We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

State Pension Uprating

Comments

-

Another satisfied customer 😉blue.peter said:Just in case anyone cares...

As recommended by @ColdIron, I phoned the Future Pension Centre on the dot of 08:00. Several menus to work through, but I got to a very helpful gentleman fairly quickly. He rapidly got to the same point as @Dazed_and_C0nfused did yesterday, recommended paying three years' NI conts, picked the three cheapest, and gave me the same total cost as I'd worked out. I said "yes, please". He then transferred me to HMRC, who gave me all the necessary payment details (so no need for me to make a second phone call). Card payments aren't accepted, which was a minor disappointment.

All done by 08:16.I've set up the necessary transfer from building society savings to bank account, and will pay those voluntary NI contributions by bank transfer in a couple of hours or so.Thank you all very much for your help and advice.0 -

blue.peter said:Card payments aren't accepted, which was a minor disappointment.They do do Open Banking, 'Pay by Bank Account' I thinkFast and certain0

-

That was certainly my experience this morning. Probably the best I've ever had with a government department.ColdIron said:Once you get through they are genuinely helpful

Very much so, thank youDazed_and_C0nfused said:Another satisfied customer 😉") ColdIron said:blue.peter said:Card payments aren't accepted, which was a minor disappointment.They do do Open Banking, 'Pay by Bank Account' I thinkFast and certain

ColdIron said:blue.peter said:Card payments aren't accepted, which was a minor disappointment.They do do Open Banking, 'Pay by Bank Account' I thinkFast and certain

Yes, I noticed that one when I was digging around yesterday, but couldn't see exactly what it was without the payment reference number that I got from HMRC this morning. I thought that it sounded like a sort of one-off DD, and wondered how it worked. I was intending to investigate it later because it sounded likely to be my best option. Thanks for confirming that I was right in my guess.

0 -

If you 'push' the money to them with faster payments they need the reference to know where to apply itWith open banking it's a 'pull' (a bit like a DD I suppose) so they don't need you to quote it1

-

Those of us with a lot of contracted out service but enough time between 2016 and SPA to be able to add to our pensions are the true winners under the new pension scheme.

4 years of voluntary NI took me up to the full nSP, with the final year buying me £4.80, so even that was a no-brainer.

But not everyone sees that. I have a friend (who is always right about everything) in a similar situation, but she refuses to top-up on the grounds that she's paid in enough tax and NI in her time and she's not going to give them a penny more.

6 -

Silvertabby said:I have a friend (who is always right about everything) in a similar situation, but she refuses to top-up on the grounds that she's paid in enough tax and NI in her time and she's not going to give them a penny more.I can understand the thinking, fallacious as it is. It's a triumph of emotion over logic. I'm glad that I was open to persuasion.Anyway, £2,420.60 now paid to HMRC for three years' voluntary Class 3 NI Contributions. Acknowledgement e-mail received from HMRC, text message confirming payment made received from Santander. All done and dusted. Diary reminder set to check my State Pension Forecast and NI record for Tuesday 30 April (today + eight weeks and one day).

3 -

ColdIron said:If you 'push' the money to them with faster payments they need the reference to know where to apply itWith open banking it's a 'pull' (a bit like a DD I suppose) so they don't need you to quote itNot quite true - I had to enter the reference before I could get into the system that generates the pull. I then told it that I banked with Santander and the amount that I wanted to pay. It transferred me to Santander's system to authorise the payment. Once that was done, I was taken back to HMRC's site, where I saw a confirmation and a statement that they'd sent me an e-mail.(Obviously, the e-mail confirmation needed my e-mail address, but this was voluntary.)2

-

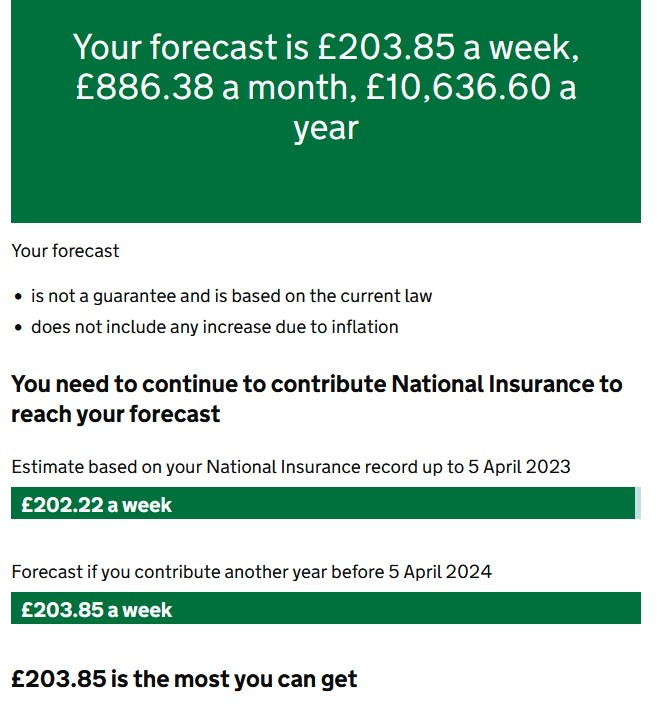

Update: It's taken HMRC and DWP less than two weeks to update my NI record and State Pension entitlement. My forecast now looks like this:

Dazed_and_C0nfused said:

Dazed_and_C0nfused said:

A fourth year would only add the final £1.79/week so less of a bargain but probably still worth doing as you will recoup your money in less than 10 years.

Allowing for tax and next April's uprating, the calculation looks like this:£824.20 / (£1.63 * 52 * 0.8 * 1.085) = 11.20 years to recoup the outlay.So the question of whether or not it's worth it is, for me, borderline. It depends on my assessment of my life expectancy. Will I live to be over 77? I don't think that I'll bet on it.I'm very grateful for the helpful advice offered to me above, and especially for @Dazed_and_C0nfused 's highly persuasive numbers.

4 -

Good to get an update and things should be straightforward come November with no changes needed once you start to receive the pension.

And at least the system does seem to be working well for some people.1 -

Just checking: Do you realise that you have to APPLY for your state pension to start being paid? I ask because some people assume that it will start automatically when they reach state pension age, which is not the case.blue.peter said:I know that my pension won't actually start arriving in my bank account until a week or two after my birthday,4

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.9K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.7K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards