We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Pension I am a wondering......

Comments

-

Maybe in the 1960s.[Deleted User] said:

Because I thought the money to pay for pensions was in the NI and if they cut that down to zero - where will the money come from to pay for the pension...However people here had said it will come from income tax, I can't see the point myself. Unless they are trying to get us to pay more overall sneakily, which is probably what they will do.penners324 said:Why do you think the state pension will disappear because NI has reduced?

There's no real link between the amount of NI paid in and pensions paid out.

NI is just tax. getting rid of employee NI would make the tax system much simpler2 -

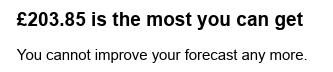

Thank you.xylophone said:I just did that check and it shows my forecast is a bit below £11.5k:

Was this the "ESTIMATE AT 5/4/23"?

If so, then you had already accrued a full New State Pension (£203.85 a week in 2023/4) plus a "protected payment" of £12.33 a week) at that date.

The weekly full NSP will increase to £221.20 a week from 8th April while your "protected payment" will increase to around £13.16 a week.

A person who has a protected payment had a "starting amount" in excess of a new state pension at 6/4/16.

This meant that although (if under state pension age and earning the relevant amount) he would have to continue to pay NI up to SPA, this would NOT improve his state pension.

The "starting amount" would revalue each year , the amount equal to full NSP under the Triple Lock and the excess the "protected payment" by CPI.

https://www.gov.uk/new-state-pension/what-youll-get

Yes, that was checked earlier this week, but it does say based upon NI record up to 5th April 2023 (which is logical as this tax year is not over yet).

So, I get the full SP plus a little bit for a short while that the employer at the time operated SERPS which is now the "protected payment". Is that correct?

Also said I have 34 full years of contributions. Plus one partial year (2021-22). So there is no purpose in paying that partial year to be a full year. And nothing to lose if future years are not full qualifying years. Is that all correct?0 -

Grumpy_chap said:

Thank you.xylophone said:I just did that check and it shows my forecast is a bit below £11.5k:

Was this the "ESTIMATE AT 5/4/23"?

If so, then you had already accrued a full New State Pension (£203.85 a week in 2023/4) plus a "protected payment" of £12.33 a week) at that date.

The weekly full NSP will increase to £221.20 a week from 8th April while your "protected payment" will increase to around £13.16 a week.

A person who has a protected payment had a "starting amount" in excess of a new state pension at 6/4/16.

This meant that although (if under state pension age and earning the relevant amount) he would have to continue to pay NI up to SPA, this would NOT improve his state pension.

The "starting amount" would revalue each year , the amount equal to full NSP under the Triple Lock and the excess the "protected payment" by CPI.

https://www.gov.uk/new-state-pension/what-youll-get

Yes, that was checked earlier this week, but it does say based upon NI record up to 5th April 2023 (which is logical as this tax year is not over yet).

So, I get the full SP plus a little bit for a short while that the employer at the time operated SERPS which is now the "protected payment". Is that correct?

Also said I have 34 full years of contributions. Plus one partial year (2021-22). So there is no purpose in paying that partial year to be a full year. And nothing to lose if future years are not full qualifying years. Is that all correct?

Yes, as it's says, you cannot improve your forecast any more.

The two elements are inflation protected slightly differently. The standard £203.85 gets triple lock increases (8.5% this April so that be ones £221.20).

The protected payment is whatever the CPI rate was the previous September.1 -

Thank you.Dazed_and_C0nfused said:

Yes, as it's says, you cannot improve your forecast any more.

It is quite confusing.

I thought an individual needed 35 years to get the full state pension, so I seem to have won") 0

0 -

Those are the rules for people staring to build up an NI history from April 2016 onwards.Grumpy_chap said:

Thank you.Dazed_and_C0nfused said:

Yes, as it's says, you cannot improve your forecast any more.

It is quite confusing.

I thought an individual needed 35 years to get the full state pension, so I seem to have won

Everyone else comes under transitional rules and so far the number of years has, if memory serves, ranged from 28 to 50.1 -

Thank you.xylophone said:I just did that check and it shows my forecast is a bit below £11.5k:

Was this the "ESTIMATE AT 5/4/23"?

If so, then you had already accrued a full New State Pension (£203.85 a week in 2023/4) plus a "protected payment" of £12.33 a week) at that date.

I also now checked the SP forecast for my wife:

So, she has accrued the full SP and it can never increase (other than Triple Lock or replacement value adjustment mechanisms).

Mrs G_C also does not seem to have lost SP value even though she was "contracted out" for a period and will have accrued a small amount of COPE within one of her employment pensions - probably when she worked for NHS.

Am I absolutely correct that, even though we both have "missing / incomplete" NI contribution years, we have absolutely no reason to make up that shortfall through voluntary contributions?

And, if we never worked again or never made further NI contributions, there would be no impact to State Pension that we would receive once we reach SPA?

(This latter point is pertinent for Mrs G_C as she is not currently working or claiming benefits and, it seems no value in her continuing to "sign on" for her "credits" via Job-Centre.)

I think the above is exactly what has been advised in this thread - I just find it all rather generous and unbelievable

0 -

Freezing tax thresholds, fiscal drag is a sneaky way to tax pensioners ..reckon will be used in future...again punishing thriftiness1

-

Not particularly; it is just getting more people back into paying more taxes. The personal allowance is still very generous compared to the past. Hopefully, it will get back down to £8k or 9k in today's terms or around that as it used to be before the massive increase in the past.daz378 said:Freezing tax thresholds, fiscal drag is a sneaky way to tax pensioners ..reckon will be used in future...again punishing thriftiness0 -

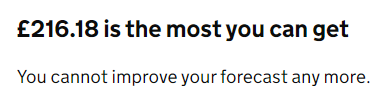

I've been checking my state pension forcast. On the first screen it tells me

You need to continue to contribute National Insurance to reach your forecast

Estimate based on your National Insurance record up to 5 April 2023

£195.01 a weekForecast if you contribute another 2 years before 5 April 2039

£203.85 a week£203.85 is the most you can get

but then when I check my NI Contributions page it saysYou have:

- 35 years of full contributions

- 16 years to contribute before 5 April 2039

You do not have any gaps in your record.

Why does one say I have 35 full years but the other says I need to contribute another 2 years to get the full pension ? Am I correct in guessing I fall under the transitional arrangements0 -

Yup that's correct - from memory people on here have taken from late twenty to early fourty years to get a full pension. It's only people who have started working from April 6th 2016 who can (currently) rely on 35 years of contributions to mean a full state pension.huw01 said:Why does one say I have 35 full years but the other says I need to contribute another 2 years to get the full pension ? Am I correct in guessing I fall under the transitional arrangements

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.8K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards