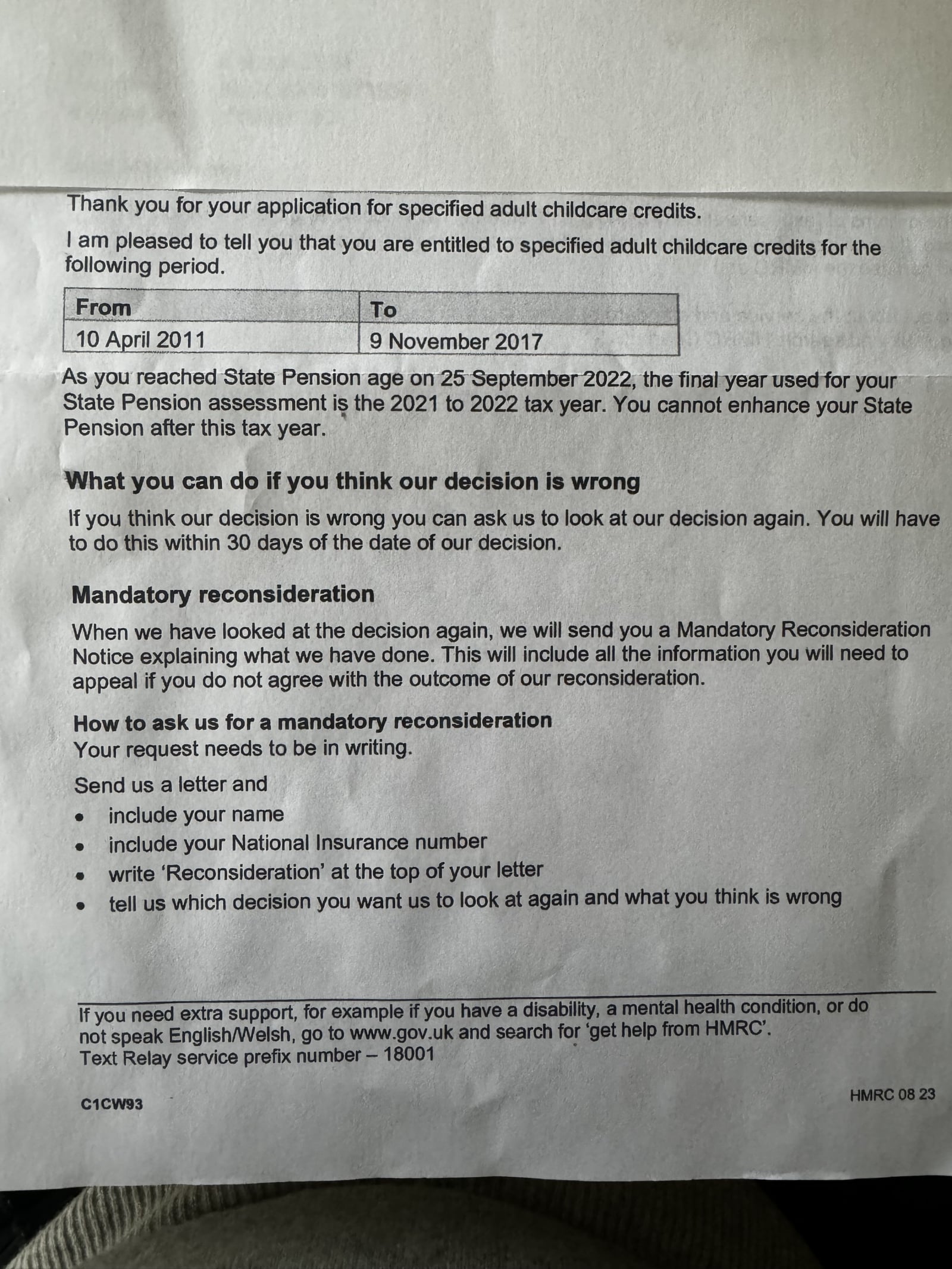

The decision letter (I’ll see if I can attach) states she is entitled to the childcare credits we claimed for however as she reached state pension age in Sept 2022 the final year used for her pension assessment was the 2021-22 tax year and her state pension cannot be enhanced after this year.

This is really perplexing me as I don’t understand why this is the case and I couldn’t see anything in the eligibility rules that said if you were already retired and receiving your pension you couldn’t top it up.

Have we missed an obvious rule here or should we appeal? I see from the letter she has shown me she only has a few more days to send a letter for mandatory reconsideration, can we appeal and what would we need to say or do we just accept it is what it is?

thanks for reading!

I am just here with my mum for the Easter weekend and we happened to start chatting about the outcome of our recent claim for grandparents childcare credits and our confusion with why this hasn’t resulted in a top up to her state pension.

The decision letter (I’ll see if I can attach) states she is entitled to the childcare credits we claimed for however as she reached state pension age in Sept 2022 the final year used for her pension assessment was the 2021-22 tax year and her state pension cannot be enhanced after this year.

This is really perplexing me as I don’t understand why this is the case and I couldn’t see anything in the eligibility rules that said if you were already retired and receiving your pension you couldn’t top it up.

Have we missed an obvious rule here or should we appeal? I see from the letter she has shown me she only has a few more days to send a letter for mandatory reconsideration, can we appeal and what would we need to say or do we just accept it is what it is?

thanks for reading!

0

Comments

-

It's an ambiguous sentence.

You can top it up where there is scope to do so, but only for tax years 2021-22 or earlier - not the year in which you reach State Pension Age (and obviously not years after reaching SPA!).Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!1 -

Purchasing SP top ups is only available, by any method, for years up to the end of the tax year before you reach state retirement. So retiring in September 2022, the 2022-23 tax year, means top ups years are only available up to the 2121-22 tax year.

1 -

thanks both for taking the time to reply, where I am confused is her online record is showing those NI credits have been applied (for those eligible years) and she now has 34 years (up from 28) which should mean she is due the full state pension however her payments have not changed (her most recent payment was £585.44 on the 18 March, her letter attached was dated 6 March, and she had a letter previously stating from the start of May 2024 her payments will increase by 8.5% but still not to the full amount).

I took that sentence to mean we’ve applied the credits but your pension eligibility is set in stone that year before you retired so no amount of top up will change it hard cheese, which seems bizarre as it would mean buying eligible years after you had retired would also not change your future pension so surely wouldn’t be an option! Is this a case of timing as in if she waits another month or 2 she’ll start seeing the increased payments?

The simple option would be to call HMRC but it’s a bank holiday and she’s too anxious to call when I’m not around to help her and we go home on Monday 😞

There is no where on her online account where I can see her past or future payments either. I think it would have been helpful if they’d stated in the letter whether there would be any changes to her payments and what they would be.

It says we only have 30 days from 6 March to appeal so we can’t wait until Aprils payment to see what it might be, but I am no clearer whether I should be doing this for her argh!

0 -

HMRC have applied the credits to her account. They will pass that information on to DWP who will re-assess her pension position, that can take several months but should be backdated to at least the time the credits were applied.and she now has 34 years (up from 28) which should mean she is due the full state pension however her payments have not changed (her most recent payment was £585.44 on the 18 March,

Those additional 6 years will add up to £34.92 to her existing pension. £585.44 / 4 = £146.36 per week so her new maximum amount will be £181.31, well short of the new pension maximum. (Pre 2016 years do not necessarily add £203.85 / 35 per year depending on personal circumstances, in fact may not actually add anything at all)

1 -

Thanks for that @molerat you’ve calmed me down! Our interpretation did seem a bit irrational. Hopefully given time she’ll see the change. Would definitely help if their communication was a bit clearer!0

-

Note my update. Are you certain those years will add much to her pension ?0

-

Does your mother receive a pension from a scheme that was contracted out of SERPS/S2P?0

-

@xylophone no I don’t believe so.

@molerat I think I was wrong in thinking 34 years was enough for the full entitlement on reading further it looks like she needs 35 years. So with the 34 years she has now with the added grandparent credit that should increase her weekly payments to around £197.88 (34x£5.82) rather than what her payments would be going forward from May which were stated in her recent letter from DWP as around £635 every 4 weeks (an increase of 8.5% from the current £585).We’ve looked at her online account again and it seems like she has some partial years that she could potential pay up including one that would cost around £300 and still is open to pay until 2025 so I think that would probably be her best option to take her to the full 35 years.

thanks again this exchange has really helped me get my head around it a bit better!0 -

35 years is not relevant to anyone with a pre 2016 history. If she currently has £146.36 that is 10 years short of the max. With 28 years she would have £163.08 if not contracted out so it looks like she was and a few of those granny credits may have added nothing to her pension. How are her full years currently split pre and post April 2016 ? I am afraid this topping up game is not as simplistic as you are seeing it.

0 -

no I don’t believe so.

Is your mother in receipt of any pension other than state pension?

If so, where is it from?

Did she obtain a state pension forecast?

Was a COPE shown?

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604.1K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards