We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Pension Targets

Comments

-

Those fund names don't give a great deal away. Is there an area where you can select new funds on the pension website? I only ask as it will probably have more information about the different funds available there. As you are still young, you would probably benefit from having everything in a globally diverse 100% equities fund. Do you know why you have two different funds currently, is that the extra percentage point you started paying in recently?SieIso said:

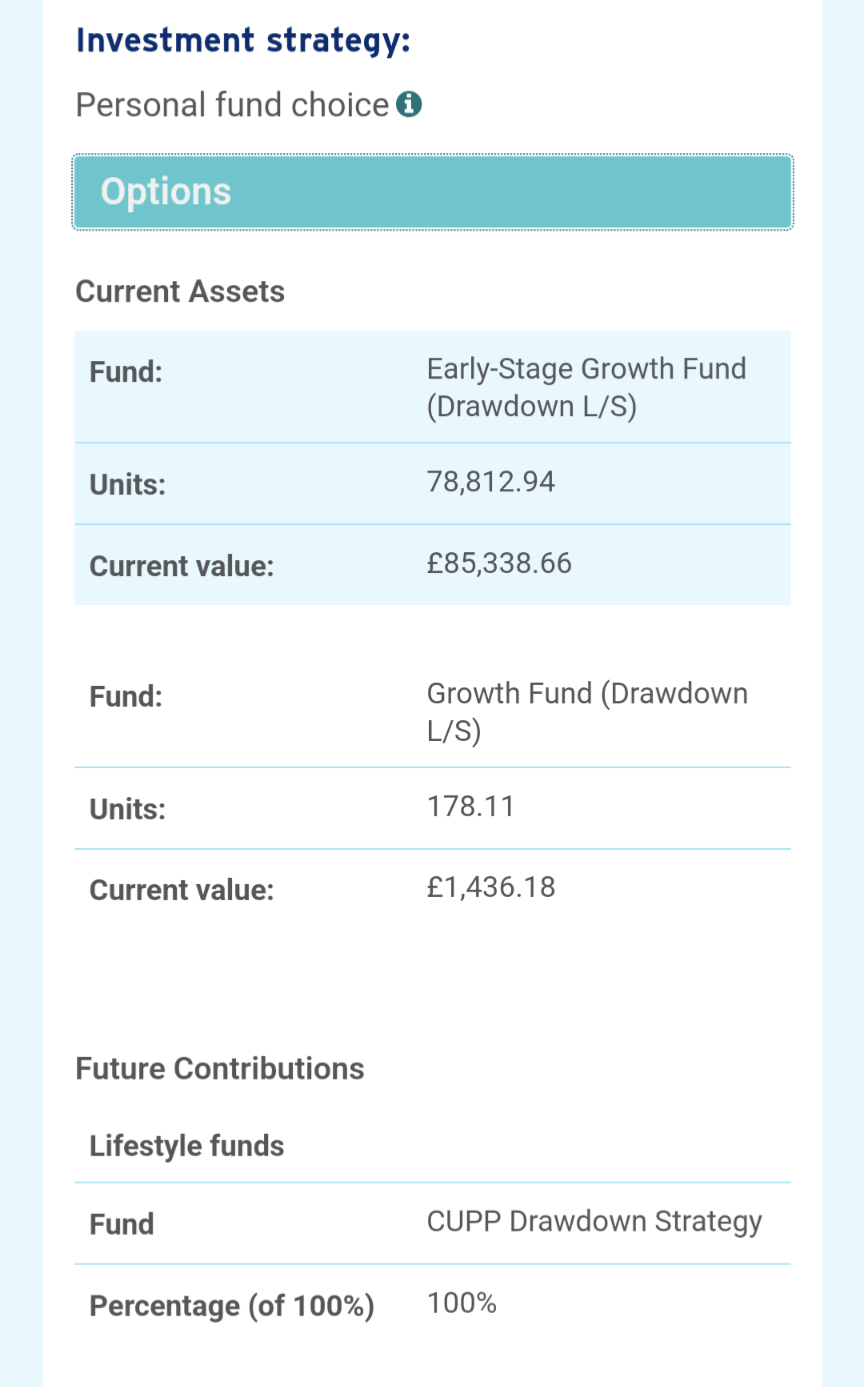

Is this what you mean?barnstar2077 said:I would investigate how your money is invested in your pension, and what your options are for different funds etc. How your pot is invested can make a massive difference.

I wouldn't worry too much though, but if you can afford to put a bit more in then do so. The guy that you spoke to was hardly impartial as others have said!Early-Stage Growth Fund (Drawdown L/S) £84,881.52 Growth Fund (Drawdown L/S) £1,429.45 Think first of your goal, then make it happen!0 -

Well just hit a landmark target this eve . My DC pension hit over £500k for the first time. I have contributed to it for the past 15 years and over that time the total contributions have averaged at 12k per annum.Sielso - I was going through some paperwork today and found a document from 8 years ago when I was 40 and my pension value was £108k then, so it shows what can be achieved. I’d suggest look for Global Equity and North American funds. Do your research but they’ve worked for me. Between me and my employer my annual contributions are now £23k per annum so increase where you can.You’re doing great and showing any level of interest is doing more than most.1

-

All eggs in one basket unfortunately is almost certainly going to disappoint over a multi decade time frame. Trades eventually run out of steam as they get crowded out. Resulting in summary in price instability. Not the optimal way of creating a portfolio.barnstar2077 said:

As you are still young, you would probably benefit from having everything in a globally diverse 100% equities fund.SieIso said:

Is this what you mean?barnstar2077 said:I would investigate how your money is invested in your pension, and what your options are for different funds etc. How your pot is invested can make a massive difference.

I wouldn't worry too much though, but if you can afford to put a bit more in then do so. The guy that you spoke to was hardly impartial as others have said!Early-Stage Growth Fund (Drawdown L/S) £84,881.52 Growth Fund (Drawdown L/S) £1,429.45 0 -

I'm struggling to understand this comment. A global equity tracker is hardly 'all eggs in one basket', unless you are referring to asset class? And over the long term, equities have historically outperformed any other conventional asset class. So if this is a long term investment, then I'm not sure why it would almost certainly disappoint?Hoenir said:

All eggs in one basket unfortunately is almost certainly going to disappoint over a multi decade time frame. Trades eventually run out of steam as they get crowded out. Resulting in summary in price instability. Not the optimal way of creating a portfolio.barnstar2077 said:

As you are still young, you would probably benefit from having everything in a globally diverse 100% equities fund.SieIso said:

Is this what you mean?barnstar2077 said:I would investigate how your money is invested in your pension, and what your options are for different funds etc. How your pot is invested can make a massive difference.

I wouldn't worry too much though, but if you can afford to put a bit more in then do so. The guy that you spoke to was hardly impartial as others have said!Early-Stage Growth Fund (Drawdown L/S) £84,881.52 Growth Fund (Drawdown L/S) £1,429.45

There is of course the question of risk appetite and willingness to accept large downward movements without panicking, but that's a separate issue to absolute performance in the long run.1 -

Hi Sielso, I am a similar age (38) and aiming for similar in that I want a pot that pays out 22ishk because my current annual outgoings including £5k savings a year is adequately funded by that as a gross income. I'm aiming to have approx a £900k pot at retirement at 60-65 across my pension pots and LISA. I've various thoughts about annuities and drawdowns, and spending profile as I age but my understanding is that £900k should be adequate for whichever I choose.SieIso said:Hi All,

I have not always focused too much on my pension but in recent years I have taken a much keener interest in it. I spoke to a representative from my pension provider this week who was onsite at my workplace, they advised that my pension is "much too low" and I should make serious efforts to address this. The representative advised that he could not give any further advice.

I am 40 and my pension pot is currently £86,400. My employer contributes 11% of my salary (£40k) and I contribute 10%. I have increased by contributions from 9% in 2023 to 10% in 2024. I am not sure what more I can do or what I need to do or even where I should be at this stage. I have been told before by the same provider that my pension pot should be of concern to me and I have tried to address this by increasing my contributions but I worry that I have left things too late.

I would like to get a pot that pays out approximately £25k per annum and I have no other pension pots.

Any advice would be great.

This assumes

- a level of inflation

- a level of pot value increase due to portfolio performance

- no state pension (I'm treating it as my buffer to account for my pot not being as large as I'm aiming for, this is instead of looking at lots of different scenarios of what might happen with the market and in my life)

- income tax and NI equivalent of today (currently no NI on pension, 25%)

My route to get there is different from yours, but hope you find that helpful. I can dig out the numbers I'm assuming and add them here if desired.Statement of Affairs (SOA) link: https://www.lemonfool.co.uk/financecalculators/soa.phpFor free, non-judgemental debt advice, try: Stepchange or National Debtline. Beware fee charging companies with similar names.0 -

Is this of any help?barnstar2077 said:

Those fund names don't give a great deal away. Is there an area where you can select new funds on the pension website? I only ask as it will probably have more information about the different funds available there. As you are still young, you would probably benefit from having everything in a globally diverse 100% equities fund. Do you know why you have two different funds currently, is that the extra percentage point you started paying in recently?SieIso said:

Is this what you mean?barnstar2077 said:I would investigate how your money is invested in your pension, and what your options are for different funds etc. How your pot is invested can make a massive difference.

I wouldn't worry too much though, but if you can afford to put a bit more in then do so. The guy that you spoke to was hardly impartial as others have said!Early-Stage Growth Fund (Drawdown L/S) £84,881.52 Growth Fund (Drawdown L/S) £1,429.45

0 -

I think these are your pension providers names for the portfolios that they invest your money in, but the portfolios are made of actual funds or stocks. (Not sure I've got those terms right). It's the actual funds or stocks that people here can look up. (I think)SieIso said:

Is this of any help?barnstar2077 said:

Those fund names don't give a great deal away. Is there an area where you can select new funds on the pension website? I only ask as it will probably have more information about the different funds available there. As you are still young, you would probably benefit from having everything in a globally diverse 100% equities fund. Do you know why you have two different funds currently, is that the extra percentage point you started paying in recently?SieIso said:

Is this what you mean?barnstar2077 said:I would investigate how your money is invested in your pension, and what your options are for different funds etc. How your pot is invested can make a massive difference.

I wouldn't worry too much though, but if you can afford to put a bit more in then do so. The guy that you spoke to was hardly impartial as others have said!Early-Stage Growth Fund (Drawdown L/S) £84,881.52 Growth Fund (Drawdown L/S) £1,429.45

Statement of Affairs (SOA) link: https://www.lemonfool.co.uk/financecalculators/soa.phpFor free, non-judgemental debt advice, try: Stepchange or National Debtline. Beware fee charging companies with similar names.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.7K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards