We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Annuity beats drawdown

Comments

-

It would be interesting to know what the recommendations would be from an IFA.1

-

That would depend on what you wanted to achieve.Nosmo_King_2 said:It would be interesting to know what the recommendations would be from an IFA.1 -

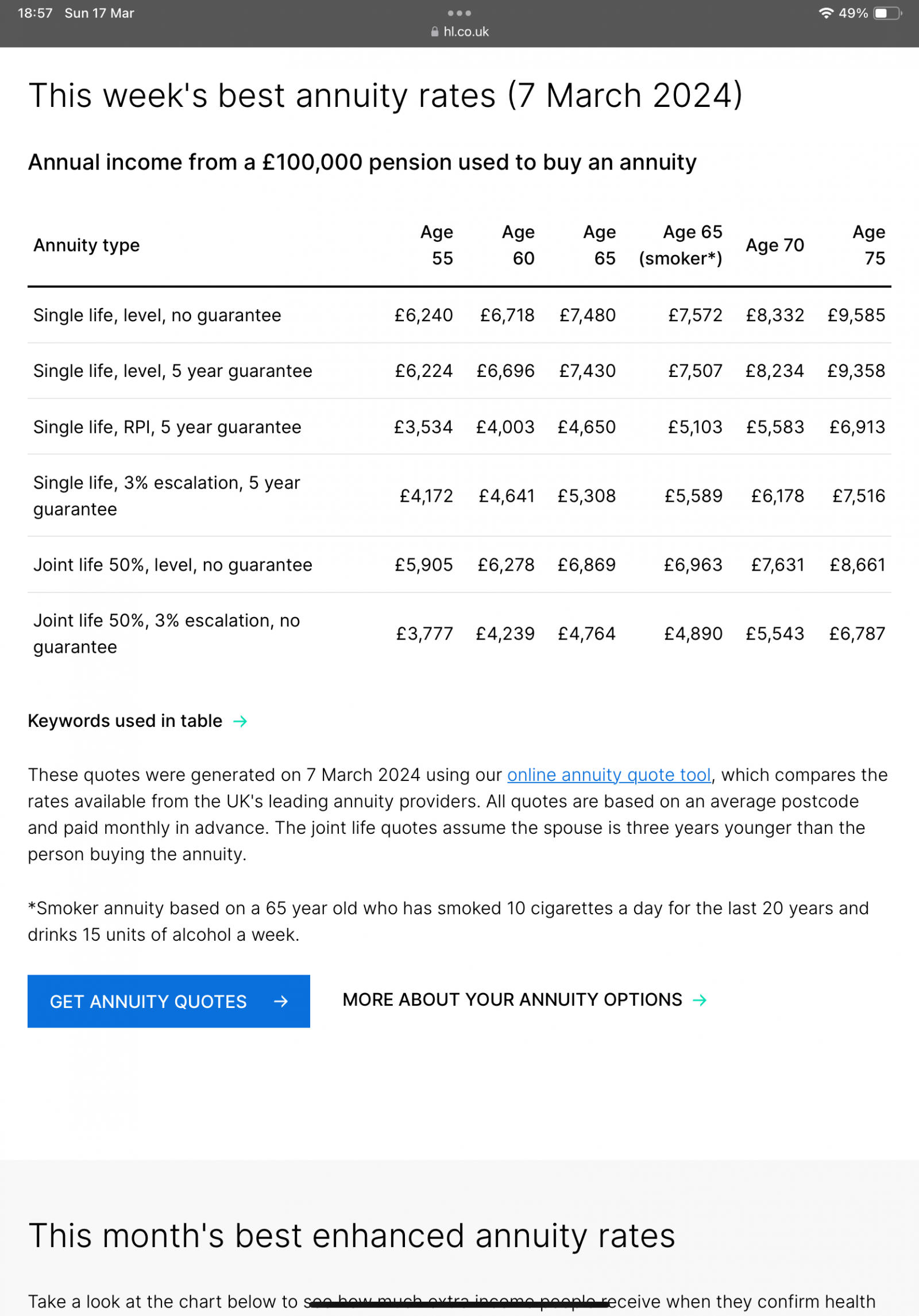

According to Hargreaves Lansdown you can get approximately 7.5% at age 65 so maybe OP is around that age?Audaxer said:

I think that would make the crossover point 17 years, as I calculate £4,800 increasing at 4.5% inflation pa would be worth an actual £9,707 after 17 years, whereas the annuity would still be giving you a fixed £9,200 pa. If you took the annuity but only need to spend £4,800 plus inflation each year, you could presumably save or invest the rest of the income until you need it after year 17 to boost your fixed annuity income.sgx2000 said:

At 4.5% inflation the relative value of the £9200 will halve in 17 years

and the 4% £4800 withdrawl will increase by inflation proportionately

I assume (have not done the calc yet) the crossover point is 12 or 13 years

It does seem to me like a generous annuity rate, but not sure whether it is the best option if you don't need that much income to start with.

1 -

It's very difficult to compare the two as you don't know what growth you are forsaking when purchasing an annuity, and how long you are going to live. If there was a 5 or 6 year bear run an annuity could well have been a great decision, however if growth averages 8% pa over the next 10 years and inflation is 3% pa suddenly its not such a great decision. Horses for courses and all that

It's just my opinion and not advice.1 -

I am 64FIREDreamer said:

According to Hargreaves Lansdown you can get approximately 7.5% at age 65 so maybe OP is around that age?Audaxer said:

I think that would make the crossover point 17 years, as I calculate £4,800 increasing at 4.5% inflation pa would be worth an actual £9,707 after 17 years, whereas the annuity would still be giving you a fixed £9,200 pa. If you took the annuity but only need to spend £4,800 plus inflation each year, you could presumably save or invest the rest of the income until you need it after year 17 to boost your fixed annuity income.sgx2000 said:

At 4.5% inflation the relative value of the £9200 will halve in 17 years

and the 4% £4800 withdrawl will increase by inflation proportionately

I assume (have not done the calc yet) the crossover point is 12 or 13 years

It does seem to me like a generous annuity rate, but not sure whether it is the best option if you don't need that much income to start with.

My best quote has been from L&G

Highest constantly for the last 6 months.....

It may be that their online quote algorithm handles medical issues better

When, and if. I eventually decide to do it, i will obviously look harder and get proper (not online) quotes

My current expenditure will be met by SP and a good DB index linked pension

So

My current idea is to split this DC pension between annuity any drawdown....

2 -

Possibly or probably......eskbanker said:

Wouldn't that favour the flexibility of drawdown for the rest, if you have the potential downside covered off already?sgx2000 said:

My current expenditure will be met by SP and a good DB index linked pension

I do however like the idea of cutting the risk of a major worldwide recession ......1 -

Just like my thinking, the future won't be the same as the past, it will have similarities indeed, but will be different and I'm guessing it will look very different as there are very different dynamics, mechanisms and very unpredictable outcomes.sgx2000 said:

Possibly or probably......eskbanker said:

Wouldn't that favour the flexibility of drawdown for the rest, if you have the potential downside covered off already?sgx2000 said:

My current expenditure will be met by SP and a good DB index linked pension

I do however like the idea of cutting the risk of a major worldwide recession ......

Having a bedrock of a DB & SP and then splitting up the DC surplus in to an annuity and drawdown sounds reasonable to me.3 -

An annuity is longevity insurance, drawdown is income generation from an investment. The two should be combined appropriately to provide for retirement and any legacy you want to leave.

And so we beat on, boats against the current, borne back ceaselessly into the past.1 -

You would get a decent 2nd hand Ferrari for that amount.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards